Amount of tax deductions. Deductions from employee salaries

– basic income. By law, it is considered as profit, which means it is subject to taxation. These standards also apply in the Russian Federation.

It is wage taxes that replenish the state budget, which ensures the smooth operation of the state apparatus.

The first thing to do is to divide taxes into those that are paid by the employer before the salary is issued, and those that must be paid after it is issued. It is by dividing taxes into these two types that it is sometimes believed that there is only one tax - income tax (personal income tax), 13% of the salary, since, although regarding the salary itself, it is usually paid by the employer, but for income received independently it is then paid and the citizen himself.

In fact, this is not at all true: it’s just that all other payments are made before the money reaches the employee’s hands, and therefore are seemingly invisible to him. But nevertheless, the employer pays the state in the same money that he could instead pay the employee, and therefore the division is purely technical. The employer determines whether to hire this or that employee and how much to pay him mainly based on what the balance of the income he brings and the expenses for him will be - and expenses also include everything. Thus, whether the employee pays the tax himself or the employer for him, this is actually done out of the employee’s pocket, which means that you can find out what percentage of the salary the taxes make up only by summing them all up.

In addition to income tax, which everyone already knows about, and about which it is often customary to ask the authorities where 13 percent of the salary goes, the following payments are also made:

- (PF);

- to the Social Insurance Fund (SIF);

- to the Health Insurance Fund (FFOMS).

What payments are taxable?

In addition to the basic salary itself, any bonuses, allowances, as well as territorial coefficients are subject to tax. In fact, any accruals from the employer must be subject to taxation (we will talk about deductions separately).

Tax amount

Let's look at the amount of each tax separately, and then illustrate all this with an example of calculating exactly how much will be paid from the salary of an ordinary employee.

Personal income tax

How, will depend on whether the recipient is a resident of the Russian Federation or not. For the former, the rate is set at 13 percent of the salary, and for the latter – 30 percent. There is also such a thing as a tax deduction. If a citizen has the right to a deduction, then the deduction must be made taking into account this deduction.

Let's give an example. An employee has three children, and if for the first two he is entitled to a deduction of 2,800 rubles (1,400 for each), then for the third one another 3,000 is added to this. Thus, the total amount of the deduction will be 5,800 rubles. If the salary is 30,000, the calculation will be as follows:

(30,000 – 5,800) * 0.13 = 3,146 rubles payable.

Without it, it would be necessary to pay 30,000 * 0.13 = 3,900.

That is, the real amount of the benefit received is far from being so impressive and in this case amounts to 754 rubles.

Standard tax deductions and the list of persons entitled to them are described in Article 218 of the Tax Code.

But it is worth noting that in order to receive a benefit, you need to contact the tax office, and the deductions themselves can be received if a citizen has incurred expenses for treatment, the purchase of real estate (both immediately and with the use of a mortgage), education, and so on.

Other taxes

To find out what percentage of the salary the taxes make up in total, let’s consider other deductions levied from. Their difference is that if income tax is formally levied directly on the employee, on his income, then the rest is paid by the employer. All together, these taxes (excluding personal income tax) amount to a little less than a third of wages. This:

- Contributions to the Pension Fund. They make up 22% of wages. In the future, it is these funds that will be used to pay the employee’s pension. That is, the salary for calculating a higher pension should also be as high as possible - it is provided by the citizen himself. If earlier payments were divided into two parts, which formed a funded and insurance pension, now all funds form the entire insurance pension.

- Contributions to the Federal Compulsory Compulsory Medical Insurance Fund, that is, the tax levied on wages that is used to provide health insurance for an employee. They make up 5.1%.

- Contributions to the Social Insurance Fund – another 2.9%. This money is used for insurance in case of temporary disability and when it occurs, payments will be made to the Social Insurance Fund. In addition, an additional contribution for insurance against accidents at work may be established - it depends on the nature of the work.

43% and more are spent on wages, which consists of: 13% personal income tax, 22% for pensions, 5.1% for medicine, 2.9% for insurance. And, of course, in addition to this, the citizen will then have to pay other fees, such as: property tax, VAT included in the price of each product purchased and other fees.

Holding order

As the Tax Code indicates, tax withholding is carried out by citizens' tax agents - that is, enterprises or individual entrepreneurs paying taxable income.

Taxes are withheld upon each payment. There is a limit on the total amount of deductions - they should not be more than 50% of the payment itself.

How exactly and in what order they are produced is an important topic for the accounting department of an enterprise. It’s worth starting with the fact that each deduction from wages is carried out in accordance with a certain basis specified in the Labor Code or other federal laws. Based on the types of grounds, deductions are divided into:

- mandatory;

- carried out by decision of the employer;

- carried out by agreement between the employee and the employer.

They are deducted exactly in the stated sequence. Let's look at mandatory deductions - these include taxes. Here the order will be like this:

- tax payments;

- payments under other executive documents.

Calculation example

Let us illustrate what was said earlier with an example of a calculation, from which it will be clear not in percentages, but in rubles, exactly how much taxes have to be paid every month.

For example, let’s take a citizen with a salary of 40,000 rubles. Now let’s calculate what taxes will be charged on it. To calculate 13 percent of your salary, you need to multiply it by 0.13. Other calculations are carried out in a similar way:

- Personal income tax – 40,000 * 0.13 = 5,200 rubles;

- to the Pension Fund - 8,800;

- in the Social Insurance Fund - 1,160, and an additional 0.2% is charged - 80 rubles.

- in the Federal Compulsory Medical Insurance Fund – 2,040.

Note that when working, accident insurance charges significantly more.

As a result, it turned out that the state had to pay 17,280 rubles, while the employee received 34,800 (that is, 40,000 minus personal income tax). The total amount spent by the employer was 52,080 rubles. Over the course of a year, the state will receive payments from this employee for a substantial amount of 207,360 rubles, and the total amount of payments from the enterprise will be 624,960.

But this was an example for an enterprise that maintains accounting according to the general taxation scheme. In addition, there is a simplified system (STS) according to which individual entrepreneurs work. Let's do the calculations for them too.

To do this, let’s take as a basis the same amount of monthly earnings of 40,000 rubles, that is, 480,000 per year. Taxes will be as follows:

- 6% of turnover (for which 480,000 is taken here) – 28,800 rubles.

- Fixed payment to the Pension Fund – 23,400;

- and the Compulsory Medical Insurance Fund – 4,590.

There is also an additional payment for exceeding the annual income level of 300,000 rubles: it is 1% of the amount of annual income, from which 300,000 have been previously subtracted. That is, in our case, the calculation will be as follows: (480,000 – 300,000) * 0.01 = 1,800 rubles.

As a result, the amount of tax payments for the year will be 58,590 rubles, which is much less than in the previous case.

You might be interested

According to Russian laws (Labor Code, Tax Code of the Russian Federation, Federal Law No. 212), the employer must pay taxes for employees. And this applies to all companies and enterprises. It is thanks to this that funds flow into the treasury. What taxes the employer pays for the employee is described in the article.

There are several contributions that must be paid for employees. Whether an employer pays taxes for an employee depends on his or her integrity. This is also checked by regulatory authorities. How much taxes does the employer pay for the employee? The main ones are 4.

Personal income tax

This is the first answer to the question of what taxes the employer pays for the employee. Personal income tax is a direct tax. It is calculated as a percentage of total income. Personal income tax is paid on all types of income received by citizens during the year. These include bonuses, fees, profits from the sale of real estate or other property, winnings, gifts, sick leave. Exceptions are cases when no tax is deducted from profits.

The basic rate is 13%. For some types of profit received, the rates are different. The main share of the tax is transferred to the budget by the tax agent. The profit that was received through the sale of property is declared independently. Although the employer pays the personal income tax himself, financially it falls on the employee. The levy is collected from the salaries of all working citizens.

NFDL is transferred to the treasury on the day of salary or other income. The exception is wages, which are paid at the beginning of the month. On the date of payment of the advance, personal income tax should not be withheld. The advance is taken into account in the final settlement with the employee. Income tax is collected from the employee in the case of official employment.

Contributions to the Social Insurance Fund

What other taxes does the employer pay for the employee? These are fees to the Social Insurance Fund. Distributed funds provide citizens with the right to receive benefits in some cases. For example, when:

- Disability.

- Loss of a breadwinner.

- The birth of a child.

- Retirement age is approaching.

Payments are received by low-income and large families. Compared to personal income tax, deductions are paid not by employees from their salaries, but by employers. When calculating staff salaries, the company must calculate the percentage for contributions to the Social Insurance Fund for a specific amount. The employer should send funds to the funds in a timely manner. Otherwise, due to late deductions, you will have to pay fines.

There are deductions:

- Actual.

- Conditional.

Actual royalties mean they are paid to a third party. These deductions include state and non-state funds. Today, taxes paid by the employer for the employee are transferred to the Pension Fund, as well as for health and social insurance.

Income from these deductions goes towards benefits in case of accidents during a person’s working activity. They are then provided by social funds. Contingent deductions do not involve the involvement of a third party; they are used to ensure that the employer provides a decent standard of living for employees who are dependent due to injury. To determine the amount of deductions, you need to apply the actual value of payments made in the previous year. Dependent persons are entitled to:

- Benefits provided after accidents.

- Compensation for moral damage.

- Child care payments.

- Benefits for company employees during layoffs.

Today, contributions amount to 2.9% of the salary level. Since not all employers are honest, evasion of payments is common. If, upon retiring, an employee discovers that he worked under an employment contract, but the employer did not contribute funds to the fund, even if an unscrupulous employer was caught, the employee will still receive a pension.

How is the amount in the Social Insurance Fund for accidents calculated? First, the amount of contributions is calculated for employees who are registered in the institution and receive a salary. Then funds from citizens working in the organization temporarily, but with whom a civil contract has been concluded, are added to the amount.

The amount of benefits paid to FSS employees in the reporting month is deducted from the entire amount. Accident insurance fees are calculated as a percentage - 2% of salary.

Deadlines

The payer of this fee (employer) pays it at the end of the reporting period. The following time frames apply for employers:

- 12 months before 31.12.

- One month before the 15th day following the reporting month.

For insurance against injuries at work, premiums are calculated monthly within the deadlines established for receiving wages from the bank for the previous period. When transferring fees, the employer should not make mistakes in the BCC, in the name of the company or bank. Otherwise, the payment obligations are not fulfilled.

If the deadline for payment of fees is a non-working day, then payment is transferred to the next working day. But the rule does not apply to all contributions. For example, payment for injuries is provided in advance: if the last day was a weekend, then payment is made on a working day that is close to a non-working day. Fees are recorded individually for each employee. It is important to timely pay the taxes that the employer pays for the employee. Otherwise you will need to pay 5% of the amount.

Pension Fund

What taxes does the employer pay for the employee, besides the basic ones? Contributions are determined by salary level. Taxes are paid if a person works in a permanent job, part-time, or on the basis of fixed-term employment agreements. What is the tax amount for an employee? It is 22% of the salary. Pay fees to the Pension Fund.

FFOMS

Taxes for an employee are calculated according to regulatory documents. The contribution to the compulsory health insurance fund is 5.1% of salary. These funds are transferred to free medical care.

How is the size determined?

The amount of contributions depends on the category of taxpayer and the total amount accrued to the employee for the reporting period. As a percentage, the contribution amounts are as follows:

- Pension Fund - 22%. Additional fees may apply, depending on the danger. The organization must be notified of this.

- Social Insurance Fund - 2.9%. This fund receives funds for accidents that have occurred. The amount of contributions is withdrawn individually for each organization, determined by the type of activity. You can find out the amounts from the notice sent by the fund to the legal address of the company.

- FFOMS - 5.1%.

As a result, how much does the employer pay in taxes for the employee in 2017? The organization pays 4 payments for an employee.

Application of the simplified tax system

If an organization operates under a special tax regime (STS) and is considered “preferential” based on the type of work, then the amount of payments will be different. To use benefits, it is necessary to determine by codes whether the enterprise belongs to the types of activities specified in Federal Law No. 212.

For institutions and individual entrepreneurs making payments to citizens, payments are not made to the Social Insurance Fund and the Federal Compulsory Medical Insurance Fund. They need to pay contributions only to the Pension Fund at a low rate of 20%. An example of institutions that pay low fees to the Pension Fund and do not make payments to the Social Insurance Fund, Federal Compulsory Medical Insurance Fund:

- Education.

- Creation of sporting goods.

- Toy production.

- Construction.

Limit amounts

All employers need to keep records of paying taxes for employees. This is necessary not only for the correct calculation of amounts. The employee needs to know what amount of payments is allocated to him. The reason for this is that the indicated rates apply to specific limits of the salary transferred to the worker.

In 2018, the Pension Fund, if the organization does not have benefits, accrues 22%. This should be done until the entire income is no more than 796 thousand rubles. Then the tariff for these funds is reduced by 2 times and is equal to 10%.

A slightly different amount is determined for calculating contributions to the Social Insurance Fund. It amounts to 718 thousand rubles. After crossing this bar, no fees will be charged. In 2016, there were changes to contributions to the Federal Compulsory Medical Insurance Fund. Contributions are paid at 5.1%, no matter what the maximum amount is. The same situation applies to contributions to the Social Insurance Fund for injuries. For beneficiaries who use the simplified system, contributions to the Pension Fund at a reduced rate are not charged.

Taxes for individual entrepreneurs

Individual entrepreneur is a citizen who carries out business, but does not form a legal entity. For these citizens, contributions of specific amounts apply. Their size is determined by the level of the minimum wage of the Russian Federation. In 2016, this figure was 6,675 rubles. The rates were as follows: PFR - 26%, FFOMS - 5.1%.

There are no contributions to the Social Insurance Fund. If you calculate correctly, then for a year an entrepreneur pays 20,826 rubles to the Pension Fund for himself, and 4,085 to the Federal Compulsory Compulsory Medical Insurance Fund. For individual entrepreneurs, a maximum amount is established: when a profit reaches 300 thousand rubles and exceeds it, 1% is paid to the Pension Fund and the Federal Compulsory Compulsory Medical Insurance Fund.

What are the contributions used for?

Taxes paid for employees are spent on 3 main areas:

- For a pension paid for by the state.

- Free service in public medical institutions.

- Benefits for sick leave, maternity leave, and injuries.

Tax reduction

According to the Tax Code of the Russian Federation, groups of deductions are established that an employee has the right to use when establishing the amount of personal income tax:

- Standard. The amount and number of deductions is determined by the number of children and the benefits of the employee’s category.

- Social. Provides an opportunity to reduce the size of the base for treatment and education services.

- Property. It is provided with the purchase of property.

- Investment. Valid for transactions with securities.

You can apply for a tax deduction for children by providing a birth certificate. You still need to write an application. The following deductions are provided:

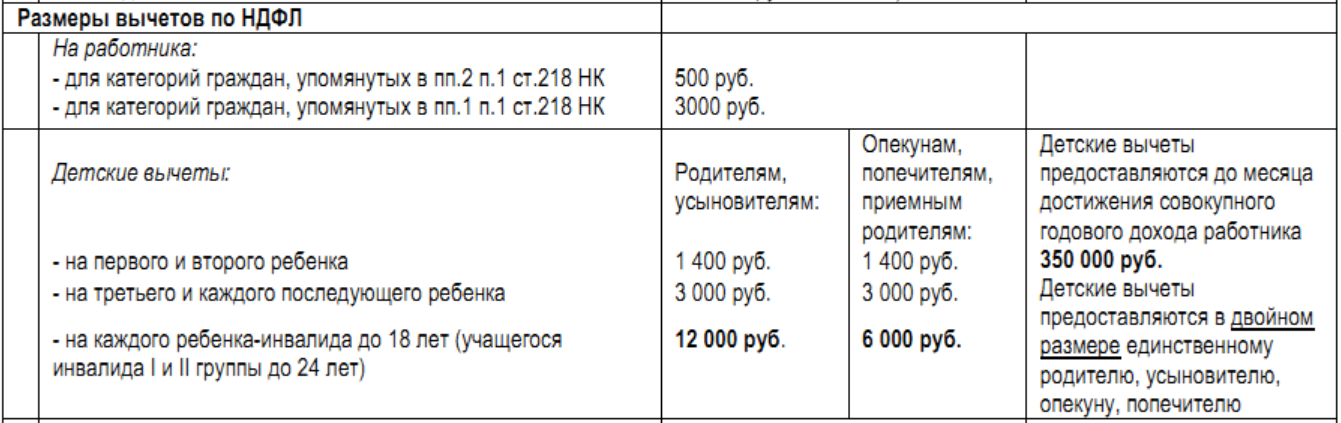

- 1400 rubles - for the first child.

- 1400 - on the 2nd.

- 3000 - on the 3rd and subsequent ones.

- 12,000 - for each disabled child under 18 years of age or for education up to 24 years of age.

If the employee is a single parent, the deduction amount is doubled. For registration, supporting documents are required. The deduction amount remains the same even if the children born grow up. For example, an employee has 3 children, but two are already 18 years old. But there is still a benefit in the amount of 3,000 rubles for 3 children until they reach adulthood. The standard deduction is provided until the amount of income for the year exceeds 350 thousand rubles.

Standard deductions per employee are:

- 500 rubles per month - Heroes of the USSR and Russia who participated in hostilities, war veterans, blockade survivors, disabled people (group 1, 2).

- 3000 rubles - for radiation sickness, disabled people of the Second World War.

Payment deadlines

Since 2016, there is 1 date when the employer needs to pay income tax on wages. It should be withheld from the employee’s salary when it is issued, and transferred the next day. It does not matter how the salary is paid - in cash or by card.

But there is an exception - tax on sick leave and vacation. It is paid at the end of the month in which they were completed. Amounts can be combined and sent as a single payment order. This helps to collect personal income tax on vacations and sick leave and send them in one order to the budget.

Contributions sent by the employer must be deposited by the 15th day of the month following the month in which the salary was sent. If this date falls on a weekend or holiday, the transfer is made on the next business day.

Reports

All employers are required to prepare reports, the information for which is salary amounts. For this there is:

- Help 2-NDFL. A document on the results of the year is drawn up for all employees. The certificate contains data on income, deductions, charges and tax deductions.

- Calculation of 6-NDFL. Provided quarterly to all company personnel. The document has 2 sections: the first includes data on income from the beginning of the year, and the second - for 3 months upon issue.

- Calculation of insurance premiums. This form is new, it was introduced in 2017. It acts to transfer management of contributions to the Federal Tax Service and cancel RSV-1. Provided to all employees at the end of the quarter.

- Report 4-FSS. It is handed over to social security. The document includes information on accruals and payment of contributions for injuries. Served at the end of the quarter.

- Report SZV-M. Provided to the Pension Fund of the Russian Federation monthly for employed persons. The document allows you to control who receives a pension but works.

- Report SZV-STAZH. The document is submitted to the Pension Fund every year. It was served for the first time only in 2018. The report contains information about employees, including those registered under GPC agreements, for the past year.

Thus, taxes for the employee must be paid by all employers. This is their responsibility. It is thanks to them that pensions are formed and people receive medical care. The state verifies this obligation through regulatory organizations.

Salaries are subject to taxes and insurance contributions to a number of extra-budgetary funds. The procedure for paying payroll taxes in 2017 is regulated by federal laws.

Payroll tax: features

Depending on the type of employment contract and the enterprise itself, there are various forms of remuneration. The labor legislation of the Russian Federation determines that an organization must pay wages to its employees twice a month: at the beginning and at the end, and contributions to extra-budgetary funds - once a month from the total amount of wages, taking into account all advances, vacation and sick leave payments.

The difference between the actual salary the employee receives and the accrued salary may also include other types of deductions. However, it must be taken into account that its size cannot exceed 20%.

Determining payroll tax and the amount of contributions to insurance and pension funds is a rather labor-intensive process that requires extensive knowledge of accounting and tax accounting. Errors may be considered an intentional violation and may be subject to penalties.

Payroll tax what percentage in 2017:

Calculation of taxes on wages under the main tax regime in 2017: instructions

Calculating payroll taxes is a serious and responsible process, errors in which can lead to serious consequences. In order to determine the correct size of this value, you must go through the following steps:

Get 267 video lessons on 1C for free:

- determine the amount at which the deduction will be determined;

- determine the tax rate that will be applied to the employee’s income;

- calculate personal income tax;

- subtract the required deductions from the amount received;

- determine the amount of insurance premiums, as well as the amount of contributions to extra-budgetary funds.

The most important tax that is calculated when determining the final salary is personal income tax, or personal income tax. In 2017 it is 13% of wages. Payroll tax table:

| Tax rate | Income | Procedure for calculating payroll tax | Governing Law |

| 13% | Salaries of Russian residents | Cumulative total with the use of deductions and subsequent offset of the paid personal income tax amount | Clause 1 of Article 224 of the Tax Code of the Russian Federation |

| 13% | Salaries of EAEU citizens and refugees | ||

| 30% | Salaries of non-residents of the Russian Federation | Separately for each type of income - without offsets or deductions | Clause 3 of Article 224 of the Tax Code of the Russian Federation |

You can determine the amount for which the deduction will be determined as follows:

- First of all, you need to decide on the initial parameters. Let's take the average person who works 5 days a week, which is approximately 21 days a month. Let's assume that out of these he went to work only 15 times. The employee’s salary is 20,000 rubles, which means that for the time worked the person received: 20,000 * (15/21) = 14,286 rubles.

- After this, you can start calculating the tax: 14,286*13%=1,857 rubles.

- Now we subtract the tax amount from the salary and get a net salary with taxes already paid in the amount of 12,429 rubles.

What does an employer face for failure to pay payroll taxes?

If the employer does not pay payroll tax, the organization will sooner or later face serious problems in the form of penalties imposed by the prosecutor's office, the state labor inspectorate or the tax office at the location of the organization. Typically, these bodies are approached by the employees themselves, who receive their salaries in envelopes. After receiving their applications, authorized organizations are required to conduct a thorough inspection, as well as decide on the initiation of administrative cases and imposition of penalties.

Also, authorized bodies are required to conduct regular scheduled inspections, which help to identify violations when calculating payroll taxes. In such cases, penalties are also provided.

Liability for violations in this area of taxation is regulated by Articles 122 and 123 of the Tax Code of the Russian Federation. Typically, the organization receives a bill in the amount of 20% of the amount of taxes not paid to the budget.

- Wages can be of two types: time-based and piece-rate. We calculate salaries based on the results of each month, using the following primary documents:

- ◊ report card;

- ◊ accounting records, work orders;

- ◊ orders on bonuses, work on weekends, etc. After calculating wages, you need to calculate how much is due for payment, that is, take into account all deductions and payments.

- Personal income tax of 13% is withheld from all income. The tax can be reduced depending on the number of children the employee has; this is the so-called child deduction:

◊ 1,400 rubles each for the first two children;

◊ 3000 rubles for the third and others.

¡ There are many features in providing this deduction; a professional accountant of the company will always understand them and take everything into account, because the size of the salary that the employee will receive depends on this.

Calculation of sick leave payments

Paying sick leave is one of the state social guarantees. It is issued in case of illness, care, as well as pregnancy and childbirth.

The basis of the calculation is the calculation of average earnings per day; for this purpose, the salary for the previous 2 years is summed up: for example, when calculating sick leave in 2016, the salary for 2014 and 2015 is taken, and the entire amount is divided into 730 calendar days. It is important to take into account all the charges that are taken into account and exclude those that are not included in it.

- The amount of the benefit depends on:

- – from the total work experience,

- – duration of work at the enterprise,

- – minimum wage values (from July 1, 2016 - 7500 rubles),

- – the size of the salary limit within which insurance premiums are calculated (624,000 rubles in 2014 and 670,000 rubles in 2015), depending on whether it is registered for oneself or for caring for a family member and on other factors.

Our accounting professionals will handle the correct calculation of benefits, the issuance of a certificate of incapacity for work, the creation of all accounting entries, and the calculation of social security contributions.

Calculation of vacation pay and compensation

Each employee is guaranteed 28 days of leave. How to calculate vacation pay?

Here, the average daily earnings are also determined, but the calculation algorithm is different: you need to know the salary for the entire 12 months before the vacation, including bonuses and additional payments, and excluding some periods.

The entire amount is divided into a certain number of days. For the calculation, not 365 or 366 is taken, but the calculated value, for example:

29.3 × 12 = 351.6 days, where

29.3 is the average number of calendar days, a constant value.

If there is a month in the vacation record in which the employee was on vacation, sick, or went on a business trip, we calculate the number of days in it as follows:

29.3 ÷ Number of days in a month × Number of days of work.

Compensation upon dismissal related to unused days of allotted vacation is calculated in a similar way. But there is a peculiarity: if the vacation period before dismissal consists of less than a full year, then the number of months for which compensation is due must be multiplied by 2.33 - this number shows how many days of vacation there are in each month (28 days ÷ 12 months). There are also a lot of nuances and difficult cases here, contact us - we will help!

Taxes from the payroll fund (payroll)

- After wages are calculated, payroll taxes are calculated, that is, insurance contributions to state extra-budgetary funds. Their size for the general taxation system is 30%, including:

- ◊ 22% — insurance contributions to the Pension Fund of Russia, the Pension Fund of Russia;

- ◊ 5.1% - insurance contributions to the Compulsory Medical Insurance Fund, the Compulsory Medical Insurance Fund;

- ◊ 2.9% - insurance contributions to the Social Insurance Fund, Social Insurance Fund.

Contributions to the Pension Fund of the Russian Federation are not calculated on the entire salary, but within a limit that changes every year; in 2016 it was equal to 796,000 rubles. per person per year. Over the limit, 10% of contributions are charged.

When calculating contributions to the Social Insurance Fund, the limit is also taken into account; it is 718,000 rubles. There are no over-limit accruals.

Entrepreneurs pay a fixed amount of contributions to the Pension Fund, which depends on the minimum wage: in 2016 it was 23,153.33 rubles. Plus they pay an additional 1% to the Pension Fund if they receive more income of 300,000 rubles.

The taxation system is a complex system of economic relations and obligations between a subject and an object. This is a set of taxes and fees established legally in a particular state.

In the Russian Federation, the concept of payroll is an abbreviation for the wage fund. Why are these taxes paid, and what is the current procedure for their registration? This question worries every taxpayer.

Responsibility for tax evasion in the Russian Federation

Evasion is now considered a serious offence. First of all, contributions to the Payroll Fund are made so that wages, bonuses and rewards are calculated. Taxes are paid to this fund by employees of all enterprises - both government agencies and private firms.

The structure and size of the wage fund is an individual indicator for each enterprise, since these parameters directly depend on the number of officially employed workers. The average salary of citizens is also taken into account.

Categories of the wage fund

The following types exist:

- Payment for time worked by the employee.

- Payments for unworked time due to employee sick leave or vacation.

- Incentive payments (most often this is a one-time payment).

- Regular payments, if work duties require the employee to use a regular car, or travel allowances.

The tax contribution directly depends on the official payroll amount. Using the accounting program "1C ZUP", the chief accountant of the enterprise calculates tax deductions to the following mandatory funds:

- to the Pension Insurance Fund;

- to the Social Insurance Fund;

- to the Health Insurance Fund.

In 2019, on the territory of the Russian Federation, the amount of contributions to the payroll remained unchanged - this is a 30% rate, it will be maintained until 2019 inclusive. The payment deadline depends on the type of activity. Currently, the contribution rates for different funds are as follows:

- contributions for the Pension Insurance Fund – 22%;

- for the Social Insurance Fund – 2.9%;

- for contributions to the Health Insurance Fund – 5.1%.

For a more detailed understanding of the deduction process, it is worth giving an example. The wage fund of JSC Galaktika amounted to 311 thousand rubles in October 2019. Salary costs will be:

- for pension insurance – 47,300 rubles;

- contributions to the Medical Insurance Fund - 10,965 rubles;

- contribution for the Social Insurance Fund – 6,235.

This rate may increase if the facility has an increased potential for injury. Calculation under the simplified tax system occurs according to the same algorithm.

Why is this tax needed?

Taxes to the Payroll Fund are an important component of decent earnings and material compensation for workers in a wide variety of enterprises and fields of activity. Any change in the amount of remuneration must be immediately reflected in the enterprise’s document flow and be justified. A deduction in the amount established by the state, when the fixed rate is 30%, allows you to insure the employee in the necessary funds. An ordinary employee of an enterprise does not personally calculate or prepare a tax contribution; in an enterprise this function is performed by the accounting department, dealing with all postings. Accountants monitor the accuracy and, most importantly, the timeliness of deductions.