How to correct personal income tax registers in 1s 8.3. Accumulation register “calculations of taxpayers with a personal income tax budget”

We propose to consider the nuances of accruing and withholding personal income tax in the 1C 8.3 program. And how to properly prepare for reporting on forms 2-NDFL and 6-NDFL.

An important point is the setting in 1C "Registration in tax authority which is responsible for reporting to tax service. Go to the menu tab "Main" and select "Organizations".

We go to our organization, click "More" and in the drop-down list select the item "Registration with the tax authority":

The next important setting is "Salary Settings" in the "Salary and Human Resources" section.

Go to the "General settings" section and specify in the item "Accounting for settlements by wages and personnel records are kept” - “In this program” so that the relevant sections are available.

Here we go to the "personal income tax" tab, in which we indicate the procedure for applying standard deductions"The cumulative total for tax period»:

The rate of insurance premiums is “Organizations using DOS, except for agricultural producers”.

Accident contribution rate - indicate the rate in percentage terms.

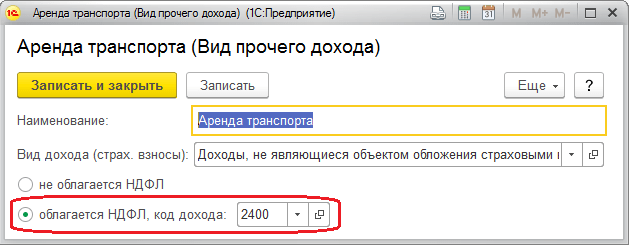

All accruals made are based on the income code for individuals, which can be viewed in the built-in reference book "Types of personal income tax».

This directory can be corrected, for this we return to the "Salary Settings", expand the "Classifiers" section and follow the "Personal Income Tax" link:

After that, the window "Personal income tax calculation parameters" opens and go to the desired tab "Types of personal income tax":

To set up personal income tax taxation for accruals and deductions, in the "Salary settings" window, expand the "Payroll" section:

To start accounting for wages and personal income tax, the established parameters are enough. But do not forget to update the configuration to the current one.

Personal income tax is accrued and calculated for each actual income received on a monthly basis at the end of the reporting period (month) according to the documents “Payroll”, “Vacation”, “ Sick leave" and others. Consider the document "Payroll".

The tax amounts for each employee will be reflected on the "Personal Income Tax" tab:

The same information can be viewed in the postings:

Based on the document, an entry is formed in the register “Accounting for income for the calculation of personal income tax” and the reporting forms are filled out:

Expenditure cash order for the issuance of cash DS;

The document posting date will be the tax withholding date.

Let's pay attention to the document "Individual income tax accounting operation". According to it, personal income tax is calculated from dividends, vacation pay and other material benefits. To create a document, you need to go to the “Salary and Personnel” tab, the “Personal Income Tax” section and click the link “All documents on personal income tax”.

We get into the magazine. To create a new document, click "Create" and select the desired option from the drop-down list:

An entry in the register “Settlements of taxpayers with a personal income tax budget” generates almost every document that affects personal income tax.

Consider the example of the document "Write-off from the current account". Let's go to the tab "Salary and personnel" and open the item "Statements to the bank":

Let's create this document. And on the basis we will make a write-off from the account:

As well as register movements.

- 1 Possible errors in the calculation of personal income tax in the program 1C 8.2 ZUP 2.5

- 2 Possible errors in the calculation of personal income tax in the program 1C 8.3 ZUP 3.0.

- 3 Possible errors in the calculation of personal income tax in the program 1C 8.3 Accounting 3.0

- 4 Possible errors in the calculation of personal income tax

- 5 Possible errors in inter-settlement documents on the example of 1C 8.3 ZUP 3.0

- 6 Possible errors in inter-settlement documents using the example of 1C Accounting 3.0

- 7 Possible errors in inter-settlement documents on the example of 1C 8.2 ZUP 2.5

Possible errors in the calculation of personal income tax in the program 1C 8.2 ZUP 2.5 Let's consider in the program 1C ZUP 2.5 on the example of the document "Vacation". Vacation pay was accrued, which was originally planned to be paid on January 29, 2016. In fact, the payment is made on January 28, 2016. Therefore, we change the date of income payment in the vacation accrual document to January 28, 2016.

Some users of the 1s 8.3 program have problems with personal income tax. And how are you?

There are any ways to roll back from the last update and even a few pieces back. In November, everything was still fine. And now, from impotence, I just feel like stupidly crying Added: Jan 19, 2018, 11:27 Quote: Gennady ObGES on Jan 19, 2018, 05:49 Just in case, I’ll clarify - the documents were retranslated (including those not completed), months restarted? Well, how can you answer this based on the screenshot and the lack of even minimal information Gennady Ob HPP, please tell me what kind of information to provide? I started everything from scratch, consistently made and carried out accruals - statements - payments.

Nothing helps. The fact that after the updates, the accrual tables have changed dramatically is a fact. I do not understand the technical subtleties, but something is clearly not right in the update.

Personal income tax accounting in 1s 8.3 accounting 3.0

Important! To avoid possible errors in personal income tax, track in the 1C 8.3 (8.2) program the correspondence between the date of income in the income register and the date of income in the tax register, otherwise the program will have errors when calculating tax. When registering any income in the program, the date of actual receipt of income is fixed.

For incomes with code 2000, this is the last day of the accrual month. For other income, this is the planned payment date from the corresponding accrual document.

When the tax is calculated, the program analyzes from which income this tax is charged, and determines the date of actual receipt of income, which is recorded in the tax accounting register. Why can there be a difference in the date of receipt of income, which is taken into account in the income register and the register tax accounting for personal income tax? Consider below.

Income tax calculated is not equal to withheld

Possible errors in inter-settlement documents on the example of 1C 8.3 ZUP 3.0 On the example of the program 1C ZUP 3.0 in the document "Vacation" the planned payment date is 01/28/2016, but we will set the document date to 01/30/2016, that is, later than the planned payment date. Let's get it through. The record of the Tax Accounting Register was formed as of January 30, 2016.

Important

If we pay vacation pay earlier than the date of the document - 01/28/2016, as planned, fill out the statement, we see - the personal income tax withheld is not filled out. As of 01/28/2016, there is no calculated tax. Accordingly, when conducting such a statement of personal income tax, the retained is not registered.

Attention

If everything is fine with the date of the document and it is earlier than the planned date of payment: Then when filling out the statement, everything will also be fine, the tax will be determined. When conducting the Vedomosti, it was recorded as a withheld tax.

The problem with NDFL

Possible errors in inter-settlement documents using the example of 1C Accounting 3.0 In the 1C Accounting 3.0 program, everything is the same. The date of the document is important. Consider the example of the document "Vacation". The planned payment date is 01/28/2016, and the date of the document will be deliberately set later, for example, 01/30/2016. Let's post the document. The calculated tax was registered as of 01/30/2016.

After the payment has been made, and not in the Vedomosti, namely the payment “Cash Withdrawal” or debiting from the current account earlier than the date of the “Vacation” document, the tax withheld is not registered, determined and not recorded in the Register. Therefore, the date of the document is important, if we put on January 28, 2016 and re-issue cash, then the personal income tax record withheld was formed, everything fell into the Register and then it will fall into form 6-personal income tax.

Possible personal income tax errors in 1s 8.3 and 8.2 - how to find and fix

There is also a payment date here and when this date changes, everything changes automatically. The date of receipt of income for personal income tax also changes automatically.

But, just in case, check. Possible errors in the calculation of personal income tax Also, when calculating personal income tax, we must pay attention to the date of calculation of the tax. This is true for programs of the third version. The tax due date must be strictly prior to the tax withholding date.

If at the time of withholding the tax, the tax itself is not accrued, then, in fact, there is nothing to withhold. Important! Track in the 1C program: the dates of inter-settlement documents are the date the tax is charged, if at the time of payment the tax is not charged, then it will not be withheld. This is especially true for non-salary income, since the date of the document is fixed as the tax date. Thus, in the third version, the date of the “Vacation” document, the date of the “Sick leave” document and other documents are also important.

But if we change the date in the main form of the document, the date is automatically changed in the form “More about the calculation of personal income tax”. It's easier here, the ZUP 3.0 program. itself guarantees us that these dates will coincide.

The only thing is that in the current release of the 1C program there is an error for the document "Sick leave". If it is paid with a salary, and we change the date of payment, then in this case the date of receipt of income in the form “More about the calculation of personal income tax” itself does not change.

Here you need to make a recalculation, or change the date in the form "More about the calculation of personal income tax" manually. For all other cases, the personal income tax accounting date should change automatically at the date of payment. But just in case, check this moment, control the coincidence of dates. Possible errors in calculating personal income tax in the program 1C 8.3 Accounting 3.0 As for the program 1C Accounting 3.0, there are also two inter-settlement documents “Sick Leave” and “Vacation”.

One line in the personal income tax with a “minus” dated 01/29/2016, and the second line with a “plus” dated 01/28/2016. Two more groups of lines from 100 to 140 are added to the 6-personal income tax. In one, everything is reversed, and in the other - everything is re-calculated. To avoid such a situation, carefully monitor the date of receipt of income, which will be recorded in the Income Register and the date of receipt of income, which will be recorded in the Tax Register.

They must match. Possible errors in the calculation of personal income tax in the program 1C 8.3 ZUP 3.0. In the 1C ZUP 3.0 program, the date of receipt of income is also taken into account in two registers: the Income Accounting Register and the Tax Accounting Register.

For example, consider the document "Vacation". The date of payment from the main form of the document goes to the Income Accounting Register. And in the Tax Accounting Register - the date from the form "More details about the calculation of personal income tax."

These two dates must match.

In this article, we will consider working with personal income tax in 1C 8.3 Accounting 3.0 - from settings to operations and reporting. Content

- 1 Program setup

- 1.1 Tax data

- 1.2 Salary setup

- 2 Personal income tax accounting operations in 1C

- 3 Reporting

- 4 Checking the correctness of personal income tax calculation

Today we will consider what - what tools and functionality the 1C program has for calculating personal income tax and its correct reflection in tax accounting.

The taxation procedure is entered when setting up the calculation type.

Fig.1

The code from Fig. 1 can be selected in the “Types of personal income tax income”, where each element is assigned a percentage of taxation and indicates whether it relates to wages.

The category of income allows you to clarify the date of its receipt in the statement that was originally indicated in settlement document. To specify the procedure for calculating the tax on the income of laid-off workers in the reference book of the same name, the calculation procedure is selected.

Fig.2

To indicate the option for calculating taxes for other incomes of individuals, the corresponding directories are also used.

Fig.3

You can designate the income code directly in the document field.

Fig.4

The deductions are stored in the "Types of personal income tax deductions".

Advance tax payments foreign citizens are fixed by the document of the same name "Advance payments for personal income tax". The statement on the legitimacy of the offset of the advance is located in "1C-Reporting".

In the personal income tax registers in 1C 8.3, settlement documents record the taxable base and the calculated tax, which is determined on the date of actual receipt of income.

The tax from all kinds of benefits, vacation and other inter-settlement payments in the documents is displayed immediately on the planned date of payment.

The actual receipt of income for types of calculation, in the income code of which it is indicated “Corresponds to wages”, is dated by the last day of the month of accrual or the date of dismissal.

Fig.5

Income is fixed in "Accrual ...", "Awards", etc.

Fig.6

Fig.7

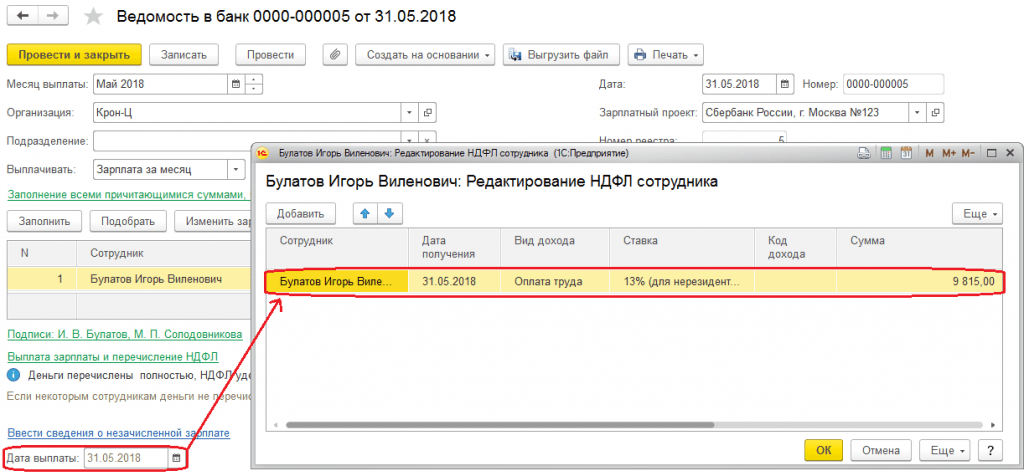

The tax withholding is dated from the date of payment entered on the payroll. The actual date of payment is also fixed by the documents “Confirmation of payment of income”, “Confirmation of salary transfer”.

When calculating the withholding, the basis document is filled out, according to which the amount of income is fixed, which is subsequently taken into account in line 130 in the 6-NDFL report.

For display in reports, the transferred tax is displayed in the payroll sheet when the attribute "Tax together with salary" or a separate form "Transfers to the budget" is indicated. In this case, the transfer period is determined by the type of income. The deadline is registered in the system during deduction and is used when compiling the 6-NDFL report.

For the analysis of personal income tax, there are the following reports:

- Monthly analytics;

- Register of tax accounting for personal income tax;

- Consolidated 2-personal income tax.

If it is necessary to recalculate the tax in the ZUP for any reason, then use the document “Recalculation of personal income tax”, located in the “Taxes and contributions” menu. Here the tax is recalculated from the beginning of the tax period specified here.

Fig.8

To adjust the accounting for the type of tax in question, 1C ZUP uses a specialized document “Individual income tax accounting operation”. It allows you to edit tax registers:

- deductions, predst. upon notice to the NO;

- Provided standard and social deductions;

- Calculations of tax agents / taxpayers with the personal income tax budget;

- Accounting for income for the calculation of personal income tax.

If the tax is excessively withheld for the employee, then in the current period he will pay for it with a “minus”. In the event that for the current month his total amount for an employee is negative, he will not be withheld and will not be accepted as offset against future payments. In settlement documents, personal income tax for offset can be seen on the "Payment Adjustments" tab. In the next period, the system will automatically reduce the withheld tax by the amount of the adjustment, but you can also return the tax using the "Refund".

The correct accounting of personal income tax in the system depends on the correctness of filling in the registration with the tax authority in the subdivision/organization card. Upon registration with the tax authority, relevant reports are collected in the ZUP. Based on the period for issuing income, the deadline date for the transfer is calculated, which is displayed in the registers during posting.

2016-12-08T15:29:55+00:00Question from reader Marina Vasilievna:

Put new program 1 C 8.3 Accounting. I'm not quite familiar with this program yet.

We rent a car from an individual, I register the rent through manual transactions entered by DT 44.1 KT 76.5 in the same place I charge personal income tax DT 76.5 KT 68.1.

But the accrued personal income tax does not fall into the register of tax accounting for personal income tax. In 1C Accounting 7.7, I carried out this personal income tax through the Adjustment of personal income tax data,

And in 1C 8.3 I can not find such a function. If possible please help me.

Answer:

To reflect the settlements with the budget for personal income tax in tax accounting an accumulation register is provided: " Calculations of tax agents with the personal income tax budget".

If we open this register using the menu " ":

we will see something like this:

All these are movements according to the register, formed during the issuance of wages to employees.

But our task is to reflect these same movements when withholding personal income tax from an individual from whom we rent a car, right in the manual operation. How to do it?

Let's open a manual operation in which we reflect our postings:

DT 44.1 KT 76.5

DT 76.5 KT 68.1

I have everything very schematically:

And from the topmost item "More" select the item "Choice of registers":

A list of registers will open, we need to tick off those movements for which we want to display:

Click "OK" and see that an additional tab for editing the case has appeared in the "Operation" document:

We press the "Add" button and fill in the line upon receipt of personal income tax for the individual we need:

Sincerely, Vladimir Milkin(teacher and developer).

We propose to consider the nuances of accruing and withholding personal income tax in the 1C 8.3 program. And how to properly prepare for reporting on forms 2-NDFL and 6-NDFL.

An important point is the setting in 1C "Registration with the tax authority", which is responsible for submitting reports to the tax service. Go to the menu tab "Main" and select "Organizations".

We go to our organization, click "More" and in the drop-down list select the item "Registration with the tax authority":

The next important setting is "Salary Settings" in the "Salary and Human Resources" section.

We go to the "General settings" section and indicate in the item "Payroll accounting and personnel records are maintained" - "In this program" so that the corresponding sections are available.

Here we go to the "Personal Income Tax" tab, in which we indicate the procedure for applying standard deductions "Cumulative total during the tax period":

The rate of insurance premiums is “Organizations using DOS, except for agricultural producers”.

Accident contribution rate - indicate the rate in percentage terms.

All charges made are formed on the basis of the income code for individuals, which can be viewed in the built-in directory "Types of personal income tax".

This directory can be corrected, for this we return to the "Salary Settings", expand the "Classifiers" section and follow the "Personal Income Tax" link:

After that, the window "Personal income tax calculation parameters" opens and go to the desired tab "Types of personal income tax":

To set up personal income tax taxation for accruals and deductions, in the "Salary settings" window, expand the "Payroll" section:

To start accounting for wages and personal income tax, the established parameters are enough. But do not forget to update the configuration to the current one.

Personal income tax is accrued and calculated for each actual income received on a monthly basis at the end of the reporting period (month) according to the documents “Payroll”, “Vacation”, “Sick Leave” and others. Consider the document "Payroll".

The tax amounts for each employee will be reflected on the "Personal Income Tax" tab:

The same information can be viewed in the postings:

Based on the document, an entry is formed in the register “Accounting for income for the calculation of personal income tax” and the reporting forms are filled out:

Expenditure cash order for the issuance of cash DS;

The document posting date will be the tax withholding date.

Let's pay attention to the document "Individual income tax accounting operation". According to it, personal income tax is calculated from dividends, vacation pay and other material benefits. To create a document, you need to go to the “Salary and Personnel” tab, the “Personal Income Tax” section and click the link “All documents on personal income tax”.

We get into the magazine. To create a new document, click "Create" and select the desired option from the drop-down list:

An entry in the register “Settlements of taxpayers with a personal income tax budget” generates almost every document that affects personal income tax.

Consider the example of the document "Write-off from the current account". Let's go to the tab "Salary and personnel" and open the item "Statements to the bank":

Let's create this document. And on the basis we will make a write-off from the account:

As well as register movements.