How to generate an invoice in 1s. Accounting info

buh.ru/S.A. Kharitonov/September 2009

Changes to Chapter 21 “Value Added Tax” of the Tax Code of the Russian Federation came into force on January 1, 2009, but only at the end of May 2009, the Government of the Russian Federation, in accordance with the vested powers, made the necessary additions and changes to the Rules for maintaining logs of received and issued invoices - invoices, purchase books and sales books for VAT calculations. For a number of positions, the innovations turned out to be very significant, and necessitated the need to refine the standard configurations of 1C accounting programs to support them. Doctor of Economics, Professor of the Financial Academy under the Government of the Russian Federation S.A. talks about the most significant changes and their accounting (taking into account the explanations of the Ministry of Finance and the Federal Tax Service of Russia) in “1C: Accounting 8”. Kharitonov.

Procedure for issuing invoices

Federal Law No. 224-FZ dated November 26, 2008 introduced significant changes to Chapter 21 of the Tax Code of the Russian Federation “Value Added Tax”. In particular, organizations have the opportunity to deduct tax from the advance payment paid to the seller for the upcoming delivery of goods (performance of work, provision of services), transfer of property rights, the implementation of which is subject to VAT. To do this, a preliminary form of payment must be provided for by the terms of the agreement with the seller and an invoice of a “special” sample must be received from the seller, containing the indicators provided for in paragraph 5.1 of Article 169 of the Tax Code of the Russian Federation.

Since changes to Chapter 21 of the Tax Code of the Russian Federation came into force on January 1, 2009 (clause 1 of Article 9 of Federal Law No. 224-FZ of November 26, 2008), the new procedure applies to prepayment amounts starting from this date. However, the application of innovations in practice raised a number of questions, the answers to which were absent in the Tax Code of the Russian Federation and in the Rules in force at the time the innovations entered into force, approved by Decree of the Government of the Russian Federation of December 2, 2000 No. 914. In particular, one of the problems that some sellers have encountered in connection with the obligation to issue an invoice to the buyer for prepayment is related to the indication of the name of the goods. How to reflect the name if the contract contains a large list of goods supplied and it is impossible to determine for which goods the advance payment is received? Another problem was related to the timing of the advance invoice. Does it always need to be issued within five calendar days after receiving the advance payment? Is it required to be displayed if during this period (within five days) goods were shipped (transfer of work results, provision of services), or transfer of property rights?

During January-May 2009, the financial department issued explanatory letters on certain aspects of the practical application of innovations.

Name of goods in the invoice for advance payment

The innovations provide that upon receipt of advance payment (in whole or in part) for the upcoming supply of goods (performance of work, provision of services), transfer of property rights, the taxpayer is obliged to issue the buyer an invoice with indicators in accordance with paragraph 5.1 of Article 169 of the Tax Code of the Russian Federation. One of the indicators is the name of the goods supplied (description of work, services), transferred property rights. At the same time, Article 169 of the Tax Code of the Russian Federation does not indicate what should be indicated in this indicator if the contract contains a large list of goods supplied and it is impossible to determine for which goods the advance payment is received? The Ministry of Finance of Russia, in a letter dated 03/06/2009 No. 03-07-15/39, explained that if the contract gives a general name of the goods supplied and provides for their shipment according to the application (specification), then in invoices for advance payments the organization has the right to indicate also the general name goods or their groups (for example, petroleum products, confectionery, stationery, etc.). However, this is possible if the specification is issued after payment for the goods. In other cases, you should be guided by subparagraph 4 of paragraph 5.1 of Article 169 of the Tax Code of the Russian Federation, i.e. indicate in invoices for advance payments the name of goods (description of work, services), property rights in accordance with the agreement concluded between the seller and the buyer.

In "1C: Accounting 8" both options for displaying product names are supported. Let's consider how.

Option 1.

The contract provides for the determination of the specifications of goods after their advance payment. In the invoice for advance payment, it is enough to display the general name of the goods (group of goods).

In this case, the seller must fill in the details in the form of an agreement with the counterparty (see Fig. 1).

When receiving advance payment from the buyer, the seller should not fill out the details An invoice for payment the corresponding payment document (Fig. 2), even if such an account is available in the information database.

In this case, the default value of column 1 of the advance invoice will be the generalized name of the item from the agreement with the counterparty (Fig. 3).

Option 2.

The agreement provides for a one-time supply of goods. Advance payment is made in accordance with the approved specification. The name of all goods is displayed in the advance invoice.

In this case, the seller, using a document Invoice for payment to the buyer an invoice should be issued, the subject of which is the agreed specification.

Upon receipt of advance payment, the seller must provide details An invoice for payment corresponding payment document ( Incoming payment order(Fig. 4), Payment order for receipt of funds, Cash receipt order) provide a link to the document Invoice for payment to the buyer.

In this case, the default value of column 1 of the invoice for advance payment will be the item according to the invoice data for payment to the buyer.

If necessary, invoice details for payment can be specified manually directly in the processing form .

In practice, situations are possible when, for one reason or another, the specification of goods that must be indicated in the invoice for the advance payment does not coincide with what is indicated in the invoice for payment to the buyer. For such situations, a mode is provided for filling out the list (specifications) manually directly in the form of an invoice (for advance payment) created by processing Registration of invoices for advance payments(Fig. 5).

The letter of the Ministry of Finance of Russia dated March 6, 2009 No. 03-07-15/39 also provides clarification on the issue of correctly filling out prepayment invoices if the supplied goods are taxed at different rates (10 and 18 percent). Two options are offered:

- allocate products with different rates into separate positions;

- indicate the general name of the goods, but apply the tax rate of 18/118.

In "1C: Accounting 8" the first option is implemented by indicating the tax rate for each item of the invoice for payment and deciphering the received payment in the form of a list (Fig. 6).

If goods taxed at different rates are paid for in advance and their specifications are not known in advance, when filling out the field Generalized name of goods for an advance invoice forms of an agreement with a counterparty, it is necessary to indicate a link to a directory element Nomenclature with a tax rate of 18%.

Deadline for issuing invoices for prepayment

According to the general rule, enshrined in paragraph 3 of Article 168 of the Tax Code of the Russian Federation, the seller must issue an invoice to the buyer for the amount of the prepayment (full or partial) within five calendar days after receiving it.

At the same time, according to the clarifications of the Ministry of Finance of Russia, given in letter No. 03-07-15/39 dated 03/06/2009, this can not be done if the shipment of goods (performance of work, provision of services, transfer of property rights) is also made against the received advance payment within the specified five days.

For continuous long-term supplies of goods (provision of services) to the same buyer (supply of electricity, oil, gas, provision of communication services, etc.) an exception is also provided from the general rule: invoices for partial payment on account of such supplies are issued to customers at least once a month, no later than the 5th day of the month following the previous month.

In this case, the amount of the prepayment is determined as the difference between the payment received in the corresponding month and the cost of goods (services provided) shipped during this month.

According to a number of experts, the position of the Russian Ministry of Finance on the timing of issuing invoices for advance payments is controversial. Existing judicial practice proceeds from the fact that payments cannot be recognized as advance payments if payment and shipment of goods occurred in the same tax period. Since the tax period for VAT is considered a quarter (Article 163 of the Tax Code of the Russian Federation), the seller should not issue invoices for advances received in the quarter in which the goods were shipped (work performed, services provided).

"1C: Accounting 8" supports the variability of issuing invoices for advance payments. The procedure for extracting can be established both for the organization as a whole and for a specific agreement with a counterparty.

For the organization as a whole, the procedure for registering invoices for advance payments is established in the details of the same name on the VAT tab of the information register entry form Accounting policies of organizations.

You can set one of the following options:

- Always register invoices for advances upon receipt of an advance.

- Do not register invoices for advances cleared within five calendar days.

- Do not register invoices for advances credited before the end of the month.

- Do not register invoices for advances credited until the end of the tax period (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 10, 2009 No. 10022/08).

- Do not register invoices for advances (Clause 13, Article 167 of the Tax Code of the Russian Federation).

Unless otherwise specified in the properties of the contract with the counterparty, when selecting the option Always register invoices for advances upon receipt of an advanceRegistration of invoices for advance payment invoices will be created for each amount received. The exception is prepayment amounts that are credited on the day they are received. For such received amounts, advance invoices are not created by processing.

when using processing

If an organization wants to follow the clarifications of the Russian Ministry of Finance, then in the accounting policy parameters it is necessary to indicate the option Do not register invoices for advances offset within five calendar days.

The third option also corresponds to the explanations of the Russian Ministry of Finance, but is aimed at organizations that carry out continuous long-term supplies of goods (provision of services) to the same buyer.

The fourth option is intended for organizations that are ready to resist possible claims from tax authorities regarding the timing of issuing invoices for advance payments.

The last option is intended for organizations whose activities fall under paragraph 13 of Article 167 of the Tax Code of the Russian Federation, i.e. those that are engaged in the production of goods (work, services) (according to the list determined by the Government of the Russian Federation) with a production cycle duration of more than six months (list approved by Decree of the Government of the Russian Federation dated July 28, 2006 No. 468).

In the case of receiving an advance payment for the specified goods (work, services), these organizations have the right to determine the moment the tax base arises as the day of shipment (transfer) of these goods (performance of work, provision of services).

In this case, the encumbrance is the presence of separate accounting of transactions and tax amounts for purchased goods (work, services), including fixed assets and intangible assets, property rights that are used to carry out operations for the production of goods (work, services) of a long production cycle, from other operations.

By default, the procedure established in the accounting policy parameters is applied to all advance payments received from customers.

If an agreement with a specific buyer has features related to the nature of the activity that affect the procedure for issuing invoices for advances, then for this agreement you can establish an individual procedure for generating invoices for advances.

To do this, you need to uncheck the box in the contract form with the counterparty Register invoices in a manner consistent with accounting policies and choose the procedure for registering invoices for advances under the contract (Fig. 7).

Organization name on the invoice

Decree of the Government of the Russian Federation dated May 26, 2009 No. 451 approved changes to the Rules for maintaining journals of received and issued invoices, purchase books and sales books when calculating value added tax. Most of the changes made by the time the “new” rules came into force (June 9, 2009) were already supported in the 1C:Enterprise program system, but one innovation turned out to be unexpected. It concerns the procedure for filling out line 2 of the invoice. In accordance with the updated rules, line 2 must indicate "...the full and abbreviated name of the seller in accordance with the constituent documents. When drawing up an invoice by tax agents specified in paragraphs 2 and 3 of Article 161 of the Tax Code of the Russian Federation, this line indicates the full or abbreviated name of the seller (specified in the agreement with tax agent), for whom the tax agent fulfills the obligation to pay tax". History is silent, consciously or not, in the first sentence the conjunction “and” is indicated, and in the second – the conjunction “or”, but the following conclusion follows from a literal reading. If an organization draws up an invoice as a taxpayer, then in column 2 it is necessary to indicate two names: full and abbreviated, and if as a tax agent, then one of your choice is sufficient: full or abbreviated. Taking into account that tax authorities cling to any opportunity not to deduct tax if the invoice is not drawn up according to the “rules”, specialists from 1C quickly implemented support for the new requirement to fill out column 2. For this purpose, the reference book was modified Organizations, in which separate fields for the abbreviated and full names are now highlighted, and named accordingly Abbreviated name (according to constituent documents) And Full name (according to constituent documents).

In invoices issued before June 9, 2009, the name is displayed in accordance with the settings for printed forms of the Organization's directory, and those issued starting from June 9, 2009 - the full and abbreviated name in the format <Полное наименование (Сокращенное наименование)>

.

In this case, to print regulated reports, the full name is used, and to display printed forms of primary documents and reports, you can select an abbreviated or full name (Fig. 8).

It should be noted that the story with the conjunctions “and” and “or” was continued. Almost from the moment the updated rules came into force, the Russian Ministry of Finance “realized” that there was a “typo” in the text, but instructed the Federal Tax Service of Russia to “explain” this to taxpayers. For more than a month, both departments agreed on the text, and finally, on July 14, 2009, the Federal Tax Service of Russia issued letter No. ШС-22-3/564@, which it called “On the procedure for filling out line 2 of the invoice.” Most of the writing is "lyrics". The reason for which the letter was issued is contained in the penultimate paragraph. It says that "... if, when filling out line 2 of the invoice, the VAT payer - the seller, indicates only the full or only the abbreviated name corresponding to the constituent documents, then this invoice cannot be the basis for refusing to accept for deduction the amount of tax presented by the seller". 1C specialists have decided not to respond to these clarifications until changes are made directly to the text of the Rules, since the letter is not a normative document. Thus, the type of organization name specified in the details For printed forms ( abbreviated name or Full name) is used to print all forms of primary documents with the exception of invoices.

Preparation of invoices for advance payments

Invoices for advance payments are issued using the document Invoice issued It can be created manually on the basis of a payment document with which the advance payment received from the buyer is registered in the information database, but this method should be used only in exceptional cases. The program developers recommend using processing for this Registration of invoices for advance payments.

Data processing can be carried out either per day or over a period, depending on the period within which the invoice must be issued to the buyer. Treatment Registration of invoices for advance payments allows you to create documents Invoice issued for an advance automatically, taking into account the registration procedure established in the accounting policy parameters and in the agreement with the counterparty. For example, if the accounting policy or agreement stipulates that invoices are not generated if the advance payment is credited for some time, then when processing documents Invoice issued are created only for those advances for which there was no offset and the established period has passed since the date of receipt of the advance (Fig. 9).

If the date of issue of the invoice for the advance payment exceeds the date when the invoice should be issued, then the line with data for this advance payment is highlighted in red. To eliminate the violation, you must manually change the date of issue (registration) of the invoice.

Payment and fulfillment of obligations under the contract can occur within one day. In this case, processing does not create an advance invoice, regardless of the established procedure for registering advance invoices.

When posting a document for the tax amount, an accounting entry is generated as the debit of the account 76.AV VAT on advances and prepayments and account credit 68.02 Value added tax. In this case, the posting date corresponds to the document date. In this regard, we draw attention to the specifics of applying the “5 calendar days” rule. We remind you that it applies only to the period for issuing (transferring) the invoice to the buyer (not to be confused with the date of preparation (extract) of the invoice, which is indicated in column 1). In "1C: Accounting 8" when registering invoices for advance payments received during the tax period, the date of the invoice (the date of the document Invoice issued) by default, in accordance with the recommendations of the Russian Ministry of Finance, it is considered to fall on the last day of the period during which the invoice must be issued to the buyer.

At the same time, if the advance payment was received on the last days of the tax period, then the “5 calendar days” rule is ignored, and invoices are automatically issued for the received advance payments with a date falling on the last day of the period.

This is due to the fact that the amount of advance VAT must be taken into account when calculating tax in the period of its receipt.

In conclusion, we note that in order to maintain invoices in accordance with the new Rules, clarifications of the Ministry of Finance of Russia and the Federal Tax Service of Russia, users of "1C: Accounting 8" need to update the standard configuration "Enterprise Accounting" to release 1.6.16.

Every accountant sooner or later encounters advance payments (whether to their suppliers or advances from buyers) and in theory knows that according to the requirements of the Tax Code of the Russian Federation (Article 154, paragraph 1; Article 167, paragraph 1, paragraph 2 ) VAT must be calculated on the advance payment on the date of its receipt. Our article today is about how to do this in practice with advance invoices in the 1C 8.3 program.

Making the initial settings

Let's take a look at the company's accounting policy and check whether the tax regime we have indicated is correct: OSNO. In the “Taxes and Reports” section in the “VAT” tab, the program gives us a choice of several options for registering advance invoices (Fig. 1) (we need this setting when we act as a seller).

We may not register advance invoices in 1C if:

- the advance was credited within five days;

- the advance was credited until the end of the month;

- the advance was credited until the end of the tax period.

It is our right to choose any of them.

Let's analyze the offset of advances issued and advances from the buyer.

Accounting in 1C for advances issued.

For example, let’s take the trading organization Buttercup LLC (we), which entered into an agreement with the wholesale company OPT LLC for the supply of goods. According to the terms of the contract, we pay the supplier an advance of 70%. After which we receive the goods and pay for them completely.

In BP 3.0 we draw up a bank statement “Debit from current account” (Fig. 2).

Please pay attention to important details:

- type of transaction “Payment to supplier”;

- contract (when posting goods, the contract must be identical to the bank statement);

- VAT interest rate;

- offset of the advance payment with VAT automatically (we indicate a different indicator in exceptional cases);

- When posting a document, we must receive correspondence of 51 invoices with the supplier's advance invoice, in our example it is 62.02. Otherwise, an invoice for the advance payment in 1C will not be issued.

Having received payment, OPT LLC issues us an advance invoice, which we must also post in our 1C program (Fig. 3).

On its basis, we have the right to accept the amount of VAT on the advance as a deduction.

Thanks to the “Reflect VAT deduction in the purchase book” checkbox, the invoice automatically goes into the purchase book, and when posting the document, we receive an accounting entry with the formation of invoice 76.VA. Please note that the transaction type code 02 is assigned by the program independently.

Next month OPT LLC ships the goods to us, we receive them in the program using the document “Receipt of Goods”, and register an invoice. We do not correct accounts for settlements with the counterparty; we select “Automatic” for debt repayment. When posting the “Goods Receipt” document, we must receive a posting for the advance payment offset (Fig. 4).

When filling out the document “Creating sales book entries” for February, we receive automatic completion of the “VAT Restoration” tab (Fig. 5), and this amount of restored VAT ends up in the sales book for the reporting period with transaction code 22.

To reflect the final payment to the supplier, we can copy and post an existing document “Write-off from the current account”, indicating the required amount.

We create a purchase book, which reflects the amount of our VAT deduction on prepayment with code 02, and a sales book, where we see the amount of restored VAT after receiving the goods with transaction type code 21.

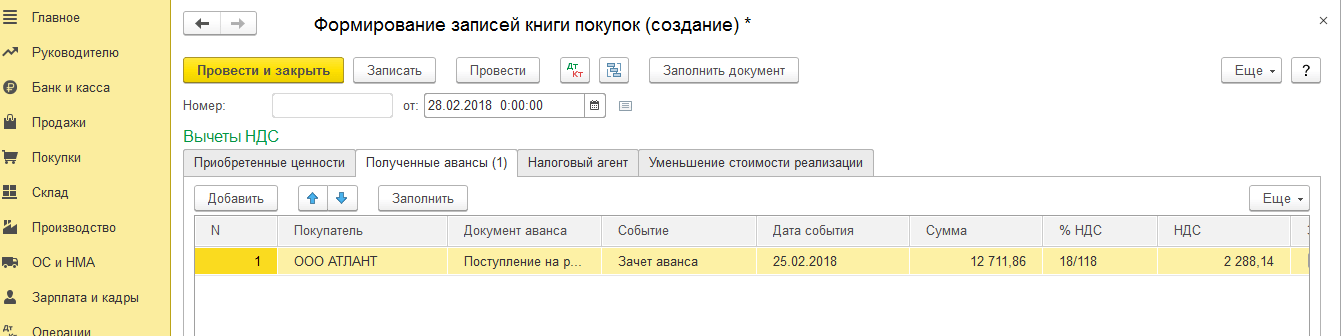

Accounting in 1C for advances received

For example, let’s take an organization familiar to us, LLC “Lutik” (we), which entered into an agreement with the company LLC “Atlant” for the provision of goods delivery services. According to the terms of the agreement, the buyer of Atlant LLC pays us an advance of 30%. After which we provide him with the necessary service.

The method of working in the program is the same as in the previous version.

We formalize the receipt of an advance in 1C from the buyer with the document “Receipt to the current account” (Fig. 6), followed by registration of an advance invoice, which gives us accounting entries for calculating VAT on the advance (Fig. 7).

You can register an invoice for an advance payment in 1C directly from the document “Receipt to the current account”, or you can use the processing “Registration of invoices for an advance payment”, which is located in the “Bank and cash desk” section. In any case, it immediately goes into the sales book.

At the time of the document “Sales of services”, the buyer’s advance will be credited (Fig. 8), and when the document “Creating purchase book entries” is executed (Fig. 9), the amount of VAT on the advance received will be deducted, account 76.AB is closed (Fig. . 10).

To check the fruits of his work, an accountant usually only needs to create books of purchases and sales, as well as analyze the “VAT Accounting Analysis” report.

Work in 1C with pleasure!

If you still have questions about advance invoices in 1C 8.3, feel free to ask us on the dedicated line. They work 7 days a week and will help in the most difficult situations in tax and accounting.

An invoice is the main document on which VAT is claimed for deduction. In order for this to be possible, certain conditions exist:

Goods and/or services must be purchased for further resale or production work.

Each received product must be accepted for accounting and listed on the balance sheet.

The presence of the “Invoice” document itself, which must be correctly drawn up and registered in the program.

In the 1C program, incoming VAT is accounted for according to receipt documents and according to created entries in the purchase book. Sometimes situations arise that a registered invoice is not reflected in the purchase ledger. To correctly account for VAT in the purchase book, it is necessary to follow the sequence of execution of all receipt documents. Let's look at the example of registering an invoice from a supplier with the provided invoice:

In this case, the invoice is generated automatically directly from the document “Receipt of goods, services”:

Pay attention to the checkbox next to the item “Reflect the VAT deduction in the purchase book by the date of receipt.” Based on this, an entry in the purchase book will appear exactly in the period in which the invoice is registered.

But sometimes it happens that documents are transferred or processed retroactively. As a result, there is a discrepancy between the actual date of receipt of the invoice. In this case, the creation of the “Invoice” document may not be reflected in the purchase book. In rare cases, there may be a discrepancy between the dates of receipt of goods and documents. For example, when a production enterprise receives fixed assets or equipment that can be taken into account in another reporting period:

The movement of the document will reflect the time difference:

When registering the receipt of OS (or equipment), the checkbox “Reflect VAT deduction in the purchase book by the date of receipt” must be unchecked:

VAT will be deducted after the equipment is accepted for accounting:

The invoice will be reflected in the purchase book if there is a posting Debit 01 – Credit 08:

In this case, you need to fill out the document “Creating purchase ledger entries”:

Other errors may be caused by checking the box “VAT included in price”:

This item is noted only when separately accounting for VAT when using materials for the production of products without VAT.

In order for VAT to be deducted, you need to check the box.

Also, errors can occur due to duplicate invoices when accounts 60.02 and 76.VA are not reconciled. This can happen if the document of payment and receipt of goods is not promptly entered. In a situation where first only bank and cash documents are entered, and later an advance invoice is entered based on them. If receipt documents are then displayed as a general list, then previously entered invoices may be duplicated. In this case, both documents end up in the sales book. To avoid this, it is necessary to restore the sequence by re-posting payment and receipt documents. It is mandatory to check the correctness of the postings.

Learning to do batch issuance of acts and invoices (1C: Accounting 8.3, edition 3.0)

2016-12-08T12:54:00+00:00Troika (1C: Accounting 8.3, edition 3.0) has an absolutely wonderful opportunity for batch posting of documents.

This opportunity is suitable for those companies that provide the same services (or groups of services) to the same contractors month after month.

Well, for example, let’s imagine that we are an Internet provider.

We have 200 clients:

- 150 of whom pay 1000 rubles every month at the Economy tariff

- 50 pay 3,500 rubles at the Business tariff.

At the end of every month we generate 200 sets of documents(act of provision of services for communication and invoice).

In this lesson I will tell you how to simplify this process to the point of impossibility in 1C.

Let me remind you that this is a lesson and you can safely repeat my steps in your database (preferably a copy or a training one), the main thing is that the version of the database is 1C: Accounting 8.3, edition 3.0.

So, let's begin

Go to the "Main" section, "Functionality" item:

Go to the "Trade" tab and check (if it is not already there) the "Batch issuance of acts and invoices" checkbox:

Entering clients into the directory

Go to the "Directories" section, "Counterparties" item:

We create two subgroups in the “Buyers” group: “Business” Tariff and “Economy” Tariff:

We have 50 customers on the “Business” tariff; for educational purposes we will include the first two.

We add the first counterparty to the "Business" tariff, here is his card:

We go to the client agreements and create a new agreement there:

Fill in the contract price type"Wholesale", validity until the end of the year and type of payment.

You need to create the calculation type yourself and name it, for example, Communication “Business”. This type does not affect anything, but simply helps us separate clients on the business tariff from clients on the economy tariff.

In the same way, create a second client in the “Business” Tariff group:

Be sure to indicate in his contract the same type of prices and the same type of calculations.

It turns out that all counterparties of the “Business” Tariff group will have an agreement with the same type of prices and the same type of payment. Why this is needed - you will find out below.

And so we fill as many customers on the business tariff as we need...

Let's move on to the "Economy" Tariff group.

We create the first client and his contract:

Here is the contract card:

Please note that the type of settlements for this group of counterparties will be different (but the same for all of them), for example, let’s call it Communication “Economy”.

In the same way, we will create a second buyer on the economy tariff:

And in the same way we will fill as many buyers as we need...

We add services to the directory

Go to the "Directories" section, "Nomenclature" item:

In the "Services" group we create two services, Internet Business and Internet Economy:

We set prices for services

Go to the "Warehouse" section, "Setting item prices":

We create a new document “Setting item prices” from the beginning of the year. Price type "Wholesale", in the table section we add our services and prices:

We carry out the document.

We issue acts and invoices

The preparatory part is finished. Now we can issue acts and invoices to all our customers in batch (group) mode every month (or more often).

It's very easy to do.

Go to the “Sales” section, “Services” item:

If you do not have this item, then you did not enable the “Batch issuance of acts and invoices” checkbox in the functionality (we did this in the very first step of this lesson).

First, we will submit the entire package of documents for all counterparties of the Economy tariff.

To do this, indicate the type of calculation Communication "Economy", the product (service) Internet Economy, and then in the tabular section click the button "Fill in" -> "By type of payment":

1C in this case will analyze the agreements of all counterparties in which the specified type of settlement is filled in and insert these counterparties along with these agreements into the tabular section:

The price in the tabular part was substituted due to the fact that we indicated it in the document “Setting item prices” for the “Internet Economy” service.

If you also need to issue invoices, go to the “Invoices” tab and click the “Mark all” button:

We post the document and see that all the transactions that are usually generated by a deed and an invoice have been generated, only for all counterparties at once:

From the same document we can print acts, invoices or documents for all counterparties at once.

Issuing invoices using the 1C 8.3 Accounting database

In 1C 8.3 programs there are only two types of invoices:

- Invoice issued

- Invoice received

However, each has several options.

The main options for an issued invoice:

- For implementation

- For advance

- For the principal's advance

- Corrective

- Tax agent

The main options for the invoice received:

- For admission

- For advance

- For the principal's advance

- Corrective

All invoices in 1C can be generated on the basis of primary documents - invoices and invoices.

Issuing an invoice for sales (issued)

Figure 1 shows the implementation document. To write and post an invoice in 1C, you need to click the button at the bottom left.

In Fig. 2 we see the invoice itself, generated according to the data of the implementation document. The number, date, as well as all other details are filled in automatically. The user only needs to specify the storage method (it is automatically set to “hard copy”). You can print the document in 1C by clicking the “Print” button and give it to the counterparty.

Invoices issued for advance payment

Advance invoices are registered by special processing, which is called that. They are usually issued once at the end of the reporting period.

Before moving on to the processing itself, let’s set up the accounting policy in the “VAT” section (Fig. 3).

To reduce the number of invoices issued, you can select the registration order, highlighted with a red outline (Fig. 3). In this case, invoices will be issued only for advances for which goods have not been shipped at the end of the quarter.

Processing is called from the “VAT Accounting Assistant” section (Fig. 4).

There is also a point for registering tax agent invoices. Let us remind you that in order to conduct transactions as a tax agent, you must set the appropriate attribute in the agreement.

Invoices received

The fundamental difference between invoices received is the need to correctly indicate the incoming document number and date (generated by the supplier).

Registration in 1C of incoming invoices for advance payment

Advances to suppliers are issued on the basis of documents debiting cash or non-cash funds (Fig. 6).

Posting adjustment invoices

To generate adjustment invoices, special documents have been developed:

- Implementation adjustments

- Adjustment of receipts

Let's look at an example of adjusting a receipt invoice (Fig. 7). The document can be created either on the basis of receipt or on the basis of the primary invoice.

Let's assume that the parties have agreed to change the purchase price. The old and new prices are indicated in two adjacent lines of the tabular part of the adjustment document. Everything else is calculated automatically. This includes automatically registering a correction invoice; you will only have to manually enter the number of the correction or adjustment.

Adjustments for sales are made in the same way.

Invoices “For advance payment by the principal” are issued only for contracts with the type “With the principal (principal)…”

Checking received and issued invoices in 1C

In conclusion, a few words about checking issued and received invoices. In the latest versions of 1C programs, a wonderful report has appeared - “Express check of accounting” (Fig. 8).

This report displays source documents for which invoices are not registered (or not issued), and also provides recommendations for correcting detected errors.

Based on materials from: programmist1s.ru