Psk according to the new formula. What does the total cost of the loan mean?

When issuing a loan, the bank informs the client about the interest rate for using the loan. Often, trying to attract customers, credit institutions declare an attractive interest rate for using a loan, but not all borrowers pay attention to additional fees and payments to the bank, which significantly increase its cost. At the same time, credit institutions receive their financial benefit from these fees.

According to the adopted Directive of the Central Bank of Russia No. 2008-U, banks are required to indicate in the agreement the full cost of the loan, including payments in their favor made by the borrower once. This document states that when calculating the full cost of the loan, the credit institution is obliged to inform the borrower about all types of payments that he will have to pay in its favor, including indicating the calculation of the following operations:

Repayment of the principal amount of the loan;

- repayment of interest for using the loan;

- payment of the commission amount for execution of the contract;

- payment of a commission for issuing a loan;

- commissions for opening an account and maintaining it;

- fees for settlement and cash services, for servicing a credit card.

Also included in the full cost of the loan are mandatory payments to insurance companies, fees for the services of notaries and lawyers when drawing up various necessary documents for pledging the property pledged as collateral for the loan.

The total cost of the loan does not include insurance payments from compulsory motor liability insurance, fees for obtaining and repaying the loan in cash, including payments through ATMs (sometimes these interests can reach 3-5% of the total amount). The possible payment of a fine for a late payment on a loan, for blocking a card, withholding a commission for crediting funds to a credit card by third-party credit organizations, etc. is also not taken into account.

Concept of effective interest rate and opportunity cost

All of the above payments significantly increase the cost of the loan for the borrower. However, in conditions of fierce competition in the lending market, in an effort to attract customers, banks in most cases refuse to charge most commissions, but even in this case, the cost of the loan will be higher than stated in the agreement. This is because there is the concept of effective interest rate and compound interest. In this case, the calculation of the total cost of the loan takes into account the amount of lost profit of the borrower, which he could have extracted from his finances if he had not paid interest on the loan with it, but put it on deposit at interest.

To find out the full amount of the loan cost, the borrower must carefully read the document under which he will sign before signing the agreement.

The loan price is the main criterion for a borrower to select a loan offer. This is the monetary expression of the fee for using borrowed money, which reflects the amount of overpayment for the loan.

What determines the price of a loan?

The price of a loan is closely related to the principle of remuneration of credit relations, because The bank receives income when issuing a loan. The loan rate is determined as the ratio of the bank's income for issuing a loan to the loan amount. For example, with a loan amount of 100 thousand rubles. and the loan price is 25 thousand rubles. the annual rate will be 25%.

The price of the loan is directly determined by the level of the interest rate. The latter is formed under the influence of the relationship between supply and demand for various types of credit. It depends on a number of factors:

Dynamics of attracting household deposits, as well as the average interest rate on deposits;

Economic situation in the country (inflation rate, etc.) - the loan rate must cover the inflation rate;

Credit policy of the Central Bank of the Russian Federation, the refinancing rate at which the Central Bank of the Russian Federation lends to other banks;

Average interest rate on the interbank lending market;

The structure of the bank's assets, the greater the share of attracted funds, the more expensive the loan;

The level of competition in the market, which affects the demand for loans from borrowers; the less it is, the cheaper the loan;

Duration and type of loan;

The degree of risk of the loan - unsecured loans without guarantors have a higher degree of risk and are issued at a higher interest rate.

How the real price of a loan is formed

It would seem that calculating the real price of a loan, knowing the annual interest rate and the loan term, is quite simple. But in this case there are pitfalls, and the actual price of the loan can be several times higher than the fixed interest rate.

Loan payments are made up of payments for repayment of the principal debt, interest on the loan, and commissions. The latter are often hidden from the eyes of users at the stage of concluding a contract. These may be fees for processing and issuing a loan, for opening and maintaining an account, and for its maintenance.

Some banks charge an additional fee for cash withdrawals (usually when using credit cards).

The agreement may also establish payments to third parties at the expense of the borrower. As a rule, this applies to mortgage loans that require payment for the services of appraisers, insurers, notaries, etc., or car loans (payment of CASCO). All this can lead to the fact that the rate of 20% per year, taking into account all commissions, can turn into 50%.

Separately, fines and penalties for late monthly payments can be included in the cost of the loan. They are individual for each bank.

Recently, laws have appeared in Russian law that protect borrowers from hidden fees and interest. The bank is obliged to inform the borrower about all types and terms of loan payments.

Thus, according to Russian law, banks must notify the borrower of the total cost of the loan (FLC), which is expressed as a percentage. It must include all payments established by the contract. Also courts

After the entry into force of Federal Law No. 353-FZ of December 21, 2013 “On consumer credit (loan)”, the full cost of the loan must also be determined in a mortgage loan agreement (loan agreement) not related to the borrower’s business activities. So what is the full cost of the loan?

If you look at it, the total cost of credit (TCC) is the same interest rate on the loan, but takes into account not only interest on the use of debt, but also other expenses the borrower incurs when receiving a loan. Accordingly, the total cost of the loan is calculated in annual percentage.

Until mid-2008, the term “effective interest rate” was used instead of the term “full cost of credit.”

Previously, the calculation of the full cost of the loan was carried out using the compound interest formula and also included the income lost by the borrower from the possible investment of the amount of interest payments on the loan during the loan period at the same interest rate as on the loan. Thus, the total cost of the loan exceeded the interest rate specified in the loan agreement, even in the absence of commissions and other payments, which was sometimes incomprehensible to borrowers.

In 2014, amendments were made to the law on consumer lending, which introduced a new formula for calculating the PSC from September 1, 2014. Taking into account the changes in the calculation of the PSC, there is now no mandatory interest multiplication, therefore, in the case when the borrower does not pay any additional fees when receiving a loan, the calculated value of the total cost of the loan and the interest rate indicated in the loan agreement will be as close as possible to each other.

INcalculationPSKturn onfollowingpaymentsborrower:

- to repay the principal amount of the mortgage loan;

- to pay interest on a mortgage loan;

- payments by the borrower in favor of the lender, if the borrower's obligation to make such payments follows from the terms of the loan agreement and (or) if the issuance of a mortgage loan is made dependent on the making of such payments;

- fee for issuing and servicing an electronic means of payment when concluding and executing a loan agreement;

- payments in favor of third parties, if the borrower’s obligation to make such payments follows from the terms of the loan agreement that defines such third parties, and (or) if the issuance of a mortgage loan is made dependent on the conclusion of an agreement with a third party. If the terms of the loan agreement specify a third party, the tariffs applied by this person are used to calculate the full cost. The rates used to calculate the total cost may not take into account the individual characteristics of the borrower. If the lender does not take such features into account, the borrower should be informed about this. If, when calculating the full cost, payments in favor of third parties cannot be unambiguously determined for the entire loan term, the calculation includes payments in favor of third parties for the entire loan term based on the tariffs determined on the day the full cost is calculated. If the loan agreement specifies several third parties, the full cost can be calculated using the tariffs applied by any of them, and indicating information about the person whose tariffs were used in the calculation, as well as information that when the borrower contacts for another person, the full cost of the mortgage loan may differ from the calculated one;

- the amount of the insurance premium under an insurance agreement if the beneficiary under such an agreement is not the borrower or a person recognized as his close relative;

- the amount of the insurance premium under a voluntary insurance agreement if, depending on the conclusion of a voluntary insurance agreement by the borrower, the lender offers different terms of the loan agreement, including in terms of the loan repayment period and (or) the full cost of the loan (loan) in terms of the interest rate and others payments.

INcalculationPSKNotturn on:

- payments by the borrower, the obligation of which by the borrower follows not from the terms of the loan agreement, but from the requirements of federal law (for example, registration fees);

- payments related to non-fulfillment or improper fulfillment by the borrower of the terms of the loan agreement (penalties, fines);

- payments by the borrower for loan servicing, which are provided for in the loan agreement and the amount and (or) terms of payment of which depend on the decision of the borrower and (or) the option of his behavior;

- payments by the borrower in favor of insurance organizations when insuring the subject of the mortgage;

- payments by the borrower for services, the provision of which does not determine the possibility of obtaining a mortgage loan and does not affect the value of its full cost in terms of interest rates and other payments, provided that the borrower is provided with additional benefits compared to the provision of such services on the terms of a public offer and the borrower has the right to refuse the service within 14 calendar days with a refund of part of the payment in proportion to the cost of part of the service provided before notification of refusal (for example, the cost of real estate services).

PSC = i * NBP * 100%,

NBP is the number of base periods in a calendar year. The length of a calendar year is recognized as 365 days. For a standard mortgage payment schedule with annuity monthly payments: NBP = 12.

The interest rate of the base period (i) is determined by the selection method as the smallest positive solution to the equation:

DPk is the amount of the kth cash flow (payment) under the loan agreement. Multidirectional cash flows (payments) (inflow and outflow of funds) are included in the calculation with opposite mathematical signs - the provision of a loan to the borrower on the date of its issuance is included in the calculation with a minus sign, the borrower’s repayment of the loan, payment of interest on the loan are included in the calculation with a minus sign "plus";

qk is the number of complete base periods from the moment the loan is issued to the date of the kth cash flow (payment).

ek is the period expressed in shares of the base period, from the end of the th base period to the date of the k-th cash flow.

m is the number of cash flows (payments);

i is the interest rate of the base period, expressed in decimal form.

Looks scary.

This formula for the UCS is quite complex for everyday understanding, so I will try to explain the calculation of the USC a little more simply, although, unfortunately, it will not work out very simply.

Let's sort it out example.

Credit issued 01.08.2014 V amount 2,6 million. rubles on term 120 months. Term repayment(N) - 08/01/2024G. Interest bid 12,4% per annum. Additional commissions Not was.

The first period payment (interest only) is 26,498 rubles, the annuity is 38,232 rubles.

In order to calculate the annual PIC rate, you first need to find the interest rate of the base period (i), and for this you need to solve the equation. By the way, the base period in a mortgage is a month. Those. in fact, we will now determine the monthly PSC rate.

Solve the equation (you can solve it in MS-Excel).

Everything that the lender gives to the borrower, namely the loan amount, is put in the formula with a “minus” sign, and what the borrower pays, the amount of annuity and commission, is put with a “plus” sign.

Those. for our example it will look like this:

IN given example it turns out, Whati = 0.01033.

At the beginning We talked, Whati -This monthly meaning PSK. Because Now we think annual size PSK:

PSK= 0.01033 x 12 x 100% = 12.396%

The UCS size is written rounded to 3 decimal places.

Similar to the interest rate specified in the contract, i.e. 12.4%, it seems.

Tnow we'll figure it out another example, With additional expenses.

Additionally To above for example, let's say borrower pays following commissions:

- one-time pay behind carrying out independent estimates subject collateral - 3000 rub.

- one-time insurance bonus By mortgage insurance - 12500 rub.

- esimultaneous commission behind opening letter of credit - 2600 rub.

- annual insurance bonus By personal insurance - 0,85% from NEO+10% (first payment - 24310 rub., etc.).

Again we find interest bet basic period(i).

IN given example it turns out, Whati = 0.01136.

Now we think annual size PSK:

PSK= 0.01136 x 12 x 100% = 13.632%.

As we can see, if there are some one-time and permanent (annual) commissions associated with issuing a loan, the size of the total cost of the loan (the value of the TSC) increases, and instead of 12.4% in our example, we get 13.632% per annum.

By independently calculating the total cost of loans (TCC), or by looking at this information on banks’ websites (they must disclose this information and many banks’ websites have special calculators), the borrower can choose the loan that suits him.

Information about the full cost of the loan (loan) must be placed in a square frame on the first page of the credit agreement (loan agreement), printed in black capital letters on a white background in a clear, easily readable font of the maximum size from the font sizes used on this page. The area of the square frame must be at least five percent of the area of the first page of the loan agreement.

Example placement information O PSK:

When choosing a loan, the borrower studies the loan products of a number of banks and pays attention to promotions of credit institutions offering low interest rates on loans. But few people know that

What is the total cost of the loan?

The total cost of the loan (FLC) is the amount that the client will actually pay to the bank for using the funds, the real price of the loan.

The practice of disclosing the real price of a bank loan did not appear in Russia immediately, but after several years of indignant misunderstanding between credit institutions and borrowers. Psychologically, the price of a loan at 11% per annum for 15 years seems attractive, but in the end, over the entire repayment period, you will have to pay twice as much as was taken. The matter was further complicated by the abundance of commissions, in percentage and with a fixed amount. Some interest was calculated on the balance amount, and others on the original loan amount. In such a situation, it is impossible to determine the real cost of a bank loan without complex calculations.

PSC is expressed in %, but does not coincide with the annual interest rate under the contract. This happens because the price, in addition to interest, may include payments for:

- for processing the application and checking the borrower’s data;

- for registering and maintaining a credit account;

- for issuing bank cards under a loan agreement;

- for operations in the process of processing and maintaining a loan;

- the cost of insurance, if the conclusion of an insurance contract is a condition of the bank for issuing a loan, or determines the amount of rates and commissions on it;

- other client expenses directly related to the issuance of a bank loan, including mandatory payments to third parties.

The full cost of the loan must be calculated before receiving it, because... lending conditions are known in advance.

It is important to consider that the list of expenses included in the CSC is not endless. It cannot be expanded by analogy, in the opinion of one of the parties to the transaction or by the decision of any other persons and organizations.

In the Russian Federation, the law “On consumer credit (loan)” has been in force since 2013. The following year, 2014, a formula for calculating the full cost of a loan became mandatory for banks (we’ll talk about it below).

The following is not included in the PSC:

- Expenses of the borrower made not according to the terms of the loan, but based on legal requirements. This may also apply to certain types of insurance.

- Penalties and additional costs associated with violation of payment discipline.

- Additional costs for servicing the loan, which are a consequence of the client’s choice. An example is an increase in the loan repayment period, which entails a recalculation of the total interest amount.

- Various types of commissions and additional payments for certain methods of loan repayment: in cash, through terminals of other banks, using third-party payment systems.

- Fee for the movement of funds on a bank card issued under a loan agreement.

It follows that the full cost of the loan is not necessarily equal to the amount that the borrower will actually pay the lender. Because During the repayment process the following are possible:

- Delays in payments or early repayment. For the first, a penalty is charged, the second promises a recalculation of interest and a reduction in the total cost of the loan or penalties, if this is provided for in the agreement.

- Changes in loan repayment conditions. This possibility is often specified in the contract, but its occurrence is linked to external circumstances.

These and other circumstances may affect the amount actually paid by the borrower. But if the changes at the time of receiving the loan are not known, or their occurrence does not depend on the lender, then they will not be included in the total cost of the loan.

It is important that the full cost of the loan is known in advance, even before receiving it. If the bank hides information about this, the transaction must be declared invalid, the loan agreement must be terminated, and the funds spent by the client must be returned to him.

For recipients of bank loans, it is the value of the total cost of the loan, and not the interest rate, that should be the criterion for evaluating and comparing different loan products.

How to calculate the total cost of the loan?

The process of calculating the real price of a loan occurs using complex formulas, which for the average consumer take a long time and are not necessary to learn. However, it is useful to understand how this calculation occurs.

First of all, let’s clarify that all payments under the loan are calculated using their own formulas. The principal interest, commissions and other payments are calculated separately (depending on the terms of the agreement - on the initial amount or on the unpaid balance). Then all the resulting figures are summed up to form the total price of the loan.

The formulas below for calculating the cost of a loan will help you find out the payments, and not the principal amount from which interest and other relative values are calculated.

The first of the calculation formulas looks like this:

PSK = i x NBP x 100;

here PSC is the total cost of the loan; NBP – number of base periods; i – interest rate in the base period. The base period refers to the period between making mandatory loan payments.

This equation is given in the text of the law “On Consumer Credit (Loan)” and is applied.

The upper part of the fraction, with the letters DK, is the amount of a specific payment. If it is made to the bank, then the amount is accepted with a positive sign, if it is a loan - with a negative sign. The second bracket contains the payment value for the full base period, the first bracket calculates the payment for part of the period. All the results obtained are summed up and ultimately equal 0. Which means the equality of cash flows received by the bank and paid by the borrower. This equation is rarely used for pen and paper calculations. It is more convenient to calculate the UCS by substituting data into an Excel table with formulas already entered.

A simplified formula for calculating the cost of a loan will help you make your own calculation:

It is calculated like this:

- the sum of all loan payments (S) is divided by the amount received from the bank (S0);

- one is subtracted from the result of division;

- the resulting number is divided by n - the number of years to repay the loan, and multiplied by 100.

The final value is presented as a percentage. You can compare it with the main interest rate and find out the amount of additional overpayment.

Example of UCS calculation

Let's calculate the total cost of the loan of 1 million rubles for 2 years, at 10% per annum and with an additional commission of 12 thousand per year. Type of payments – annuity, i.e. equal shares in all periods.

The payment schedule will be as follows:

monthly payment | by principal amount | interest payments | commission | unpaid balance |

|

The total loan payment is 1 million 131 thousand 478 rubles 32 kopecks. Let's insert this figure into the simplified formula:

((1 131 478,32/1 000 000)-1)/2*100 = 6,57%.

The total cost of the loan was just over 6 and a half percent per year, i.e. 13.15% for two years.

Why is this not similar to the stated rate of 10% per annum?

Because interest was accrued only on the amount of the unpaid balance, but there was a commission charged on the original loan amount.

This simple example shows how much reality differs from what seems understandable before calculation.

How to calculate the cost of a loan online?

Calculating the full cost of a loan using a general (rather than a simplified) formula manually can be a very lengthy exercise in mathematics. Wasting time here is guaranteed, and the risk of errors is very high. But, to the delight of users, the Internet offers quite a few programs that already have all the formulas needed for calculations, and all that remains is to put your data in the appropriate forms.

In the practice of searching for a loan, calculators will be especially useful with the ability to select a loan that satisfies specified parameters, with the function of searching for a loan for the required amount and with a suitable interest rate. Here is a good example of such a calculator.

As you have already seen, comparing loans is a rather labor-intensive and time-consuming undertaking. In addition, in order to compare conditions, for example, on mortgage loans from different banks, you need to have a fairly good understanding of not only lending, but also insurance, and also be a good lawyer. To simplify the procedure, the Central Bank of Russia introduced the concept of “full cost of the loan” (previously the concept of “effective interest rate” was introduced). For deposits, the concept of the total cost of the deposit can be used.

Formula for calculating the total cost of the loan

as follows:

- d i - date of the i-th payment;

- d 0 - date of initial payment - is the date of transfer of funds to the borrower;

- n - number of payments;

- DP i - the amount of the i-th payment under the loan agreement. multidirectional payments are reflected with different mathematical signs. Thus, the payment of loan funds to the borrower is reflected with a minus sign, the return of funds and commission payments are reflected with a positive sign;

- PSK - the total cost of the loan, reflected in % per annum

When determining the full cost of the loan, all payments related to the issuance of the loan (commission for issuance, consideration of the application, etc.) are reflected in the initial payment.

What is included in calculating the total cost of the loan:

1. Exactly known payments under the loan agreement, which are payments related to the conclusion and execution of the loan agreement:

to repay the principal amount of the loan;

on payment of interest on the loan;

fees and commissions for drawing up a loan agreement, considering a loan application, issuing loan funds, opening and maintaining an account;

commissions for cash settlement and operational services

if the payment is made on a loan on a bank card - commissions for issuing and annual servicing of credit cards

2. Payments to third parties, if the obligation to pay these payments arises from the conclusion of a loan agreement

- insurance of real estate or vehicles

- payments to notary offices and notaries

- valuation of property pledged as collateral

The calculation of the full cost of the loan does not include

payments by the borrower that do not arise from the loan agreement, but from the requirements of Russian legislation. For example, to apply for a car loan, this will be compulsory motor liability insurance, which must be concluded in any case;

payments related to the borrower’s failure to comply with the terms of the loan agreement. For example, late payments;

the borrower's payments on the loan, which depend on the borrower's decision or on his behavior. For example, a commission for early repayment, a commission for receiving funds in cash, a fee for providing information about the status of the debt.

If the loan agreement provides for different types of loan accruals depending on the borrower’s decision, the calculation of the full loan amount is calculated based on the maximum possible loan amount (overdaft limit), loan term, and equal payments under the loan agreement.

Calculation example:

Basic loan terms:

| date | Interest payment | Principal payment | Commissions and other payments | Remainder debt at the end months |

|---|---|---|---|---|

| 01.01.2011 | - 50 000,00 | |||

| 31.01.2011 | 833,33 | 4 166,67 | 1 500,00 | 45 833,33 |

| 28.02.2011 | 763,89 | 4 166,67 | 500,00 | 41 666,67 |

| 31.03.2011 | 694,44 | 4 166,67 | 500,00 | 37 500,00 |

| 30.04.2011 | 625,00 | 4 166,67 | 500,00 | 33 333,33 |

| 31.05.2011 | 555,56 | 4 166,67 | 500,00 | 29 166,67 |

| 30.06.2011 | 486,11 | 4 166,67 | 500,00 | 25 000,00 |

| 31.07.2011 | 416,67 | 4 166,67 | 500,00 | 20 833,33 |

| 31.08.2011 | 347,22 | 4 166,67 | 500,00 | 16 666,67 |

| 30.09.2011 | 277,78 | 4 166,67 | 500,00 | 12 500,00 |

| 31.10.2011 | 208,33 | 4 166,67 | 500,00 | 8 333,33 |

| 30.11.2011 | 138,89 | 4 166,67 | 500,00 | 4 166,67 |

| 31.12.2011 | 69,44 | 4 166,67 | 500,00 | 0,00 |

| Total | 5 416,67 | 50 000,00 | 7 000,00 | 0,00 |

In this example, the total cost of the loan was 55,49 %

As you can see, the total cost of the loan may differ greatly from the interest rate stated and advertised by the bank. In addition, it should not be confused with such a concept as an increase in the cost of a loan, which largely depends not on the interest rate, but on the loan term.

The full cost of the loan is quite difficult to calculate using a calculator, but Excel can be a huge help in calculating it. In spreadsheets, this calculation is implemented using the IRR (internal rate of return) function. If you need to compare several programs, download

FCC (total cost of credit) shows the actual interest rate on the loan. Previously, this criterion was called the effective interest rate. The parameter takes into account not only the principal amount of debt and interest, but also almost all additional payments by the borrower according to the terms of the loan agreement (commissions, credit card fees, insurance premiums and bonuses, if insurance affects the procedure for issuing a loan). Registration fees, penalties, fines and other payments that do not affect the size and conditions of obtaining a loan are not taken into account.

Formula for calculating UCS

From September 1, 2014, a new formula is in effect for calculating the full cost of the loan. Grounds: Federal Law No. 353 of December 21, 2013 “On consumer credit (loan)” (see Article 6 “Full cost of consumer credit (loan)”).

For the new calculation of the PSC, legislators established a formula that is used in a number of foreign countries to find the effective annual interest rate (APR, or Annual Percentage Rate).

The formula itself:

PSK = i * NBP * 100 .

- NBP is the number of base periods in a calendar year. The length of the calendar year is assumed to be 365 days. With a standard payment schedule with monthly payments under the “annuity” system, NBP = 12. For quarterly payments, this figure will be 4. For annual payments – 1.

- i – interest rate of the base period in decimal form. It is found by selection as the smallest positive value of the following equation:

Let's look at the components:

- DP k – the value of the kth cash flow under the loan agreement. The amount provided by the bank to the borrower is included in the cash flow with a minus sign. Regular payments under the loan agreement are marked with a “plus” sign.

- m – number of payments (number of amounts in cash flow).

- e k – period expressed in parts of the established base period, calculated from the end of the qk-th period until the date of the k-th cash payment;

- q k – number of base periods from the date of loan issuance to the k-th cash payment;

- i – base period rate in decimal form.

Let's show the calculation with an example.

Example of calculating UCS in Excel

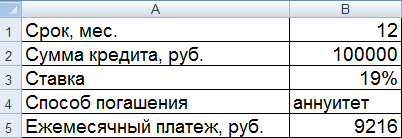

The borrower takes out 100,000 rubles on 07/01/2016 at 19% per annum. Loan term – 1 year (12 months). The payment method is annuity. Monthly payment – 9216 rubles.

Let's enter the input data into the Excel table:

Let's make the calculation:

In our example it turned out that i = 0.01584. This is the monthly size of the PSC. Now you can calculate the annual value of the total cost of the loan.

The formula for calculating UCS in Excel is simple:

The value cell is set to percentage format, so multiplying by 100% is not necessary. We simply found the product of the loan term and the interest rate of the base period.

The calculation using the new formula showed the PIC equal to the contractual interest rate. However, in this example, the borrower does not pay the lender additional amounts (commissions, fees). Interest only.

Let's look at another example, with additional costs.

Cash flow will change accordingly. Now the borrower will receive 99,000 rubles. And the monthly payment due to the fee will increase by 500 rubles.

The base period interest rate and the total cost of the loan have increased significantly.

This is understandable, because The borrower, in addition to interest, pays the lender a commission and fee. Moreover, the fee is monthly. That is why there is such a noticeable increase in PSC. Accordingly, the cost of the loan product will be more expensive.