Terms and features of payment of vacation benefits in accordance with the Labor Code of the Russian Federation. Why you can’t issue vacation pay three days before the vacation Our opinion: rely on the month the income occurred

In field 107 of the payment order you must indicate the tax period for which the tax or contribution is paid. From the contents of field 107 it should be clear for what period the tax is paid. Also, a specific date can be indicated in field 107. Recently, the Federal Tax Service issued a letter dated July 12, 2016 No. ZN-4-1/12498, in which it stated that tax agents should fill out several payment slips to pay personal income tax. According to the new rules for filling out payment slips, should field 107 be indicated now? Is it possible to continue making one payment? Let's figure it out.

Introductory information

Field 107 must be filled in to indicate the frequency of payment of the tax payment or the specific date for payment of the tax payment, if such a date is established by the Tax Code of the Russian Federation (clause 8 of the Rules, approved by order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n).

In field 107 the 10-digit tax period code is entered. The first two characters are the tax payment period. For example, for quarterly - CV, monthly - MS, annual - GD.

The fourth and fifth digits are the tax period number. For example, if the tax is paid for August, “08” is indicated.

The seventh to tenth signs indicate the year. Dots are always placed in the third and sixth characters. For example – KV.03.2016.

New clarification from the Federal Tax Service on field 107

The letter of the Federal Tax Service dated July 12, 2016 No. ZN-4-1/12498 states that the tax agent should prepare several payment orders if personal income tax is transferred with different payment terms.

Thus, the Federal Tax Service, in fact, recommends new rules for filling out payment orders starting in July 2016. After all, there were no such demands from tax authorities before. However, after these recommendations appeared, accountants had questions about what exactly to enter in field 107.

What exactly should I indicate in field 107 now?

When paying personal income tax, tax legislation establishes several payment deadlines and for each of these deadlines there is a specific payment date (See “”).

Here are some examples.

Personal income tax from salary

Personal income tax on wages, bonuses and material benefits must be transferred to the budget no later than the day following the day of payment of income (paragraph 1, clause 6, article 226 of the Tax Code of the Russian Federation).

Example.

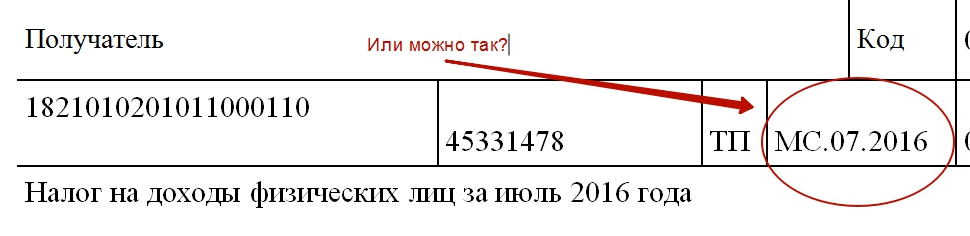

The employer paid wages for July to employees on August 4, 2016. In this case, the date of receipt of income will be July 31, the date of tax withholding will be August 4. And the last date when personal income tax should be transferred to the budget is August 5, 2016. Does this mean that you need to put 08/05/2016 on your payment slip?

Or can you indicate “MS.07.2016” in field 107 of the payment order to make it clear that this is a tax for July?

Personal income tax on sick leave and vacation pay

Personal income tax withheld from temporary disability benefits, benefits for caring for a sick child, as well as from vacation pay must be transferred no later than the last day of the month in which the income was paid (paragraph 2, clause 6, article 226 of the Tax Code of the Russian Federation).

Example.

The employee goes on vacation from August 25 to September 15, 2016. His vacation pay was paid on August 15. In this case, the date of receipt of income and the date of withholding personal income tax is August 15, and the last date when the tax must be transferred to the budget is August 31, 2016. Would it be correct to mark 08/31/2016 in field 107 of the personal income tax payment slip? Or should I indicate “MS.08.2016”?

The rules for filling out payment orders do not have a clear answer to these questions. Therefore, we will express our opinion on how to implement the new recommendations given in the letter of the Federal Tax Service dated July 12, 2016 No. ZN-4-1/12498.

Our opinion: rely on the month of income occurrence

We believe that there is no need to indicate a specific date in payment orders. After all, most likely, the main thing for tax inspectors is not to collect a lot of information about different dates, but to understand for what period the personal income tax was paid and compare it with the 6-personal income tax calculation. And if so, then accountants, in our opinion, need to rely specifically on the month in which the employees had taxable income.

To determine which month personal income tax applies to, refer to the date of recognition of income under Article 223 of the Tax Code of the Russian Federation. For example, for salaries, this is the last day of the month for which money is issued. For vacation and sick leave - the day of payment (Article 223 of the Tax Code of the Russian Federation). Let us explain with examples and samples of payment slips.

Wage

It follows from paragraph 2 of Article 223 of the Tax Code of the Russian Federation that wages become income on the last day of the month for which it is accrued (clause 2 of Article 223 of the Tax Code of the Russian Federation). Therefore, enter in field 107 the number of the month for which the salary was accrued. Let's assume that an accountant prepares a personal income tax payment from wages for August. Then in field 107 he will indicate “MS.08.2016”. Even though the payment is drawn up in September. And this, in our opinion, will be correct.

Vacation pay

Vacation pay becomes income on the last day of the month in which they were paid (clause 6 of Article 223 of the Tax Code of the Russian Federation). For example, if you pay vacation pay to an employee in September, then in field 107 of the income tax payment slip, indicate “MS.09.2016”. Even if the vacation “shifts” to October.

Sick leave

Vacation pay becomes income on the last day of the month in which they are paid (clause 6 of Article 223 of the Tax Code of the Russian Federation). For example, if you pay vacation pay to an employee in October 2016, then in field 107 of the payment slip you need to fill in “MS.10.2016”. And thereby show that vacation pay was paid in the tenth month of 2016.

Material benefit

Sometimes employees receive income in the form of material benefits, for example, from a loan received. To transfer income tax from him in field 107 of the payment order, fill in the month on the last day of which the person gained material benefit. For example, if the material benefit from using the loan arose in November 2016, then fill out field 107 as follows:

Paying off debts: field 107

Tax agents are also required to fill out field 107 in situations where personal income tax debts are being repaid. If the organization repays the debt on its own initiative (voluntarily), then in field 107 indicate the month for which the debt is repaid. And in field 106 put the PO code. This code will mean that this is not a current payment, but a debt repayment. Let’s say, if you are paying off your personal income tax debt for April 2016, then make up your payment order like this:

How to fill out field 107 in ambiguous situations

Now let's look at several common situations for filling out field 107 when transferring personal income tax.

Situation 1. Salary and vacation pay at the same time

In August, the organization simultaneously issued salaries for July and vacation pay on the same day.

Solution. In relation to wages, the income date is the last day of the month for which it is accrued. For vacation pay, this is the day the money is issued. Therefore, you need to make two payments. In field 107 for salary tax, enter “MS.07.2016”, and in field 107 for vacation pay tax - “MS.08.2016”. This will make it clear which month you are transferring tax for. And this approach will meet the new recommendations of tax authorities.

Situation 2. Salary and sick leave at the same time

In September, the organization simultaneously issued salaries for August and vacation pay on the same day.

Solution. In relation to wages, the income date is the last day of the month for which it is accrued. For vacation pay, this is the day the money is paid. Therefore, you need to make two payments. In field 107 for salary tax, enter “MS.08.2016”, and in field 107 for vacation pay tax - “MS.09.2016”.

Situation 3. Vacation pay was issued in another month

Solution. In relation to vacation pay, the date of income is the day the money is issued. It doesn’t matter what month the employee takes a vacation. Therefore, in field 107 of the payment slip for the transfer of personal income tax from vacation pay, indicate “MS.08.2016”. That is, show that you issued the vacation pay in August 2016.

Situation 4. Salary and bonus at the same time

Situation 5: payments to contractors

The contractor was paid in September for services rendered in August.

Solution. The date of receipt of income under a civil contract is the day the money is issued. This day fell in September. Therefore, in the payment slip for personal income tax, in field 107, enter “MS.09.2016”.

Situation 6: daily allowance

In August, the employee received excess daily allowance related to his business trip. Personal income tax must be withheld from them. The advance report on the results of the business trip was approved in September 2016. The tax was withheld from the salary for September.

Solution. The date of receipt of income for excess daily allowance is the last day of the month in which the advance report for the business trip was approved (clause 6, clause 1, article 223 of the Tax Code of the Russian Federation). For wages, the date of income is the last day of the month for which the money was paid (clause 2 of Article 223 of the Tax Code of the Russian Federation). That is, in both cases - the last day of the month. Therefore, in our opinion, you can make one payment and in field 107 mark “MS. 09.2016". After all, the tax authorities in their explanations did not say that the tax should be divided into different payments and with the same payment deadlines.

conclusions

There is also an opinion among accountants that after the appearance of the Federal Tax Service letter dated July 12, 2016 No. ZN-4-1/12498, payment slips should indicate specific dates no later than which the organization or individual entrepreneur must pay personal income tax. For example, personal income tax on vacation pay issued in September must be transferred by the end of the month. Therefore, in field 107 when paying personal income tax on vacation pay, you need to put “09/30/2016”. Personal income tax must be transferred from the paid salary the next day. This means that if the salary was issued, say, on September 5, then in field 107 you need to indicate the next day, that is, “09/06/2016”. This option also has a right to exist. Moreover, we do not rule out that it is correct and will not cause claims from the Federal Tax Service. But, unfortunately, there are no official explanations on this matter yet.

In our opinion, before making a final decision about what exactly to write in field 107, it still makes sense to ask for clarification from your Federal Tax Service. But in any case, keep in mind: inspectors do not have the right to fine the tax agent or charge penalties if the tax is paid on time and the payment falls into the budget.

Moreover, if a tax agent, for example, paid wages and vacation pay on the same day and filled out only one payment order, then this cannot be considered a violation or error if the payment goes to the budget at the correct KBK. Cm. " ". At the same time, we repeat that tax authorities most likely plan to correlate the data from field 107 with 6-NDFL calculations. And if the tax program cannot match the accrued and transferred tax, then the inspectorate may request clarification, ask to clarify the calculation or payment details.

When preparing Form 6-NDFL, accountants are faced with difficulties in how to reflect certain amounts of personal income tax calculated and withheld by the tax agent. In this article we will look at how to correctly reflect vacation payments in four different situations.

Based on the professional standard, each specialist can outline specific ones for himself. To do this, it is enough to undergo training at the Accounting School. All our courses are developed taking into account the professional standard “Accountant”.

The procedure for filling out the calculation in form 6-NDFL was approved by Order of the Federal Tax Service of the Russian Federation dated October 14, 2015 No. ММВ-7-11/450@.

In the 6-NDFL calculation, vacation pay is reflected in the period in which it was actually paid.

Example (vacation pay accrued and paid in one quarter)

Vacation pay paid:

- January 20, 2017 - 25,000 rubles, personal income tax - 3,250 rubles transferred on the day of payment of vacation pay

- March 20, 2017 - 30,000 rubles, personal income tax - 3,900 rubles transferred on the day of payment of vacation pay

- line 020 - 55,000 (25,000 + 30,000)

- line 040 - 7 150 (3 250 + 3 900)

- line 070 - 7 150

- line 100 - 01/20/2017

- line 110 - 01/20/2017

- line 120 - 01/31/2017

- line 130 - 25,000

- line 140 - 3 250

- line 100 - 03/20/2017

- line 110 - 03/20/2017

- line 120 - 03/31/2017

- line 130 - 30,000

- line 140 - 3 900

Example (vacation pay accrued in one quarter, paid in the next quarter)

Vacation pay of 30,000 rubles was accrued on March 31, 2017, paid on April 4, 2017, personal income tax - 3,900 rubles was transferred on the day the vacation pay was paid. The specified vacation pay is not reflected in the calculation of 6-NDFL for the 1st quarter of 2017. They are reflected in the calculation of 6-NDFL for the first half of 2017

- line 020 - 30 000

- line 040 - 3 900

- line 070 - 3 900

- line 100 - 04/04/2017

- line 110 - 04/04/2017

- line 120 - 04/30/2017

- line 130 - 30,000

- line 140 - 3 900

Example (vacation pay was paid in December of one tax period, the deadline for transferring personal income tax is in the next tax period)

On March 24, 2017, on the day of dismissal, compensation for unused vacation was paid in the amount of 30,000 rubles, including personal income tax of 3,900 rubles.

- line 020 - 30 000

- line 040 - 3 900

- line 070 - 3 900

- line 100 - 03/24/2017

- line 110 - 03/24/2017

- line 120 - 03/31/2017

- line 130 - 30,000

- line 140 - 3 900

Webinars for accountants at Kontur.School: changes in legislation, features of accounting and tax accounting, reporting, salaries and personnel, cash transactions.

Every worker has the right to annual paid rest of at least the duration established by law. Article 114 of the Labor Code of the Russian Federation also obliges the employer to preserve the employee’s place of work, position and average earnings during the vacation.

Labor Code of the Russian Federation on the timing of receiving vacation benefits

Annual paid leave is provided to each employee. This right is enshrined in law by the corresponding article of the Labor Code of the Russian Federation.

The duration of annual paid leave usually does not exceed 28 calendar days. Longer vacations are established for certain categories of workers, for example, for workers of the Far North, employees of hazardous industries, etc.

The legislator provided for the preservation of the average earnings of the working person during the annual rest period allotted to him. Payment for this period is set according to a formula.

By multiplying the number of days of rest by average earnings, the amount of vacation pay is determined. To calculate average daily earnings, a calculation period of 12 months is taken and payments are made only for the time actually worked. Disability benefits and various social benefits are not taken into account.

The period for which vacation pay is paid is established by Part 9 of Article 136 of the Labor Code of the Russian Federation. Vacation pay must be paid no less than 3 days before the start date of the vacation. Earlier it is possible to pay vacation pay, but later it is not. In case of delay in payment of benefits due to the fault of the enterprise, the employee is entitled to compensation.

It is also not very convenient to make a payment earlier than three days in advance. Various circumstances may arise in which going on vacation will have to be postponed (for example, illness). Therefore, it is optimal to accrue and pay vacation pay 3 days before the start date of the vacation.

Despite the fact that the above-mentioned article of the law does not specify the status (calendar or working) of these three days, there is a special letter from Rostrud (No. 1693-6-1 dated July 30, 2014), according to which the counting must be carried out in calendar days. Three calendar days before the start of the vacation, benefits must be paid.

Late payment of vacation pay

Administrative liability for an employer who has not notified an employee of the vacation entitled to him by law or who has committed such a violation of the Labor Code of the Russian Federation as failure to pay vacation pay on time is provided for in Art. 5.27 Code of Administrative Offenses of the Russian Federation:

- for officials, a warning or fine from 1 to 5 thousand rubles;

- for entrepreneurs a fine of 1 to 5 thousand rubles;

- for organizations a fine of 30 to 50 thousand rubles.

Find out at what time he can count on vacation, working the right from the vacation schedule, the preparation of which everyone is notified against signature. If there is no such schedule, the employee writes a statement.

The vacation application was submitted less than 3 days before the expected vacation date

Most likely, such leave will not be issued: the employer will not have time to make calculations and pay vacation pay.

Although the Labor Code of the Russian Federation does not regulate the time for submitting an application for vacation, given that vacation pay must be paid 3 days before its start, the application must be submitted at least 4 days in advance. Otherwise, the employer simply will not have enough time to complete the registration and payment within the period established by law.

It is worth noting that in most cases it is not necessary to apply for annual paid leave. The fact is that enterprises draw up a vacation schedule, of which the employee is notified in advance, against signature.

When the deadline established by the schedule approaches, the director issues an order to grant vacation, and the accounting department calculates vacation pay based on it. The employee, having read the order, puts his signature on it as a sign of consent.

If an employee requires paid leave, but not at the time established by the vacation schedule, he must write an application at least 4-14 days before the expected date of departure.

Watch the video below about the timing of vacation pay:

If the last of three days before the issuance of vacation pay coincides with a weekend

As mentioned above, vacation pay must be issued no less than three days before the first day of vacation. The deadline for paying vacation pay in 2019 remains the same; no changes regarding the norms established by law have been adopted.

If the third day is a weekend or non-working day, the payment must be made taking this into account, that is, 4 or 5 days in advance.

For example, an employee is scheduled to go on vacation starting May 10, 2017. His vacation pay must be paid no later than May 7. Considering that May 7 is Sunday, and May 6 is Saturday, the day the benefit is issued is shifted. Even if the accounting department works on Saturdays and makes a transfer to the card, the bank is not working, which means the employee will not receive the money. Therefore, payment of vacation pay must be made no later than May 4-5, 2017.

Ask questions in the comments to the article and get an answer from an expert

Vacation from the 1st day of the month in 1C: Salaries and personnel management 8th edition 3.1

The situation when an employee goes on vacation from the 1st day of the month quite often raises questions from our clients and readers: vacation pay must be paid 3 days before the start of the vacation, the previous month has not yet been fully worked out, and wages have not been accrued, but this month must be included in the calculation of the average. Previously, I advised my clients to simply recalculate the vacation accrual document after the final calculation of salaries for the previous month, but with the advent of 6-NDFL, the situation has changed a little.

Let's consider an example in the 1C program: Salaries and personnel management 8th edition 3.1. To calculate vacation pay, go to the “Salary” tab and select the “Vacation” item.

Add a new document and carefully fill out all fields. The vacation begins on October 1, the payment date is September 28, and we select September as the accrual month.

If we look at the calculation of average earnings, we will see that wages for September were not included in it.

We pay vacation pay to the employee in the amount calculated according to this document, then we calculate and pay the salary for September.

After data on wages for September appears, vacation pay needs to be recalculated. Until 2016, you could simply go into a previously created document, recalculate it and pay the employee the difference in amounts if average earnings increased. But with the advent of 6-personal income tax, the situation has changed: now we calculate and pay personal income tax in the context of the dates of receipt of income, the vacation tax was calculated on the date September 28, then was withheld and transferred to the budget, so now it is not advisable to recalculate this personal income tax. If the amount of vacation pay increases, and this change is reflected in the same date of receipt of income, then it turns out that we have underpaid the tax to the budget, so we need to act differently. Open the vacation accrual document again and pay attention to the lower left corner of the form.

If wages for the previous month have been calculated and paid, a “Correct” link appears in the document and a warning message stating that it is not recommended to make changes to the existing document. But the “Fix” command is just right for our purpose. When you click on the link, a new document is created in which the amount of vacation pay is recalculated, while the previous amount is reversed and a new one is added, taking into account the last payroll calculation.

In our case, the average earnings have increased, we promptly pay the difference in vacation pay to the employee, and the date of receipt of income, which will be reflected in 6-NDFL, will be a different date - October 5.

For many years now, filling out form 6-NDFL has been raising questions from the accountant, one more intricate than the other. Situations with vacation pay also did not escape this fate. And the main problem is that they have their own rules for withholding personal income tax, which differ from wages and other payments. In addition to the vacation pay itself, many questions arise about compensation for unused vacation upon dismissal.

Colleagues, I would like to reassure you right away! In the situation with vacation pay, and even with compensation, when filling out 6-NDFL, everything is quite logical and obeys simple rules. In this article we will look at this with practical examples. What are we going to talk about?

1. Where do the difficulties with 6-NDFL come from?

2. Date of receipt of vacation pay in 6-NDFL

3. Date of deduction of personal income tax from vacation pay in 6-NDFL

4. Deadline for transferring personal income tax from vacation pay to 6-NDFL

5. Vacation pay in section 1 of the 6-NDFL report

6. How to show vacation pay in 6-NDFL

9. We reflect vacation pay along with salary in 6-NDFL

So, let's go in order.

1.Where do the difficulties with 6-personal income tax come from?

Before you figure out how to show vacation pay in 6-NDFL, you should understand that the solution to any situation that arises follows from the logic of constructing the reporting form itself. The report on Form 6-NDFL is submitted quarterly and completed on the reporting date - March 31, June 30, September 30, December 31. It includes two sections, the principles of including income and tax in which are not the same:

Section 1 is filled in with a cumulative total throughout the year, i.e. income and tax are reflected in it in total. It includes income that is considered received by the employee.

Section 2 includes only those transactions that were performed over the last 3 months. Moreover, the main criterion for inclusion in this section is that the personal income tax payment deadline falls within this reporting period (not the actual deadline, but the deadline according to the law).

The main difficulties in filling out are related to the fact that the dates of receipt of income, its deduction and transfer of personal income tax differ and may fall into different reporting periods. This is also true for vacation pay. Therefore, first of all, let’s look at how the date of receipt of income for vacation pay is determined, the date of tax withholding, and what are the deadlines for transferring personal income tax for this type of income. By the way, if your organization pays dividends, then fill out 6-NDFL for this type of payment.

2. Date of receipt of vacation pay in 6-NDFL

Holiday pay, as defined by the Supreme Court, is part of wages. However, the date of actual receipt of income in the form of vacation pay is determined not by wages, but by paragraph 1 of clause 1 of Article 223 of the Tax Code of the Russian Federation (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 02/07/2012 No. 11709/11, letter of the Ministry of Finance dated 01/26/2015 No. 03-04-06/2187, etc.).

Those. for the purposes of calculating personal income tax the date of receipt of vacation pay in 6-NDFL is the day of payment to the employee— transfers to a bank account, withdrawals from the cash register (letter of the Federal Tax Service dated July 21, 2017 No. BS-4-11/14329@).

According to Article 136 of the Labor Code, the employer is obliged to pay vacation pay no later than 3 calendar days before the start of the vacation (there is also a letter from Rostrud dated July 30, 2014 No. 1693-6-1 on this topic).

The start date of the vacation does not matter, even if it falls on the next calendar month. It doesn’t matter if the vacation is transferable and affects different months, quarters, calendar years (letter of the Federal Tax Service of Russia dated May 24, 2016 No. BS-4-11/9248). To determine the date of receipt of income, only the date of payment of vacation pay is important. For this date, line 100 of form 6-NDFL is filled out.

The date of payment of vacation pay determines whether the amount of vacation pay and personal income tax on it falls into section 1.

3. Date of deduction of personal income tax from vacation pay in 6-NDFL

The next important step to show vacation pay in 6-NDFL is to determine the tax withholding date, which is reflected in line 110. Everything is very simple here: Personal income tax is withheld at the time of payment of income(Clause 4 of Article 226 of the Tax Code). Therefore, for vacation pay, the date of receipt of income and the date of withholding personal income tax from vacation pay in 6-NDFL will coincide, i.e. this is one day.

4. Deadline for transferring personal income tax from vacation pay to 6-NDFL

In general, for most types of income, the deadline for transferring personal income tax to the budget is no later than the first working day following the day the income is paid. But the picture is different for vacation pay! Because the deadline for transferring personal income tax from vacation pay is regulated by a separate norm - clause 6 of Article 226 of the Tax Code. Tax must be remitted no later than the last day of the month in which the payment took place.

On the one hand, this rule is designed to simplify accounting and reduce the number of payments, especially with a large number of employees. Because during the month the tax agent can “accumulate” the amount of tax on vacation pay, and at the end of the month transfer it in a single payment.

But for an accountant, due to his heavy workload, sometimes it is actually easier to transfer personal income tax as soon as the employee’s vacation pay is paid, so as not to forget about it in the future and not delay the transfer. The Tax Code does not prohibit this, so do what is most convenient for you.

The deadline for transferring personal income tax from vacation pay to 6-personal income tax is reflected in line 120. to help you pay the tax.

5. Vacation pay in section 1 of the 6-NDFL report

So, we have sorted out the dates reflected in Section 2, a little later we will analyze problematic situations and look at an example of how vacation pay is reflected in 6-NDFL. In the meantime, just a few words about Section 1, everything is simple here.

This section includes income accrued to employees. For salaries, this is the last day of the month, and for vacation pay, as we have already found out, it is the payment day.

Those. if the payment of vacation pay took place in this period (or in previous ones, since the section is filled in with an accrual total), then their amount falls into Section 1. And personal income tax from vacation pay will fall into lines 040 and 070 of form 6-NDFL (calculated and withheld tax ).

6. How to show vacation pay in 6-NDFL

Let's look at a practical example. First, we will discuss the specific situation and all the dates for it, then we will see how it looks in the reporting form.

Employees of Bashmachok LLC are going on another vacation (dates taken for 2018):

- — warehouse manager Bosonozhkina B.B. from March 5 to 10 days, vacation pay in the amount of 9800 rubles, payment on February 28;

- - Secretary of Tufelkina T.T. from March 19 to 28 kd., vacation pay in the amount of 21,500 rubles, payment on March 15;

- — seller Sapozhkova S.S. from April 2 to the 14th day, vacation pay in the amount of 12,300 rubles, payment on March 29.

Personal income tax for each employee was transferred simultaneously with the payment of vacation pay, on the same day.

The dates for receiving vacation pay and the dates for withholding income will be as follows:

- — Bosonozhkina: February 28

- — Tufelkina: March 15

- — Sapozhkova: March 29.

These are the dates for vacation pay. According to these dates, we fill out Section 1 and lines 100 and 110 of Section 2.

The personal income tax transfer dates will be as follows (data for lines 120):

- — Bosonozhkina: February 28 (this is the last day of the payment month – February)

- — Tufelkina: April 2 (since the last day of the month – March 31 – falls on Saturday)

- — Sapozhkova: also on April 2 (for the same reason).

Each of these payments will be shown separately in Section 2, because There are no payments with a completely matching set of dates (terms 100, 110, 120) in the example. In reality, if you pay vacation pay to several employees on the same day, then they can be combined for Section 2. By the way, the date of actual transfer of personal income tax for them will not matter whether you transferred it on the same day or not.

Now let's see how the data in our example will look in 6-NDFL. For all female employees, vacation pay in Section 1 of the 6-NDFL report will be reflected in the 1st quarter. To simplify, let’s assume that there were no other payments in the organization.

With Section 2 the situation will be more complicated. In what period will the paid vacation pay be included in the report for the 1st quarter or for the half year? Let me remind you that this is determined by line 120 – the date of tax transfer (according to the Tax Code, not the actual one).

We have the following sets of dates:

Thus, each payment will be entered into Section 2 as a separate block. And only Bosonozhkina’s vacation pay will be included in the 6-NDFL report for the 1st quarter.

Vacation pay for Tufelkina and Sapozhkova will be included in Section 2 only in the half-year report.

If March 31 was not a day off, then these vacation pay would also be included in the report for the 1st quarter.

You can see that when it comes to vacation pay, everything turns out quite logically! The example already shows how “carrying over” vacation pay is included in the report, as well as payments for vacations that begin in the next reporting period.

However, many questions arise about how to show January vacation pay in December in 6-NDFL. The problem, in my opinion, is purely psychological – the long New Year holidays. Otherwise, there are no differences from other “transitional” situations between quarters. Therefore, we will also analyze a small example on the topic.

Once again we repeat the important points on which we rely:

- Vacation pay in Section 1 and lines 100-110 are reflected by the date of their payment.

- The deadline for transferring personal income tax is the last day of the month. If this day falls on a weekend or holiday, then the transfer date for line 120 will be the next business day.

- Line 120 determines the reporting period for which vacation pay and the tax on it in Section 2 will be included.

That's all the “tricks”!

At LLC “Bashmachok” the director is Kozhemyakin K.K. goes on vacation from January 8, 2018. On December 28, 2017, he was paid vacation pay, and personal income tax was transferred on the same day.

- The date of receipt of income and withholding of personal income tax is December 28.

- The personal income tax transfer date is January 9, because December 31st falls on a day off, and the first working day after the New Year holidays is January 9th.

Thus, Kozhemyakin’s vacation pay will fall into Section 1 of the report for 2017:

and in Section 2 of the report for the 1st quarter of 2018.

9. We reflect vacation pay along with salary in 6-NDFL

All situations regarding the payment of vacation pay come down to two cases:

- Vacation pay is paid regardless of salary, as it accrues. In this case, wages and vacation pay are reflected in Section 2 in separate blocks for the following reasons:

- the date of receipt of income will most likely differ (exception is if vacation pay is paid on the last day of the month);

- special procedure for the deadline for transferring personal income tax from vacation pay (the last day of the month of payment).

- Vacation pay is paid along with salary. This may simply be a coincidence of dates, or, for example, an employee takes a vacation and is subsequently fired.

Let’s say vacation pay and wages were paid on the last calendar day of the month and the date of receipt of income in the form of vacation pay and wages, the tax withholding date coincided. But the date of transfer of personal income tax on wages is the next working day, and for vacation pay it is still the same last calendar day of the month. This is the example with Bosonozhkina, discussed above.

Thus, in 6-NDFL, vacation pay along with wages will be reflected in Section 2 in separate blocks.

Let's look at a small example of filling out 6-NDFL in case of vacation followed by dismissal. Let's assume that Tufelkin's secretary T.T. from our example with Bashmachok LLC, goes on vacation for 28 days from March 19 with subsequent dismissal.

Let the settlements with the employee be made on March 16 (Friday, this is her last day of work), she was paid vacation pay in the amount of 21,500 rubles. and wages for March in the amount of 10,400 rubles. Personal income tax from the current account is transferred on the same day.

Despite the fact that the employer transferred to the employee all payments due to her in one amount on one day, we are talking about two independent payments - wages for working days in March and vacation pay.

In the event of termination of the employment relationship before the end of the calendar month, the date of actual receipt of income in the form of wages is considered to be the last day of work for which the income was accrued (clause 2 of Article 223 of the Tax Code). In the example, this is March 16 (since March 17 and 18 are days off for which salaries were not accrued). The deadline for transferring personal income tax is March 19, the next working day.

Vacation pay must be shown in 6-NDFL on the date of receipt of income on March 16, and the deadline for transferring personal income tax is April 2. There will be no differences here from regular vacation pay.

Section 2 of the 6-NDFL calculation for nine months is filled out as follows.

Vacation followed by dismissal is a rare case. Much more often, an employee quits and receives compensation for unused vacation. But the rules here will be the same:

- If an employee resigns, then The date of receipt of income in the form of wages is considered to be the last day of work(Clause 2 of Article 223 of the Tax Code of the Russian Federation).

- The date of receipt of income in the form of vacation compensation is the day of its payment.

Article 140 of the Labor Code of the Russian Federation establishes that upon termination of an employment contract, payment of all amounts due to the employee from the employer is made on the day of the employee’s dismissal. In other words, in the event of dismissal, compensation for unused vacation and wages for the last month worked are paid on one day, which is the last day of work.

Let's take the same example with the secretary of Bashmachok LLC T.T. Tufelkina, assuming that she quits on March 16, receives a salary for March of 10,400 rubles. and compensation for unused vacation 21,500 rubles.

The date of receipt of income and the date of withholding personal income tax for both payments is the same - this is March 16. The deadline for transferring personal income tax from wages is also clear - March 19. But what is the personal income tax transfer date for compensation?

The provisions of Chapter 23 of the Tax Code of the Russian Federation do not contain explanations of what income is classified as income in the form of vacation pay.

From Art. 236 of the Labor Code of the Russian Federation it follows that “vacation payment” and “severance payments” (which also includes compensation for unused vacation) are different in their legal nature. Compensation for unused vacation cannot be considered as part of vacation pay. Therefore, compensation will not have a “special” deadline for transferring personal income tax, as in the case of vacation pay. The general rule applies - We transfer no later than the next business day.

Therefore, personal income tax on compensation for unused vacation upon dismissal can be reflected in 6-personal income tax together with personal income tax on wages. In our example, this is March 19th.

Tufelkina’s salary and the compensation paid to her for unused vacation in lines 100-140 of form 6-NDFL will be reflected in the aggregate; there is no need to fill out these lines separately for income in the form of compensation for unused vacation.

Thus, we figured out how to show vacation pay in 6-NDFL. The only issue that was not touched upon was the situation with recalculation. The need for recalculation may be required not only in the case of arithmetic errors made by the accountant.

There is often a need early recall of an employee from vacation. And he will use the rest of his vacation separately in the future. Those. the employee initially received vacation pay for more days than he used.

Before we look at the recalculation of vacation pay in 6-NDFL using a practical example, remember the basic rules:

- The amount of income actually received in 6-NDFL is indicated already counted.

- The amount of tax withheld in 6-NDFL is indicated actual, i.e. the one that was initially retained.

On May 14, the manager of Bashmachok LLC Shnurkov A.A. vacation pay was paid in the amount of 19,600 rubles for 28 days of vacation (from May 18 to June 15). On the same day, personal income tax in the amount of 2,548 rubles was transferred to the budget.

But on June 5, the employee was recalled from vacation. As a result of recalculation, vacation pay for 18 days (from May 18 to June 4) amounted to 12,600 rubles. (Personal income tax - 1638 rubles).

For June, the employee was entitled to a salary of 20,000 rubles. (Personal income tax - 2600 rubles).

On July 5, the employee received his salary for June, reduced by the amount of vacation pay for those days when he was recalled from vacation, that is, by 7,000 rubles. (for 10 calendar days from June 5 to June 15). As a result, the salary amounted to 13,000 rubles. And personal income tax must be paid in the amount of 2600 – (2548 – 1638) = 1690 rubles.

This is how the situation will be reflected in Section 2 of the 6-NDFL report.

Since the salary payment for June took place in July, the report for the half-year will include vacation pay, and the report for 9 months will include salary.

If you have questions about how to show vacation pay in 6-NDFL, ask them in the comments!

28 thoughts on “ How to show vacation pay in 6-NDFL - practical examples”

Thank you very much for such a clear explanation of this tricky report! There were always some problems with these vacation and sick pay. I never assembled 1C correctly. Everything has to be adjusted manually. There were disputes with the chief accountant regarding the reflection of vacation and sick pay in the calculations. But now all problems have been eliminated.

Thank you very much. Everything is presented in very detail and clearly. I figured out this report myself through trial and adjustment. But many people have great difficulty filling it out.

Julia and Dina, thank you SO MUCH! Everything is very accessible and competent. You are WELL DONE!

Thank you for such a detailed and clear article! Everything is clear when the payments went through as expected. But I’ve got this mess, maybe you can help me deal with it in the best possible way? A swarm of thoughts in my head, I would also like to hear your opinion :))

We paid salaries for December on December 28, 2017. and on the same day the personal income tax was transferred. On December 29, resignations were received, they had to be satisfied and additional compensation for unused vacation was added and included in the payroll for December. It was not possible to pay compensation on the day of dismissal (December 29) and transfer personal income tax from it. These payments were made only on January 9, 2018. Which sections and columns of the 6-NDFL report for 2017 include compensation for unused vacation?

Hello Antonina! The date of receipt of income for compensation for unused vacation is the date of its payment, i.e. in your case 01/09/2018. Consequently, this compensation will not fall into sections 1 and 2 of the report for 2017, but will be reflected in both of these sections for the 1st quarter of 2018. But there are consultants who have a different opinion on this matter in this situation, so you will have to make the decision yourself.

Julia, thank you for your answer!

In January 2018, the employee went on vacation on January 9, 2018, personal income tax from vacation pay was transferred on January 10, 2018, and personal income tax for December was transferred on January 15, 2018. How to indicate personal income tax in the report. Thank you.

If you mean filling out section 2, then it is impossible to answer your question, because. you did not indicate the dates of payment of vacation pay and salaries. The actual dates of personal income tax transfer do not matter.

The employee was given vacation pay on March 21, 2018 in the amount of 30,900, but the employee has a property deduction for the apartment. It turns out that the amount of income is not taxed. Should this be reflected in the report and how?

The amount of the property deduction provided to the employee, as well as other deductions, is reflected on line 030 of form 6-NDFL. If you have already submitted a calculation without a deduction, then you need to submit an amendment.

Good morning! Great article, thank you very much!

Please tell me if a person was fired on March 30th. Payment and transfer of personal income tax were also made on March 30. In section 1 I include this amount in the first quarter (fill out line 20, 40, 70).

And in the second section, in what period should I include these amounts. After all, the deadline for transferring personal income tax falls on April 2! It turns out that there will be 2 quarters in section 2?

Hello Anna! Yes, you wrote everything correctly. In section 1 - already for the 1st quarter, in section 2 - in the half-year report.

The article is wonderful. Just about the artsy-twisted. Many thanks to the author.

Good afternoon, Yulia! Thank you so much for this article, the clearest explanation I have ever read.

Hello! The employee went on vacation on May 27, 2018. But I received my vacation pay on payday, i.e. 04.06. And personal income tax was also withheld and paid to the budget on June 04. It is clear that it is a violation. But what is the best way to fill out 6-NDFL. p100 06/04/18, p110 06/04/18, p120 05/31/18? And below is the salary block p.100 05/31/18, p.110 06/04/18 and p.120 06/05/18. Or should we spread everything out in one amount (i.e. not allocate vacation pay?). Most likely they won’t come to check, but the report immediately shows the violation and threatens with a 20% fine?

Good afternoon

Please help me figure it out. If vacation or sick leave was paid in June 2018, and the transfer deadline falls on 07/02/18. Then in section 2 these amounts will fall into 6NDFL for the 3rd quarter. Question. And in line 070 of section 1, should we reflect the withheld personal income tax when paying income for the 2nd or 3rd quarter?

Thanks in advance.

Good afternoon.

How to fill out section 1 if the vacation is from 14/06/18 to 27/06/18? But it was paid to the employee only on 07/05/2018. Personal income tax is also listed on 07/05/2018.

The program includes these vacation pay on line 020, personal income tax on these vacation pay is included on line 040 (calculated). But they do not appear on page 070, but are included in page 080 as not retained. It's like that?

Good evening, please tell me, at the end of May vacation and personal income tax were accrued and paid, in June, when calculating salaries, it turned out that May was not included in the employee’s calculation, they recalculated vacation pay, paid additional vacation and personal income tax with salary together, tell me how to reflect vacation pay and personal income tax in counting?

Hello, please tell me, if vacation pay was paid on June 15, part of personal income tax from vacation pay was withheld on June 15, the second on July 2, then in which report will 6-personal income tax holiday pay be included for six months or 9 months? And what will be the date of personal income tax withholding on line 110? Thank you

Hello! The situation is not entirely clear. Did you not fully withhold personal income tax when paying? Or did they keep everything that was due, but transferred it in two parts? If the second, then in section 2 there will be a record for 9 months, the withholding date is June 30, the transfer date is July 2.

Hello! Thanks for the interesting question. To make it easier to answer, let’s conditionally enter the dates. Let’s assume that the payment of vacation pay took place on May 28, the vacation began on June 1, and the salary with the rest of the vacation pay was paid on June 7.

With Section 1, everything will be simple; it will reflect accrued vacation pay along with additional payment, salary (line 020). Personal income tax will be included in both calculated and withheld tax (lines 040 and 070).

For vacation pay, the date of receipt of income is the date of payment of vacation pay. For salaries - the last day of the month. Personal income tax is withheld on the date of payment. Personal income tax on vacation pay must be transferred no later than the last day of the month in which it was paid.

Then in Section 2 of form 6-NDFL for the six months there will be 2 blocks:

Vacation pay paid before recalculation:

05.28.18 - amount of vacation pay

05.28.18 - personal income tax amount

31.05.18

Salary paid (together with other employees):

05/31/18 - salary amount

06/07/18 — Personal income tax from salary

08.06.18

And the additional payment for vacation pay will have to be reflected in Section 2 for 9 months:

06/07/18 - amount of additional payment for vacation pay

06/07/18 — Personal income tax from additional payment for vacation pay

07/02/18 (since June 30 is a day off)

Hello, Elena! If vacation pay was paid in July, then it should go to line 020 in July, because the date of income for vacation pay is the date of payment. Accordingly, personal income tax for the six months will not fall within the 040, 070, or 080 deadlines.

If you have 1C: Accounting, then it has a chronic problem with line 080. 06/04/18

07/02/18 (since June 30 is a day off)

When you had to pay them according to the law does not matter here. Only the date of actual payment matters. And the report doesn’t show that you violated anything.

Good afternoon

Tell me how to reflect the amounts of vacation pay in 6-NDFL in the case when various deductions are made from the amounts of vacation pay (alimony, cost of work clothes, etc.). Those. the employee receives part of the vacation pay. The second part in the form of alimony (etc.) is transferred for its intended purpose, usually on the day of payment of wages, i.e. These are completely different dates. And what about personal income tax in this case??? Show in full at the time of transferring vacation pay to an employee? or in proportion to the amounts of vacation pay paid and the amounts withheld from vacation pay?

Hello! Alimony is withheld after personal income tax is withheld. Therefore, personal income tax is withheld at the time of payment of vacation pay. Those. On the date of payment of vacation pay, show the entire amount of personal income tax as withheld.

Good evening everyone. I’ve already read so much about filling out the 6-NDFL, but I still haven’t found the answer to my question. I would be grateful if you could clarify. Let’s say an employee went on vacation on October 4, 2018. Firstly, when should I pay him vacation pay and withhold tax from it? Secondly, I transferred personal income tax on October 8, it was so convenient for me. What dates should I put in the second section of the 6-personal income tax? 100-01.10.18, 110-01.10.18, 120-31.10.18? The question essentially is, if personal income tax is transferred not on the last day of the month, but earlier, then. October 8th, then should I put October 8th in line 120 or is it still the last day of the month? Or did I break the law, I have to pay on the last day of the month?

Hello! 1) Vacation pay had to be paid no later than September 28. Because if paid on October 1, only 2 days remain before vacation payment, not 3. On the same day, September 28, withhold the tax and transfer no later than October 1 (postponement from September 30). 2) You did not write when the vacation pay was actually paid, but apparently it was October 1. Then 100-01.10.18, 110-01.10.18, 120-31.10.18 are correct. In line 120 the day according to the law is written, i.e. the last day of the month or the nearest working day if the end of the period falls on a weekend. You can pay personal income tax on any day from the date of transfer of vacation pay until the end of the month.