How to control accounts receivable: methods and tools. Formula for calculating overdue receivables Norms of overdue receivables in distribution

The correct economic policy of an enterprise depends on constant analysis and effective management (hereinafter referred to as DM), which significantly affects the profitability of production. Such research suggests where there are weak points in revenue generation and then decides how to minimize their impact. Among the methods of debt management are the following: organization of clear accounting of orders; timely issuance of invoices and determination of the nature of debts.

The study of these factors requires special attention. If, for example, the receipt of funds takes too long, then you need to look for ways to reduce the time spent between the stage of selling the goods and registration for the consumer. In addition, it is also worth assessing the costs that arise due to the presence of remote sensing, because this results in lost benefits from not using funds that could have been invested. What factors should attract attention when analyzing the financial policy of an enterprise in order to organize effective management of the enterprise? This will be described below.

The need for remote sensing analysis

Various types of debt obligations of any enterprises and persons in favor of a given manufacturer are called debt obligations.

During her analysis identify all the moments of its occurrence and impact on the profitability of the organization. This is necessary to correctly determine effective management keys, as well as consider the optimal timing for providing credit to buyers. After all, the time it takes to pay off the debt has a direct impact on sales volumes and businesses. Typically, a longer repayment period for loan agreements significantly increases the quantity of products sold and vice versa.

During her analysis identify all the moments of its occurrence and impact on the profitability of the organization. This is necessary to correctly determine effective management keys, as well as consider the optimal timing for providing credit to buyers. After all, the time it takes to pay off the debt has a direct impact on sales volumes and businesses. Typically, a longer repayment period for loan agreements significantly increases the quantity of products sold and vice versa.

It has already been precisely established that the credit period for repaying the cost of goods or services directly affects the costs and income of the enterprise. At the same time, a strict payment procedure will allow you to invest less money in debt and reduce the risk of losses from non-repayment of bad debts. However, it will entail a decrease in sales volumes and, accordingly, a reduction to a minimum of profits from a negative assessment of such activities by buyers.

Due to such circumstances main goals carrying out the analysis of remote sensing data are as follows:

- Identify the characteristic features of profitability while analyzing the state and dynamics of debt and accounts payable.

- Define an effective framework for achieving improvements in enterprise debt management.

- Prevent the occurrence of bad debts in the future and optimize relationships with customers during the provision of loans to them in order to ensure stable income.

Debt arises for various reasons, so DZ is classified by these types:

- shipment has taken place, but full payment has not yet arrived;

- delay in payments for goods (services) after the deadline;

- on bills of exchange receivable;

- delay in payments to the budget;

- debt for wages and other amounts due to working personnel;

- other.

In this list, the lion's share of the total volume of debt is occupied by unpaid debts of buyers for goods transferred to them in the first three positions. The final amount for settlements with consumers usually reaches 80-90% of the total mass.

By twelve month repayment period Debt divides debt into 2 more groups:

- long-term (more than 12 months);

- short-term (up to 12 months).

Indicators of remote sensing and its accounting

In companies using accounting, DZ share for the following articles:

During the analysis in terms of its structure it is necessary to identify the specific share of funds separately for each item. At the same time, you need to pay attention to the occurrence and accumulation of overdue debt obligations, which lead to a deterioration in the profitability of the organization’s activities. Identification of such moments will make it possible in the future to more carefully assess the solvency of counterparties, as well as to more closely and accurately conclude transactions with new buyers.

Fractional parts of remote control will help you pay attention to which indicator leads to a deterioration in economic activity. They require corrective actions in the further management of financial flows.

In civil law, debt is referred to as property rights, which are secured after the lapse of time by receiving a certain amount of money or goods (services) from the debtor. Such debt assets or finances must be reflected in accounting and tax reporting as part of the company's assets.

These actions regulated the following regulatory acts of the Russian Federation:

- Civil code.

- Federal Law “On Accounting” dated November 21, 1996. No. 129-FZ.

- Tax Code.

- Regulations on accounting and financial reporting.

- Decrees of the Government of the Russian Federation.

- Code of Administrative Offences.

- Accounting Regulations “Income of the Organization” PBU 9/99.

- Accounting Regulations “Organization Expenses” PBU 10/99.

In practice, there are often cases of failure by debtor counterparties to fulfill their contractual obligations, therefore the legislation also provides for penalties for violating the terms of transactions. They are subject to civil liability and are subject to fines, penalties, penalties or high interest rates.

If you have not yet registered an organization, then easiest way This can be done using online services that will help you generate all the necessary documents for free: If you already have an organization and you are thinking about how to simplify and automate accounting and reporting, then the following online services will come to the rescue and will completely replace an accountant at your enterprise and will save a lot of money and time. All reporting is generated automatically, signed electronically and sent automatically online. It is ideal for individual entrepreneurs or LLCs on the simplified tax system, UTII, PSN, TS, OSNO.

Everything happens in a few clicks, without queues and stress. Try it and you will be surprised how easy it has become!

Remote sensing analysis methods

There are two methods for performing analysis: continuous and selective.

Which one to use depends on several factors:

Which one to use depends on several factors:

- size of debt amounts;

- volume of settlement documents;

- number of debtors.

Analyzing the debt, a number of indicators, both absolute and relative, are identified that characterize the fulfillment of debt obligations by buyers. First, the absolute indicator of overdue debts is determined. These include those debts for which the three-month period, counted from the final day of repayment, has already expired.

The significant value is . This value is determined using the formula, where by dividing the amount of sales revenue (VR) by the average DZ (AD), the desired parameter is obtained:

Kodz = VR/DZ.

In the formula, the expected amount of BP during subsequent payments is taken without taking into account the amount and excise tax.

This coefficient shows the number of turnovers that such funds make during a particular reporting period. Most often it is calculated per calendar year.

The next step is to find repayment period by dividing the number of calendar days in the reporting period (N) by the turnover ratio:

Ppdz = N / Kodz.

When determining the timing of debt repayment, attention is paid to its duration: the longer it is, the higher the risk of non-repayment of funds. If an increase in this indicator is detected, then we can judge a decrease in products (services).

Establishing the percentage of debt in the total volume of working capital is necessary for determining financial well-being enterprises. This type of debt refers to current assets and, unlike non-current ones, after a certain period it turns into the company’s finances.

Analysis shows, how high is the share of immobilized assets, which include remote assets.

The higher its percentage, the stronger the inhibition of financial processes.

Specific gravity DZ is calculated using the formula:

UVdz = Dz/Co*100,

where Co is the volume of working capital.

It is imperative to determine and share of doubtful debts characterizing the quality of all available types of receivables. With the growth of this indicator, one can judge the constant decrease in the company’s liquidity, since its ability to cover, in turn, repay loans from assets, decreases.

Share of doubtful debts calculated by dividing their sum by the total value of the DZ:

Uvsd = Ssd/ Odz* 100,

where Сз – doubtful debts.

The hidden liability that has arisen for the enterprise, formed in connection with prepayments to suppliers, is clarified during the analysis and assessment of the state of settlements.

Examples of remote sensing analysis

It is best to analyze the activities of an enterprise in terms of the structure, composition and dynamics of the overall remote control using the data in Table 1.

Table 1. Composition and dynamics of total receivables

From the table parameters it is clear that the amount of receivables decreased in 2014 in contrast to the previous year by 0.4%. This circumstance is caused by a reduction in debt among consumers of manufactured products. However, in 2015 there was a jump upward and, as a result, its amount exceeded the figure for 2014 by 38.7%. As can be seen from Table 1, the largest parameters entered in the growth rate column relate to 2 positions: settlements with consumers and tax obligations.

Since the maximum value in Table 1 belongs to the line of settlements with buyers and customers in comparison with other minor parameters, it is necessary to understand this type of debt in more detail. To do this, draw up Table 2 for settlements with consumers.

Table 2. Summary table for settlements with consumers

Here, maximum amounts are taken into account, which have a predominant impact on the overall debt structure. Therefore, table 2 consists of data from 4 counterparties of the enterprise, which are biggest debtors , and other organizations combined into a common line of other buyers and customers. The three main consumers have debt that accounts for more than 10% of the total debt. The indicators of other buyers differ significantly and have an insignificant share, but they are also analyzed.

Among the counterparty enterprises with the maximum share in the total amount of debt, the first place is occupied by company A, which reached 41.6%. It is her actions that have a predominant impact on the growth of debt in the structure of the “buyers and customers” item.

Table 3. Debt repayment terms

The compiled Table 3 indicates that the bulk of the loan receivables lies within the repayment period for 60 days. The filled-in cell parameters draw attention to a more detailed consideration of the debt from company B due to overdue and the large share of the debt, reaching 44.3%.

As the analysis progresses, the parameters of the remote control turnover must be determined. They characterize the number of turnovers of funds during transactions. The average duration of one revolution is analyzed.

The company's indicators are summarized in table 4 turnover.

Table 4. Turnover

The indicators collected in the table revealed that the duration of the turnover of debt funds has decreased over three years, which indicates a decrease in the repayment period of debt. This is a positive trend in the economic activity of the enterprise, because it leads to an acceleration of the release of finance from circulation.

At the end of all analytical actions in Table 5, a comparison of receivables and credits is performed.

Table 5. Comparison of accounts receivable and accounts payable

The resulting ratio of accounts receivable to accounts payable in the table exceeds “1.00”. Received values confirm full coverage of remote sensing above the creditor's, i.e. an enterprise can easily pay its creditors in a timely manner, and there is no need to turn to other, additional sources of financing. At the same time, the coefficient does not exceed the standard indicator “2”, which indicates a slowdown in the period of transition of the liquid part of current assets into cash.

Methods of analysis and accounting of accounts payable

Debt obligations incurred by an organization to other companies and individuals are called accounts payable.

Repayable loan payments may be the following:

- to budget or other funds;

- work team;

- enterprises supplying raw materials;

- organizations with which they are concluded;

- other creditors.

This list can also include debts to banks or other legal entities for short-term or long-term loans received from them.

Unjustified accounts payable

During the analysis it is necessary to identify the presence of unjustified accounts payable, which includes:

- overdue debts to suppliers due to unpaid payment documents on time;

- debt for materials supplied or services provided, arising due to the lack of payment documents from suppliers.

If you've already run out statute of limitations filing on the issue of payment of debt to the supplier, the amount is included in the profit of the organization that has the credit debt.

This type of debt can be in the form of either cash or in kind. Therefore, its structure includes different calculation items. It includes unclaimed deposited amounts, debts from claims, etc.

This type of debt can be in the form of either cash or in kind. Therefore, its structure includes different calculation items. It includes unclaimed deposited amounts, debts from claims, etc.

They analyze the activities of a particular enterprise in terms of the timing of receiving finance and paying debt payments. In the same way as in the loan agreement, the turnover ratio, the absolute indicator and the period for repayment of accounts payable are determined.

Identified accounts payable on the basis of clause 78 of the Accounting Regulations are subject to liability if the statute of limitations has expired. The amount is withdrawn from the accounting balance based on the readings received after the inventory. Based on the results of its implementation, a written justification is drawn up, an order is issued for the enterprise or another order from the head of the company on deregistration.

Annually subject to inventory check all settlements with suppliers, debtors and creditors. These activities are needed to ensure reliable accounting and reporting. Based on the results of the inspection, the commission reports on the identified debts with an expired statute of limitations. After this, measures are taken to write them off.

When analyzing the business activities of a company, it is imperative to carry out comparison of accounts receivable and accounts payable indicators. A positive result will be if the resulting indicator of the total debt is greater than the creditor's, which indicates successful work and effective production management. In such cases, the organization receives more finance than it spends.

However, a large difference may also indicate that there is an inability of this company to pay the invoices issued to it.

However, a large difference may also indicate that there is an inability of this company to pay the invoices issued to it.

For comparison, the following are calculated creditor indicators:

- turnover period,

- debt repayment period,

- the rate of increase in the amount of loans.

The best option for a comparative analysis is considered to be the one when the turnover ratios of accounts payable and accounts payable do not significantly exceed each other. This ensures stable profitability of the enterprise and sustainable production.

An example of receivables analysis is presented in the following webinar:

Indicative for the comparative analysis of accounts receivable and accounts payable is a special coefficient characterizing the ratio of accounts payable and accounts receivable. It is calculated as the ratio of accounts payable balances to accounts receivable balances at the beginning and end of the period under study and shows what share of the institution’s obligations can be repaid when the institution’s resources diverted to accounts receivable are received.

Online calculator for calculating penalties

Penalty is a penalty interest that a negligent counterparty is obliged to pay for late payment of a debt.The penalty is set as a percentage of the overdue amount for each day of delay.

The amount of the penalty is determined by the parties themselves when signing the agreement. For example, a penalty of 0.1% will correspond to 36.5% per annum. In the event that there have been partial repayments of overdue debt, penalties are calculated separately for each overdue payment, taking into account the number of days overdue for each payment.

Calculation of the term and amount of trade credit

What makes a company provide trade loans to its counterparty partners? Competition is forcing many companies to increasingly offer deferred payment sales to their customers. And if the purpose of deferring payment for the supplied goods or services is to increase sales volumes, then the other side of this “coin” is an increase in the volume of doubtful debts.Therefore, it is necessary to realistically assess all the advantages and losses, take into account the positions of competitors and develop the most flexible policy in this matter.

Funds received from debtors are one of the main sources of income for manufacturing enterprises.

In an unstable market economy, the risk of non-payment or late payment by customers of invoices increases, which leads to the appearance of receivables. The appearance of accounts receivable leads to a shortage of funds, increases the organization's need for current assets to finance current activities, and worsens the financial condition.

Calculation of accounts receivable turnover

The formula for calculating accounts receivable turnover from textbooks on financial analysis has shortcomings, and in practice, financiers make mistakes when applying it. We offer an adjusted calculation methodology. RTD – receivables turnover period in days; DZn and DZk – its size, respectively, at the beginning and end of the period in rubles; B – revenue in rubles; CD – number of days in the period.Cunning numbers: why it is not enough to know “plan” and “fact” to calculate KPI

Oleg, good day. I decided to join the discussion.1. A good article due to the use of specifics in the description of the model.It becomes clear what they wanted to say with their calculations.2.

I think your concept of a “base” is a good point for limiting and clarifying the calculation of an employee’s effectiveness.

As I understand it, the specifics of the calculation formulas and the base itself are the lot of the managers of a particular enterprise themselves.3.

According to accounting standards, accounts receivable are defined as amounts due to a company or other person from customers or other debtors. The most common type of receivables is the debt of buyers and customers for goods, materials, services supplied to them, work performed and not paid for on time; the excess of debt on loans issued by the organization to its employees over loans received for these purposes.

Planning and Economic Department

“from the last paragraph of the calculation it follows that there is a threshold at which it is not at all profitable for the manager, having arrears of 300,000, to reduce the total amount of debt (1,300,000) at the expense of solvent clients, becausein this case, its coefficient will decrease!

rather, it is more profitable for him not to take money from solvent clients. Then such motivation is not in favor of the employer. PDZ must necessarily participate in motivation!

I’m looking for an answer to what to “link” it to in the calculation?” Tatyana Answer: I will quote the paragraph in question: “Let out of 1,300,000 rubles.

Analysis of receivables and payables

The level of accounts receivable is determined by many factors:- applied forms of non-cash payments for these products

- type of product for which payments are made

- degree of market saturation with this type of product

- market capacity

those. change in its size over the analyzed period; consider its composition.

This page presents the structure of the regulations for the defining activities carried out by various officials of the company, within the framework of a single process of control and collection of receivables.

The specified document is an element of the enterprise's accounts receivable management system.

Regulations for the control of receivables (hereinafter referred to as receivables) and collection of overdue receivables (hereinafter referred to as receivables)

1. Purpose of the Regulations.

This Regulation is intended for:

- Systematic prevention of the occurrence of overdue receivables (hereinafter referred to as ORD), prevention of the occurrence of irrecoverable and chronic receivables.

- Reducing the average time of delays and reducing the average volume of delivery orders.

- Maintaining the size of the maximum permissible limit within the planned and normative values.

2. Scope of application of these Regulations.

2.1 These Regulations apply to all clients working with deferred payments and to all cases of occurrence of DZ and PD, regardless of categories of clients, except for cases for which there is a written order from management to completely or partially exclude them from the scope of application of these Regulations.

2.2 The Regulations come into force from the moment the client has a liability to the organization (that is, from the moment he receives the first shipment of goods on deferment).

3. Classification of clients (statuses) and their defining characteristics.

Based on settlement and payment discipline, when repaying debt, all clients of the organization are assigned 4 main categories or statuses:

3.1 Reliable payers- clients who, having a deferred payment over a one-year period, have never been late in returning their debt, or have made no more than 2 delays lasting up to 1 week, with a preliminary warning of the delay and agreement on the terms of debt restructuring.

3.2 Clients with uncertain reliability- clients for whom there is no statistics of interaction on PD during the previous one-year period, or clients for whom payment statistics are unstable. That is, in up to 50% of cases there is a delay for periods of time (from 1 to 2 weeks), with or without warnings, while there is always consent to debt restructuring.

3.3 Clients at risk of delinquency- clients who allowed during the one-year period:

- one-time delays for periods longer than 1 month;

- more than 1 (one) delay per month for periods of more than 2 weeks, mostly without warning;

- delay of up to 1 month in more than 50% of cases;

- avoidance of contacts and opposition to the terms of debt restructuring he proposed.

3.4 Non-paying clients- clients:

- those who had a history of interaction over the past year period of more than 1 (one) delay in payment of debt for a period of more than 2 weeks, without warning, protested against the proposed conditions for debt restructuring and allowed evasion of contacts;

- with whom legal proceedings have already taken place;

- to whose address letters of claim have already been sent.

4. Assigning initial categories (statuses) to clients.

4.1 Initial categories (statuses) are assigned to clients at the beginning of the calendar year, based on the history of interaction with them and statistics on timely/untimely repaid debts to the company, taking into account the criteria given in clause 3.

4.2 The assignment of customer categories is carried out jointly by the Head of the Sales Department (ROD) and the Head of the Financial Control Service (RSFC), then approved by the Commercial Director (CD) of the enterprise.

4.3 Depending on the status (category) assigned to the client, the following terms of delivery/payment for goods provided by the organization are automatically established for him:

| № | Client status | Initial terms of cooperation |

| 1. | Reliable payers | |

| 2. | With uncertain reliability | Shipment limit:__;discount:__;deferred payment duration:__. |

| 3. | Clients threatened due to late payment (non-payment) | Shipment limit:__;discount:__;deferred payment duration:__. |

| 4. | Non-paying clients | Shipment limit:__;discount:__;deferred payment duration:__. |

4.4 Over time, depending on the statistics of payments and delays, the client’s category may change, both upward and downward, and along with it, the delivery conditions established for this client will also change.

4.5 Monitoring payment statistics and changes in clients’ credit history is carried out jointly by the Head of the Sales Department (ROD) and the Head of the Financial Control Service (RSFC).

4.6 Review (confirmation or change) of client statuses (categories) is carried out based on the results of 3 months of interaction, also by the Head of the Sales Department (ROD) and the Head of the Financial Control Service (RSFC).

5. Proactive actions.

5.1 The main working documents for monitoring the dynamics of remote receivables/receivables are: 1C report on receivables of counterparties, route sheet and payment history.

5.2 In relation to new clients (clients for whom there are no statistics because work has not been carried out with them previously), in order to have an adequate understanding of their solvency, Sales Representatives (TRs) must, at a minimum, collect information about the personal data of the owner, manager and Decision maker, about which a note is made on the client’s card.

5.3 Also, without fail, the TP is required to enter into the card the status of the outlet, availability of goods, location, brand representation, price level and inventory (to determine the safe shipment limit).

5.4 To select the terms and conclude the Agreement, the Sales Representative is required to have the following package of documents:

- A certified copy of the Certificate of state registration of a legal entity.

- Certified copy of Legal Registration Certificate. persons at the tax authority.

- A certified copy of the Certificate of entry into the Unified State Register of Legal Entities.

- Extract from the Unified State Register of Legal Entities no later than 30 days.

- A certified copy of the charter (information on the size of the authorized capital, location of the enterprise or private enterprise, competence and terms of appointment of the director).

- A certified copy of the protocol or decision on the appointment of the head of the enterprise.

- Letter requesting a deferment agreement.

- Details of the enterprise and personal contact information about the top officials of the enterprise (Director, Chief Accountant, Merchandiser, Purchasing Specialist), indicating work, home and personal mobile phones.

In the absence of at least one of the points listed above, the decision to conclude the Agreement is made personally by the General Director.

5.5 For clients who have previously been late in repaying their loan payments, employees of the Sales Department (SD) apply advance warning of the due date of payment, however, depending on the category assigned to the client (see P 4 of these Regulations), the intensity of the reminder should be different.

| Category (client status) | Reminder intensity |

| Reliable clients | A reminder may be omitted altogether, or a one-time reminder 1-2 days before the payment is due is sufficient. |

| Unspecified clients | 2 reminders 4 and 2 days before the payment is due. |

| Threatened clients | At least 3 reminders 7, 4, 1 days before the payment is due. |

| To defaulters | Deferred payment is not available |

5.6 Warning calls are made by TP as planned, every Friday, in relation to clients who have a payment due date in accordance with the Agreement next week.

6. Monitoring the dynamics of remote sensing and critical sensing

6.1 Performed by sales representative.

6.1.1 Communication with the client during the visit preceding the payment due date: During the visit preceding payment, the TP, after completing the main goals of the visit, reminds the decision maker (hereinafter referred to as the decision maker) of the Client about the deadline for the upcoming payment, indicating the date, number, amount of the payment invoice, form of payment. Then, based on clause 5.1, it is checked with the Client’s data.

6.1.2. TP analyzes the Client’s behavior in relation to the debt.

Options:

| a. | The Client’s behavior and the state of the outlet do not raise doubts about timely payment. | Specifies the time and date of contact (based on the route sheet). Thanks the Client for his constructive approach and says goodbye. |

| b. | The Client’s behavior and the state of the outlet raise doubts about timely payment. |

Specifies the time and date of the contact (based on the route sheet). Thanks the Client for understanding that timely payment is an important element of the working relationship, says goodbye to the Client. Makes a note in the route sheet about the need to remind the Client about payment in advance. If necessary, requests assistance from the supervisor (hereinafter referred to as SV) in achieving the goal. |

| c. | The Customer's behavior and the state of the outlet indicate a high risk of loss of funds (hereinafter referred to as DS). | Immediately informs the immediate supervisor about the current situation. Coordinates further actions with the immediate supervisor and follows his instructions. |

6.1.3 Communication on the day of payment:

- After greeting and establishing a positive contact with the decision maker, he indicates, as one of the goals of interaction, payment for the current invoice (indicating the date, number, amount).

- Variant situations:

| a. |

The client pays for the delivery |

Records the receipt and transfer of funds. Thanks the Client for the timely fulfillment of obligations (in the situation of non-cash payments, specifies the date, number, amount of the payment order). Moves on to the next purpose of the visit. |

| b. | The client requests an additional delay |

1. Clarifies:

2. Analyzes the Client’s behavior in relation to the debt. |

| a1 | The credit history is beyond doubt (reliable payer), the Client’s behavior, the state of the outlet does not raise doubts about the execution of agreements |

Agrees on the time and date of contact (no more than five days from the current moment, a period of more than 5 days is agreed with the immediate supervisor), the amount and invoice number. Expresses the hope that the agreements will be implemented on time. Makes an appropriate note on the itinerary sheet and proceeds to the next stage of the visit. |

| b1 | The outlet has a new or credit history, the Customer’s behavior, the state of the outlet raises doubts about timely payment (a client with uncertain reliability and a client at risk of being overdue). |

Sets the time and date of contact, amount and invoice number (no more than three days from the current moment, a period of more than three days is agreed with the immediate supervisor). If the Client:

|

| c1 | The Client’s behavior and the state of the outlet indicate a high risk of losing the DS (regardless of the client’s status). | Immediately (at the point of sale) informs the immediate supervisor about the current situation. Coordinates further actions with the immediate supervisor and subsequently follows his instructions. |

6.2 Performed by supervisor.

(Working documents: 1C report on contractors’ debts, weekly work plan, checklist, route sheets, etc.)

- Personally monitors late payments for more than 5 days from the date of payment under the contract; in case of a delay of more than 10 days, he submits a memo to the NOP with a report on the work done and a request for further collection from the defaulter.

- At the end of the working week, analyzes the situation with overdue receivables of subordinates, plans (with inclusion in the operational plan) measures to eliminate late payments in the form of:

- individual or group work with a sales representative in the office. Including sending a sales representative to a training group on the topic: “Negotiations with a debtor client”;

- individual work with a sales representative in the territory;

- a telephone call or personal visit to the debtor Client;

- coordinated interaction with the SFK employee.

6.3 Performed by the head of the sales department

(Working documents: 1C report on accounts receivable from counterparties, weekly plans for supervisors, work plans for the week, operational plan for the month.)

1. Personally controls and takes part in the process of collecting late payments lasting more than 10 days from the date of payment under the agreement.

2. Checks the weekly work planning of sales department supervisors (hereinafter referred to as OP), to see if there are any measures in the plan to reduce debt and work with debtor clients.

2.1. Monitors in daily reports (checklist) the actions of TP and SV in situations of late payment, including the availability of training goals.

3. Based on the results of monitoring the work of the department, the NOP from days 10 to 15 makes a decision on:

- providing the SV with an additional period of time to collect the maximum allowance;

- unconditional recovery of funds. In this case, a memo is drawn up to the immediate supervisor with a report on the measures taken to return the PD.

4. Plans and reflects in the operational plan measures to reduce the percentage of late payments in the OP.

5. Determines, based on an analysis of work for the period, the planned percentage of late payments for the month and approves it by the Director.

6.4 Director of LLC

(Working documents: 1C report on accounts receivable from counterparties, supervisors’ route sheets, monthly operational plan for the head of the sales department (HOP), personal operational plan.)

1. Personally controls the process of returning late payments of more than 15 working days from the date of payment under the contract.

1.1 Within 10 calendar days from the date of the deadline under clause 1. decides on:

- providing the NOP with an additional period of time to collect the maximum allowance;

- inclusion of a task for a specific PP situation in the SFK employee’s plan;

- debt restructuring (partial return of goods, compensation with other goods, additional deferment with payment of penalties);

- change in the client’s reliability status and subsequent change in commercial conditions in the 1C program;

- unconditional collection of funds;

- transferring the PD to the irrevocable PD database.

2. Monitors the presence in the operational plan of the NOP of measures to reduce accounts receivable (RA) and work with the Client as a debtor.

3. Approves the acceptable planned percentage of late payments for the next month of the OP.

6.5 Legal department

- Based on the request of the OP, SFK or instructions from the director of the LLC:

- draws up claims to counterparties and debtors;

- organizes work to collect the maximum allowance in accordance with the current legislation of the Russian Federation and the requirements of the company’s internal standards;

- keeps records of work with PDZ in the network diagram.

7. Cost of delay and terms of debt restructuring

7.1 By decision of the management of the LLC, before the formal filing of the claim with the court, a delay of no more than 3 calendar weeks (or 15 banking days) from the date of the delay is allowed. In other words, after 4 calendar weeks or 20 banking days, the overdue payment must be repaid, a debt restructuring program must be adopted, or the client must be transferred to the South Ossetia and the SFK to ensure the claim procedure for collecting the PDZ.

7.2 This period of time is a resource for the work of sales representatives, supervisors and the head of the sales department to resolve the issue pre-trial in the interests of both parties and agree on the restructuring of overdue debt.

7.3 Delay in repayment of a loan is actually a commodity lending to the defaulting client, therefore, if the client changes the repayment terms of the loan, it will also be fair to change the terms of payment for the overdue amount.

7.4 If the client agrees to restructure the overdue debt, an additional agreement to the current Agreement is concluded with the client, according to which the following table applies:

|

Overdue time (months-weeks) |

1st month | 2nd month | ||||||

| 1 week | 2 week | 3 week | 4 week | 1 week | 2 week | 3 week | 4 week | |

|

Late price (% of the amount) |

1.5 | 3 | 4.5 | 6 | 2 | 4 | 6 | 8 |

7.5 At the same time, the competence of the sales representative managing this client includes the ability to exclude payment for late payments during the 1st week of delay (if full repayment of the DZ takes place within this week).

7.6 The ability to exclude payment of late payments for the second week (at the oral request of the leading client of the sales representative and subject to full repayment of the payment for this period) is within the competence of the Head of the Sales Department.

7.7 Other decisions on the provision of benefits and exceptions are within the competence of the LLC Director.

7.8 In case of partial repayment by the client of the arrears indicated in the table (clause 7.4 of these Regulations), the rate will be charged on the outstanding balance of the PDZ.

8. Enforcement measures in case of late payment

If the scheduled payment is not received on the appointed day, and there is no warning from the debtor, the following actions are taken:

| № | Action | Purpose of action | Executor |

| 1. | Contact the debtor, notify about the lack of payment and the occurrence of arrears under the Agreement, find out the reason for the lack of payment and the actual repayment period of the debt. | Notify the client about his violation of payment discipline. Clarify the circumstances of the delay and evaluate the client’s behavior. | Sales Representative |

| 2. | Based on the repayment terms of the PDZ indicated by the client: notify the client about the proposed restructuring conditions and request a letter of guarantee from him indicating the repayment period of the PDZ and the obligation to reimburse payment for late payments. Agree on a date for the meeting and exchange of documents. | Agreeing with the client on the conditions for restructuring the sales contract, changing the initially provided delivery conditions, launching the restructuring process. | Sales Representative |

| 3. | Make a reconciliation report, changes/additions to the supply agreement (with restructuring conditions). Meet with the client and finalize the terms of the restructuring. | Receiving from the client a written request for a deferred payment, indicating a new payment deadline and guarantees of reimbursement of not only the main cost, but also payment for late payment. | Sales representative, supervisor |

| 4. | If the client avoids contact, hides, refuses to give explanations or indicate reasonable terms for repayment of the PDZ, as well as refuses to discuss the terms of restructuring the PDZ, the following is delivered to the client’s address (in person against signature or by a valuable letter with notification):

If full or partial payment is not received on the appointed day, and the client still does not engage in dialogue, then the claim is processed, and the day the letter of demand is delivered to the client becomes the beginning of the 30-day period established by current legislation for pre-trial settlement of the issue. |

Exerting measured pressure on the client in order to force him to enter into a dialogue on restructuring the property liability or its repayment. |

Sales representative, supervisor, NOP, SB, Lawyer |

| 5. | If the client repays part of the TDS, but still does not enter into dialogue, repeat step 3 or steps 3, 4, taking into account the remaining outstanding amount of the TDS. | Exerting repeated dosed pressure on the client in order to force him to enter into a dialogue on restructuring the payable liability or its repayment. | Sales representative. |

| 6. |

If the client makes contact, participates in dialogue, accepts the terms of the restructuring, however, does not comply with them with a warning and asks for a deferment again, such a deferment can be granted to him:

|

Encouraging a conscientious client approach to the terms of the contract, a dialogue mode for solving problems and readiness to accept the terms of the restructuring. |

Head of Sales Department, Director of LLC |

| 7. | Resolving the situation pre-trial (settlement agreement) and in court. | Compulsory collection of traffic regulations and corresponding penalties. |

Lawyer, SFK, Director of LLC. |

Familiarization sheet

In accounts receivable analysis, some tasks that at first glance seem complex often turn out to be simple. You just need to understand their essence and use Excel to solve them. Let's learn to identify from the general list those clients whose debt amount is greater than legal costs.

Calculation of the number of overdue days

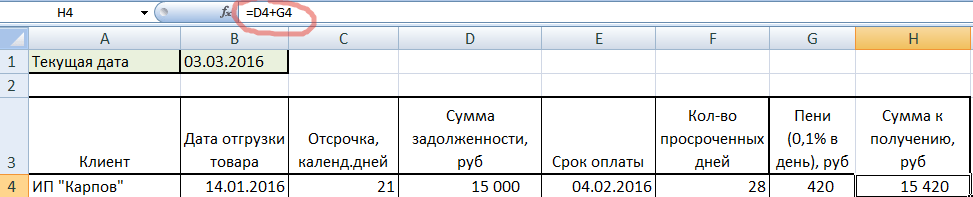

A situation where it is necessary to identify customers with debt may arise in an enterprise that works with deferred payments. That is, for example, the goods are shipped on the 1st, and the buyer is given a delay of 2 weeks. Those. he must make the payment by the 15th. Let's create a basic accounts receivable report in Excel to understand the principle.

In cell B2, the current date is written not in numbers, but in a formula, so that when opening a document the current date is always entered. The column with the dates of shipment of goods is presented in the DATE format, and with the amounts of debt - in the financial format.

To calculate the number of days overdue on accounts receivable, you need to subtract the current date from the actual date on which the payment should have been made. Let's add another column in which we write a simple formula: add the number of days of deferment to the shipment date. And extend the formula to the end of the table.

According to the receivables, it turned out that IP “Karpov”, for example, should have paid the debt on February 4, and today is already March 3. But the individual entrepreneur “Strigunova” still has 6 days to pay, because... its deadline is March 9.

Now let’s count the number of overdue days, not forgetting to change the format of the cells of the new column to numeric.

Those. from the current date we subtracted the payment date and obtained the number of days overdue. Note that cell B1 is absolute (enclosed in $ signs), so it remains the same as you drag through the formula. By the way, we got two negative values. This means that IP “Strigunova” and IP “Malyshev” still have 6 and 2 days, respectively, to make payments.

Calculation of penalties for the period of delay

Client delays should not go unpunished. Therefore, we charge a penalty of 0.1% for each day of delay. Let's multiply 0.1% by the amount of debt and the number of days overdue.

We will hide two clients without debt, highlighted in red, for now. But we won’t remove it from the list, so that when you open the same document a week later, the debt will be calculated automatically. Select both lines, right-click and select HIDE.

The broken sequence of lines reminds us that we have two more clients.

Calculation of the refinancing rate on the settlement day

The second option for calculating interest on the debt amount is depending on the refinancing rate on the day of settlement. Let's say it's 10%. We multiply the rate by the number of days overdue and the amount of debt divided by 365.

We see that the penalties with this calculation turned out to be less than with the addition of 0.1% for each day of delay. Therefore, we conclude which method of calculating interest is more profitable to indicate in the contract.

How to identify unscrupulous clients

The main thing remains: to identify the desired clients. First, let's add up the debt and penalties accrued at 0.1%.

Let's assume that legal costs are 5,000 rubles per client. Let's calculate below the amount that we can receive after filing a lawsuit against those who have a debt of more than 5000. To do this, we will need the SUMIF function.

First argument: the range in which the criterion will be searched. Second: the actual criterion, (>5000). Third: summation range (it coincides with the first). And don’t forget to subtract the hidden Strigunova and Malyshev (H12 and H13). We get 73984 rubles.

To quickly determine who should be sued, you can use the IF function. Let's write it in a new column.

You can read the formula like this: if the total amount of debt exceeds 5000 rubles (H4>5000), then we take it “to court”. Otherwise, we output a space. Thus, we have identified clients whose amount of debt exceeds legal costs.

- Good afternoon! Your payment has arrived today, but we haven’t seen the money.

- And what?! Today is just the payment day. We'll put it up for payment next week. More likely…

This is how it is in Russia - very often the payment date is determined by an authorized person or the current situation, and not by the terms of the contract. In the current economic climate, payment discipline has certainly not improved. I won’t say why it is important to have liquidity of working capital - and without financiers you can bend a lot of obvious fingers.

The technique that I will describe below is universal and easy to use, like a script. Consists of 2 main blocks: control algorithm And tactics for dealing with objections. Let's start with the algorithm:

8 stages of the algorithm for monitoring overdue receivables (APR):

- Call 2-3 days in advance and notify about the upcoming payment. Responsible – manager;

- On the day of payment - clarification on the fact of payment. Responsible – manager;

- Lack of payment and/or delay of 2-3 days. Find out the date of the planned payment, emphasis on the importance of compliance with the obligation, control. Responsible - manager;

- Delay of more than 5-7 days / notification from the Buyer of a significant increase in the payment period / violation of the agreed payment deadline. Finding out the reasons, contacting the decision maker regarding payments, arguing the need for payment. If, conditionally, there is no payment on the next day, it is necessary to receive from the Buyer a letter of guarantee with an agreed payment schedule (with a stamp). Responsible: manager, supervisor (control);

- Delay of more than 7 days without receiving a payment schedule / violation of the payment schedule. Sending a notice of violation of the terms of the contract indicating the number and points relating to payment. Responsible: manager, supervisor, lawyer (filling out the notification);

- Overdue for more than 12 days. Collection of documents necessary for drawing up a pre-arbitration claim. Responsible - manager;

- Overdue for more than 14 days. Drawing up and sending a claim by mail with acknowledgment of receipt, by e-mail. Search for a settlement solution with the Buyer's decision maker. Notification from the director (com/finance/sales). Responsible: lawyer, manager;

- Overdue for more than 28 days. Legal formalities have been completed. If your management decides, you can sue.

If the periods are plotted on a chart and signed, it will be much more readable. If you can't handle it, write to PM, I'll send it :)

Of course, the timing may vary, but a delay of more than 1 month is completely suspicious. There is a risk of later discovering a company on the way to bankruptcy or new owners registered in Dagestan. It is important to learn how to get real answers and not fall for the following speech modules:

“We put you on payment”– if repeated 2 or more times, request a payment order, otherwise apply the algorithm;

“I have submitted you for payment, please wait”- can be overcome with persistence or demand access to the decision maker regarding payments;

“We have rent, taxes, salaries, loan payments”- do not forget that your employer is in an identical situation and do not give in;

“Your turnover is poor, you ask for money in advance of sales”- disagree, look for solutions in reducing the next deliveries in quantity, rotating the assortment to a more liquid one (ABC analysis) or holding promotions. You didn't sign up for these contractual obligations;

“There is no money because there is no trade”— it is important to understand the situation regarding your products. Often, the realized funds of one supplier are used to pay for the supply of products from another, less liquid one. And if in this case your products are liquid, this is leverage. As a last resort, it is easier to take away part or all of the products. And sometimes it turns out that the product has already been sold! Where is the money, Zin?!

The buyer always pays faster and more to those who (1) are important to him and (2) who achieve this more actively than others. I hope that in terms of strategic importance you have already shown and proven your importance. Therefore, we are working on the second one - this is not begging, but a requirement to keep your part of the deal, don’t forget.

What is the best tactic for dealing with arrears? There are several options with humorous names.

6 tactics for dealing with objections to overdue accounts receivable (AR):

- “Good already” – product limit so that the client does not collect more than he can sell and pay for;

- “Not like a boy” - this is the same “stop shipment” before payment. Although recently it is better to reduce large receivables gradually, implementing the principle of “50% shipment for 100% payment”;

- “Put on the counter” – imposing fines and penalties. Court. It works, yes, but it is usually rarely possible to continue cooperation after this tactic;

- “You - to me, I - to you” - the provision of some additional preferences or concessions from the Supplier for making a payment. In regional networks, Suppliers often hear offers to carry out promotions that are not entirely profitable, which will help them see their money faster. Although it is always better to come to an agreement, this is already on the conscience of the Parties;

- “Take it to heart” – “If you don’t pay, I will be left without a bonus. Why are you doing this to me!? What did I do wrong to you!?” etc.;

- "Have a conscience!" - “We always met you, tolerated delays, got into the situation. Now we have N containers at customs, we are collecting money for salaries and taxes - pay today, we are partners!”

The main rule here is not to make boring calls “when will you pay?” Every call you make should be an event, because you really need to get this money urgently. Record every agreement, monitor and ensure its implementation.

Write the most effective techniques and interesting examples in the comments!