Structured products as an alternative to bank deposits. Structural product

Structured products (SP) are complex financial instruments based on simpler (underlying) financial assets. At their core, structured products are “packaged” investment strategies. They are often combinations of traditional investments in stocks, bonds and derivatives.

Traditional investments and derivatives are combined into a single financial asset and securitized. Structuring allows you to obtain investment products with risk-return parameters that meet the specific needs and expectations of investors. Structured products have different forms (legal shell) and are issued by investment companies and banks.

Benefits and relevance

According to research by the European Structured Investment Products Association (EUSIP, www.eusipa.org), they are increasingly gaining confidence among investors. The reasons for the success of structured products lie in their basic properties: a certain (pre-known) level of profitability, protection from unfavorable market conditions and fixed investment terms.

It should also be noted that the launch time frame for new structured products is quite short, which allows them to quickly respond to new trends in financial markets.

Increased volatility in the foreign exchange, stock and bond markets creates favorable conditions for investing in structured products. Low interest rates in developed capital markets are also forcing investors to seek new financial instruments.

According to the EUSIP report, in the first quarter of 2015, the turnover of transactions with structured products traded on the exchange increased by 30% compared to the last quarter of 2014 and amounted to €39.2 billion, an increase compared to the first quarter of 2014 amounted to 17 %. In the first three months of 2015, European banks issued more than 980 thousand new structured products. This is 30% higher than in the previous quarter and 46% higher than in the previous year.

The volume of structured products issued in the first quarter amounted to more than €260 billion. There is no organization on the Russian financial market that centrally records transactions with structured products, so it is impossible to estimate its volume and its dynamics. According to the Department of Sales of Structured Products and Financing of the IT Invest company, of which the author is an employee, in the fourth quarter of 2014, products related to the national currency exchange rate were in demand among private investors; in the first and second quarters of 2015, increased demand for them remained.

Main types of structured (structured) products

There are many different types of structured products. Most of them are based on simple instruments that are freely traded on the stock exchange. However, investors are often unable to “put together a quality JV” on their own due to lack of access to a wide range of capital market instruments, restrictions on minimum transaction amounts, commissions and exchange fees, as well as insufficient expertise in structuring, derivatives pricing and hedging.

As noted earlier, in Russia there is no organization that systematizes information related to the release and circulation of structured products. Therefore, there is no official classification of joint ventures. In this case, the map of structured products developed by EUSIP for the European market (available on the organization’s website) can act as a conditional classifier. Let's look at it in more detail.

Investment products are a wide class of structured products, including products with different natures of risk and return, but united by a common attitude to the principles of investment. Each of the products in this class can be considered an investment in a security or strategy, with risk, return and participation in the growth or decline of the underlying asset of the structured product being elements of the system of packaging and transforming the risk of the investment.

Leverage products have a completely different nature in relation to risk and return. Structured products of this class imply the loss of the entire invested amount in the event of an unfavorable scenario for the chosen strategy. On the other hand, leverage also implies high potential returns in the event of a favorable outcome. The lion's share in the filling of these joint ventures is taken by option contracts, including exotic ones. By the way, leverage products have not gained popularity in Russia; Russian investors show the greatest interest in structured products of the investment group: with capital protection and increased profitability.

Capital protection (structured product)

Capital protection products provide a guarantee of return of the nominal amount of the investment - full or partial (at the investor's choice). In addition, they offer participation in the income from the rise or fall in the price of the selected underlying asset.

Capital protection products are suitable for risk-averse investors. They can be structured to benefit from both rising and falling markets during the life of the product, according to the investor's expectations of its behavior.

The main parameters of capital protection products - level of protection, underlying asset, investment period, participation in growth or decline, threshold prices - allow flexible adjustment of products to current market conditions.

Structured product with capital protection, popular on the Russian market:

Unlimited participation

Limited participation

Binary

Unlimited participation (structured product)

These products involve full or partial capital protection (at the investor’s choice) plus participation in the return of the underlying asset.

Market Expectations:

Growth of the underlying asset;

Increased volatility;

Characteristics:

Unlimited income potential;

The yield is determined by a parameter characterizing the level of participation and the price of the underlying asset on the maturity date of the product.

Profitability profile

Structure - fixed income instruments and purchased Call options.

Limited participation (structured product)

These products involve full or partial capital protection (at the investor’s choice) plus participation in the return of the underlying asset up to a certain level.

Market Expectations:

Growth of the underlying asset;

Possibility of a sharp fall in the underlying asset.

Characteristics:

The payment at the end of the term will be at least equal to the level of protection;

Capital protection is defined as a percentage of the original investment amount (eg 100%);

The value of the product may be below the capital protection level until the maturity date;

Yield is determined by a parameter characterizing the level of participation, the price of the underlying asset on the maturity date of the product and the maximum possible level of profitability.

Profitability profile

Structure - fixed income instruments and vertical call spreads.

Binary structure products

These products provide full or partial capital protection (at the investor’s choice) plus increased profitability if the underlying asset grows to a certain level.

Market Expectations:

Growth of the underlying asset;

Possibility of a sharp fall in the underlying asset.

Characteristics:

The payment at the end of the term will be at least equal to the level of protection;

Capital protection is defined as a percentage of the original investment amount (eg 100%);

The value of the product may be below the capital protection level until the maturity date;

The yield is determined by the price of the underlying asset on the maturity date of the product and the maximum possible level of yield.

Profitability profile

Structure - fixed income instruments and binary options Call.

Increasing profitability (structured product)

Structured products offer income in the form of a fixed coupon or multiple coupons. Investors give up participating in the rise or fall of the underlying asset in favor of a lump sum or series of payments. Enhanced yield products are suitable for investors who are willing to accept moderate to increased risk on their investment and who expect sideways movement in the underlying asset over the life of the product. The potential return is limited, and the risk of the product is lower than a direct investment in the underlying asset.

The terms of products are usually short and range from 1–6 months, if the product is serial - up to 2 years. The higher the current volatility of the underlying asset, the larger the fixed coupon will be. The expected decreasing volatility creates favorable conditions for purchasing products with increasing profitability.

Structured products with increased profitability, popular on the Russian market:

Reverse convertible;

Auto buyout (“Phoenix”).

Reverse convertible structural products

These products offer investors increased returns in the form of a fixed coupon. Upon completion of the product, the client receives 100% of the originally invested funds if the price of the underlying asset is higher than the predetermined strike price. Otherwise, the investor receives a predetermined amount of the underlying asset. The coupon is paid in both cases.

Market Expectations:

Neutral or weak positive dynamics of the underlying asset;

Reduced volatility.

Characteristics:

If the price of the underlying asset is below the strike price on the maturity date of the product, the invested funds will purchase the underlying asset at a predetermined price;

If the price of the underlying asset is higher than the strike price on the maturity date of the structured product, the investor is returned the amount originally invested plus a predetermined coupon;

The coupon is paid in any case, regardless of the position of the price of the underlying asset on the maturity date relative to the strike price;

The product allows you to obtain the underlying asset at a lower price;

Potential losses are less than when investing directly in the underlying asset, but comparable in absolute size;

Limited profitability of reverse convertible products.

Profitability profile

Structure - fixed income instruments and sold put options.

Autoredemption (structural product "Phoenix")

Products of the “Auto-repurchase” type are multi-period products for one or more underlying assets with initial prices and barriers, as well as the possibility of early withdrawal (early repayment) on the part of the issuer of the product (not on the part of the investor - the buyer of the product). There are various variations of the repayment terms of such products, in general they are similar to those described below:

1. If at the end of any period the prices of all underlying assets are higher than the established initial prices, the product will be redeemed early (autocall event) with payment of 100% of the originally invested amount plus coupons of all past periods;

2. If at the end of any non-last period (the calculated date of the period does not coincide with the end date of the product) the price of at least one of the assets is below its established barrier, then the coupon for this period is not paid, but the product continues to be valid. If in a subsequent period prices rise and exceed the established barriers on the settlement date, the client will receive a coupon for this period, as well as all coupons not paid in previous periods;

3. Execution of the product at the end of the last period will depend on the relative position of the prices of the underlying assets relative to the established barriers: if at least one asset has fallen below its barrier price by the maturity date, the product will be converted into a predetermined number of lots of the most fallen underlying asset.

Market Expectations:

Neutral or weak positive dynamics of the underlying asset (basket);

The underlying asset will not reach the barrier until the end of the product's life.

Characteristics:

Early buyback at 100% plus coupon if the underlying asset (basket) is trading above the barrier price by the end of the period;

Possible early redemption combined with attractive increased profitability;

Less risk than direct investment;

Limited potential profitability.

Profitability profile

The payouts for this product correspond to the put and call options sold, plus (sometimes) vertical call spreads on the underlying assets with strikes corresponding to the barrier and initial levels opened in a certain sequence. However, in practice, to hedge payments, the issuer of the product often does not trade options, but uses a replication of their value using a delta hedge. At the same time, to reduce the error in estimating the value of the product (payments), assets with low correlation are selected.

Products with participation (structured products)

A separate group of investment grade products that does not provide protection for the original investment. This is how they differ from the group's products with capital protection. The risk of investing in a joint venture is generally the same as the risk of investing in the underlying asset. However, their profitability may exceed the profitability of a direct investment in the underlying asset, and also have a zone with non-linear profitability.

It is worth noting that products of this group are not popular in Russia.

Exotic Structured Products

The underlying assets of the structured products described above are often stocks and currencies. This limits their “scope” to a certain extent. For example, funds, corporations and high-net-worth individuals often require products that hedge their investments and/or their business performance. For them, there is a class of so-called exotic products, the underlying assets of which, in addition to stocks, stock indices and currencies, are: credit default swaps (CDS), interest rates, commodity assets (oil, gold, industrial metals, agricultural commodities) and volatility.

A good example of such a product is structured notes linked to the performance of the HFRG Russian Guardian Index. The HFRG Russian Guardian Index is designed to demonstrate significant growth in times of financial stress for Russian assets.

To achieve this, the index consists of components that represent the prices of derivative financial assets that can show significant growth during periods of financial turmoil in a country. The component weights correspond to the premiums invested in those components. The premium is the maximum possible loss associated with each component of the index. The weights of the components change dynamically in order to achieve the highest possible return for a given fixed level of risk. Information on the HFRG Russian Guardian Index is available at www.hedgefundresearch.com.

Dynamics of HFRG Russian Guardian Index

Adding a structured note linked to the HFRG Russian Guardian Index to portfolios of stocks, bonds and ruble deposits can significantly improve their return and risk indicators during stressful periods of the Russian economy, one of which, by the way, is currently being observed.

Principles for choosing a structured product

To choose a structured product, an investor needs to decide on the following parameters of his future investment:

1. Risks - what part of the investment will be at risk and what will be the nature of this risk.

2. Timing - for how long will funds be diverted for investment, will it be possible to withdraw funds back before the completion date of the product.

3. Underlying asset - the investor must choose a financial asset that will determine the profitability of the investment made.

1. The price of the underlying asset will rise, fall or move in a sideways channel.

2. The volatility of the underlying asset will increase, decrease or remain unchanged.

Last but very important, the investor must make a guess about the future interest rates in the economy - whether rates will rise, fall, or remain the same.

As a rule, it is difficult for an inexperienced investor to immediately answer all the above questions. It will also be difficult for him to navigate among the wealth of forms and types of structured products. All this complicates the selection process. This is why the structured products industry offers its clients not products as such, but strategies packaged within them.

As noted above, due to the short release time and variety of types, joint ventures respond well to changing market conditions. This is perhaps one of the main reasons why structured products have become increasingly popular among investors in recent times.

At its core, structured products use a fairly simple idea, which is as follows. Let's assume that we find a bank that gives us 10% per annum in rubles. This means that from one million rubles a net income of 100 thousand is obtained - by investing this money in riskier investment products, the investor risks only his profit, while the main deposit remains untouched. True, with this approach it is necessary to take into account inflation, since the amount in rubles will lose part of its purchasing power after a year.

Consequently, when investing in structured products, the client's funds are divided into two components, one of which is usually noticeably larger than the other. The first, large part, is invested in fixed income instruments, such as bank deposits, bonds, bills or savings certificates; the risk part with increased returns can be stocks, shares of exchange-traded funds, futures, or even assets not related to finance (bet on political events - for example, the current situation with Greece).

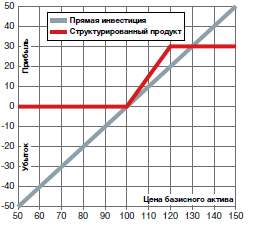

There are four possible situations here. The first situation of complete capital protection is discussed above and shown in the figure on the left. In it, all profits (the size of the orange zone) will be invested in risky assets, which, if the outcome is favorable, can provide income 2-3 times higher than the standard growth of the deposit. Those. will turn into a light brown area. If the result is unfavorable, the deposit amount remains unchanged.

In the second situation, the investor can behave more riskily, allocating a part of the deposit to aggressive assets that is greater than bank profits (i.e., in our original example, more than 10%) in exchange for a potential increase in income. As a rule, this happens when the investor, for some reason, is confident in the future change of the asset in the direction he needs. The figure on the right shows a situation where an investor is ready to lose up to 10% of invested funds, allocating 20% of the initial deposit to risky assets - capital protection is 90%. A favorable outcome here doubles the potential profit compared to the left figure, an unfavorable outcome leaves from 1 million rubles to 900 thousand.

Therefore, in terms of potential profitability, structured products represent a compromise between conservative and more aggressive investments:

There is a third situation, when some banks invest only part of the guaranteed profit in risky assets, which allows us to speak of a structured product as an instrument with guaranteed profitability. Those. The investor will receive a formal profit in rubles for any outcome of the risky part of the portfolio - although in an unfavorable case it will be less than inflation. This condition is partly related to Art. 834 of the Civil Code of the Russian Federation, which provides for the mandatory payment of interest on the deposit amount - some banks prefer to maintain structured products as a bank deposit. So it is better to check with the specific bank whether your structured product is subject to protection from the DIA. The general provision only says that individuals (compared to legal entities) in the event of bank bankruptcy will have a priority claim for repayment.

However, in addition to the described options, there are also those where the size of the client’s loss can potentially be equal to the deposit made. This is the most dangerous type. For example, these could be barrier structural products. Let's say a client invests in a pool of shares and makes a profit provided that none of them fall below a prescribed amount, say 30% of the last high. Breaking this barrier leads to losses proportional to the magnitude of the fall. Or it could be not a single stock, but an entire index of stocks - say, you are betting that the index of European shares will not fall below the value specified in the product. Or you can even bet that an asset will not exceed a certain value, or will remain within a certain interval. In other words, you come to a pure financial casino.

Participation rate

The coefficient is expressed either in numbers or as a percentage. It follows from the formula that the higher the coefficient, the greater the profit - but the greater the risk. In the case of CG > 1, we are usually talking about products using leverage (for example, futures).

Structured company products

From theory, you can move on to practice and see which companies and under what conditions offer similar products to investors (at the moment). Here is a small table

from which it can be seen that among the banks, the best offer in terms of the minimum entry threshold is currently the BCS company.

Structural notes

Structured notes can be considered a type of structured product, since the essence of the proposal remains unchanged - the division of capital into a base and a risk asset. As a financial instrument for an investor, notes appeared in the late 1960s in the USA - and the conditional difference between notes and the products discussed above can be considered the high entry threshold and the predominantly banking sector offering this service. At the same time, there may be surprises - for example, Trust Bank depositors lost their money when, succumbing to the persuasion of employees, they decided to transfer their funds from deposits to notes. Read more about this.

Why is a structured product dangerous?

The advantages of structured products include the opportunity to receive a potential income 2-3 times higher than a bank deposit, keeping your capital under protection and only risking not making a profit (however, the risk of bankruptcy of the issuer remains). Structured products are offered by many banks and companies, among which there are also offers with a relatively low entry threshold. However, you need to remember the following things:

investment may only be available in rubles;

the terms for which the products are offered (usually no more than three years) make the probability of income close to the toss of a coin;

management company services are paid, although they are often built into the product;

there is no ownership right to the structural product, i.e. all assets are registered in the name of the management company and in case of bankruptcy problems arise with the return of capital

Structured (sometimes the terms "structured" and "complex" are used) product– an investment portfolio formed by an investment company in the interests of the investor according to predetermined rules and sold as a single product. May include both stock market instruments and bank deposits.

The portfolio structure is built in such a way as to guarantee the investor a return not lower than a given one (usually a break-even or microscopic profit is guaranteed), while the full return of the product is unknown in advance. In addition to the minimum, the maximum return for the investor may also be limited, that is, if the portfolio generates a profit above a predetermined level, the investor receives a limited return, and the investment company receives all the return exceeding a given level.

A particular and simplest case of a structured product is an indexed deposit. A company or bank offering an indexed deposit guarantees the return of the investor's funds if the price of the underlying asset decreases and pays the investor an income equal to the increase in the price of the underlying asset (if it has increased) multiplied by a certain coefficient called the “participation coefficient”. Usually the coefficient is less than one (that is, the company and the investor share the income), but in some cases it can be more than one - if, in addition to the investor’s funds, the company uses leverage.

This structural product is constructed from two parts. The first is a bank deposit with a predetermined profitability, the second is any instrument that reflects the profitability of an asset chosen by the investor, for example, shares of a certain company, a stock option, mutual fund shares, futures on a stock index or commodity, etc. In this case, the size of the parts (structure) of the product is selected in such a way that the previously known return on a bank deposit covers part of the possible loss on the selected asset or all of the possible loss. As a result, the investor is guaranteed to get his money back, and if the bet is successful, he will receive a return that sometimes exceeds the bank interest.

More complex structured products can be issued in the form of bonds, notes, bills, investment shares, trust agreements, etc. They are built on the basis of a combination of various instruments. As part of the fixed income, not only bank deposits can be used, but also bonds, bills, savings certificates, and in the part with variable income (risky asset) - currencies, swaps, interest rate futures, shares of exchange-traded funds, synthetic products (volatility derivatives) , correlation), as well as instruments for non-financial assets (bet on weather, political events, natural phenomena).

In the line of investment objects, structured products occupy a place between instruments with fixed income and instruments with a previously unknown income, therefore they combine the positive and negative qualities of both types of investment instruments. On the one hand, the investor can be sure that he will receive a predetermined minimum level of return (or a loss no more than a predetermined one), but on the other hand, he does not receive the full income from the increase in the price of a risky asset and with a high probability can receive a return below bank interest. In addition, additional fees charged by the investment company and taxes can significantly reduce the investor's income.

If you have ever touched upon the issues of investing in stock assets, you have probably heard about the need to diversify your portfolio. And this is the right strategy - do not put all your eggs in one basket, but invest in a set of instruments with different levels of risk and return. In this way, the investor insures himself. You may have thought that it would be a good idea to immediately invest in a ready-made “set”. There is such an opportunity - which, as a rule, are issued by banks and investment companies and have a fixed validity period.

As the name suggests, these products consist of multiple assets, each with its own level of risk and return. Financial advisors, brokers and banks offer ready-made products developed based on in-depth analysis of markets and the economy. The investor’s task is to choose the one that meets his expectations from the investment.

How Structured Products Work

Structured financial products can be issued by a bank and sold directly, through a broker, asset manager or insurance company. In any case, the structured product is based on a combination of financial instruments.

That is, structured financial products work on a fairly simple principle: the investor’s funds are divided into two parts, usually a larger and a smaller one. Most of it is invested in financial instruments with fixed income (for example, reliable bank deposits, bonds, bills), and a smaller part is invested in risky and high-risk instruments that have increased profitability and even excess profitability (stocks, mutual funds, futures, options, etc. .). Simply put, the main point of structured products is to allow certain instruments to offset possible losses on risky assets.

There is also another way in which structural instruments work: banks invest only part of the guaranteed profit in risky assets. And then the investor receives a structured financial product with a guaranteed return (but this does not mean at all that the return will be high, it may even be less than inflation). By the way, when purchasing a structured product from a bank, check whether it is covered by deposit insurance - sometimes banks do this.

The investor's return is related to the so-called participation ratio, which determines what share of the underlying asset's return the investor will be able to receive. As such, there is no universal formula for the participation rate, but the return can be calculated as the product of the participation rate and the return on the asset at the end of the structured product's life, minus the risk. Typically, the coefficient is expressed as a percentage. The higher the participation rate, the higher the profitability and, of course, the higher the risk.

What are the types of structured products?

So, we were able to find out that structured products are intended to protect investments and additionally generate income against the backdrop of growth of their constituent assets. If you contact a specific broker or bank, you will be offered various structured products with beautiful and informative names and with different combinations of assets. And there can be a lot of such combinations. But in general, two main types of structural products can be distinguished.

- Risk-free products that guarantee a 100% capital return. That is, the investor only risks that upon expiration of the financial structured product he will receive only his capital, at most reduced by the amount of inflation.

- Limited risk products in which assets are divided into two parts to cover possible losses on risky investments. And here everything depends on the current situation and the state of affairs of the issuers: an investor can earn almost 50% of the investment or lose part of the capital.

Speaking about the types of structured products, it is perhaps worth highlighting notes that have recently appeared on the Russian market and are themselves an exchange instrument, that is, they can be bought and sold without waiting for the expiration date. We can say that notes are a pumped up and improved structural product. By purchasing a note, an investor receives a ready-made strategy with specified conditions. By the way, the entry threshold for notes is often much lower than for conventional structural products.

Structured products are interesting in themselves as a combination of several instruments, each of which has its own characteristics of circulation on the market. These financial instruments are in demand among investors of different levels due to their obvious advantages.

| Risk management is a key benefit of structured tools. Since they are a complex product assembled from several simple ones, risk diversification is built into the very idea of the instrument. The investor receives a portfolio in which part of the risks of some instruments is insured by the reliability of others. | |

|---|---|

| Possibility of entry for an inexperienced investor. Structured products are ready-made solutions and strategies developed by experienced analysts and brokers, professional participants in the stock market. That is, the investor does not need to make an independent decision about the structure of the portfolio, take responsibility for analysis, or make transactions. It is enough to inform the consultant about the desired level of profitability and acceptable level of risk. | |

| An integrated approach makes structured products successful. The investor receives a set of assets in one instrument and can be confident in certain guarantees of profitability. | |

| Structured financial products, despite their similarity to a bank deposit, can have many times higher returns, which are largely achieved due to the “risky” part of the instrument. Without actually taking any action, but having an economic sense and working closely with a broker, an investor can get a very profitable instrument. | |

| Guarantee of capital protection - at the time of expiration (expiration) of the structured product, the investor will receive back his money or money with an increase (but do not forget that inflation is also not asleep and the amount may actually decrease in purchasing power). | |

| Variability of terms - structured products can be created for a period from several months to several years, thus, the investor has the opportunity to choose whether he will receive income in the short term or make long-term investments. |

Structured products are both a complex and at the same time understandable tool with transparent operating principles. Using this type of instrument, a private investor protects his capital as much as possible and can regulate the level of risk. The main thing when working with this type of investment is to remember that behind the structured product there are stocks, bonds, options, futures and other assets that develop according to their own trends and under the influence of their own factors. Therefore, even if you absolutely trust a bank or broker, carefully study the composition of the structured product, familiarize yourself with the parameters and guarantees. After this, you can safely invest.

I became interested in BCS SP structured bonds. The product is relatively new and is practically not discussed.

Let's try to figure out how this works, using XS1604405545 as an example.

The company buys a portfolio of Eurobonds with 5 leverage, that is, it is similar to an ETF with a fixed coupon.

Let's assume you have about 100k and you can buy 1 lot of Gazprom Eurobonds with a yield of about 6%. Need more profitability? We borrow another 400k and buy 5 lots. Provided that the debt is not more expensive than the coupon, this increases the yield. According to rough estimates, to make a profit when paying a coupon of 12.5%, the margin must cost no more than 3% - this is approximately at the level of treasuries (cool, where can I get those?).

Next, we diversify the bond portfolio by adding Eurobonds from a couple of banks and something else with a similar coupon.

The scheme looks quite reliable. The risks are generally clear:

- risks of the issuer BCS SP (Cyprus) and the BCS group of companies

- the risk of default for one of the companies whose securities were purchased in the portfolio (hard to imagine)

- special section:

- discuss on the forum:

- Keywords:

- comment

- Comments ( 9 )

- 14 February 2019, 18:14

- D.R. LECTER

- Seal

At the forum, we were recently interested in a structured product from Sberbank, an exchange-traded bond BSO-OGZD_DIGIPRT-24m-001Р-02R,

Terms of issue can be viewed here: https://www.sberbank.com/common/img/uploaded/securities/emission/pbo/ogzd_digiprt-24m.pdf

The product is currently not very actively traded; the number of transactions on it is only a few units per day. The product itself is quite exotic and is a combination of a regular zero-coupon bond and a binary option with a bullish spread built into it. Obtaining additional profitability on the product depends on the behavior of quotes for Gazprom depositary receipts ADR.GAZP and the ruble/dollar exchange rate:

At a minimum you can get a denomination of 1000 rubles, at a maximum - 1253· α, where α is the ratio of USDRUB rates on the final and initial dates (now it is approximately 1.18) The final date is already close - the bond is redeemed on April 26, 2019. And it would seem that you can get almost 50% of the yield if the receipts are traded around 5.4 $. However, the bond is trading slightly above par. What's the catch?

This is largely due to the properties of binary options. Obtaining at least some yield on a bond is strictly tied to the condition that depositary receipts on the final date should cost more than they cost when the bonds were placed,

- special section:

- Keywords:

- comment

- ★8 | ₽ 10

- Comments (4)

- Keywords:

- comment

- Comments ( 52 )

- Keywords:

- comment

- Comments (0)

- special section:

- Keywords:

- comment

- ★38 | ₽ 112

- Comments (100)

After spending about 2 hours, I smoked it (I think), I don’t advise anyone to buy it and I think that the exchange should not have allowed such securities for trading.

What kind of animal is this?

Snowball coupon - means that subsequent coupons depend on the previous ones. For example, there may be a formula “previous coupon + 3% - LIBOR” and, accordingly, if the first coupon is 5%, and Libor is 4%, then the next coupon is 4%. And so on and so forth. But things are even more complicated for us