Fundamentals of accounting for fixed assets. Organization of accounting of fixed assets Fixed assets of the enterprise

Fixed assets can be received by the enterprise in one of the following ways:

1.Purchase for payment or in exchange for other property;

2.Construction and manufacturing;

3. Contribution by the founders to the account of contributions to the authorized capital;

4.Free receipt;

5.In other cases.

Accounting for the availability and movement of fixed assets owned by the enterprise is carried out on active account 01 “Fixed Assets”.

Account 01 “Fixed Assets” reflects fixed assets at historical cost:

The cost of buildings, structures, equipment, vehicles and other individual fixed assets acquired by the enterprise is reflected using account 08 “Investments in non-current assets”. This account is used to reflect in accounting all the costs of the enterprise associated with the acquisition and commissioning of fixed assets, and, thus, performs the functions of a calculation account. Analytical accounting for account 08 is maintained for each acquired or created object.

The inventory value of buildings, structures, equipment, vehicles and other individual fixed assets consists of the actual costs of their acquisition and the costs of bringing them to a state in which they are suitable for use for the planned purposes.

Fixed assets purchased for a fee from other enterprises and persons, as well as those created at the enterprise itself, are reflected in the debit of account 01 “Fixed assets” and the credit of account 08 “Investments in non-current assets”. Fixed assets received from other organizations and persons free of charge are reflected in the debit of account 08 and the credit of account 98 “Deferred income” at market value; when putting into operation a fixed asset received free of charge, its value is written off from the credit of account 08 to the debit of account 01 “Fixed assets” facilities". Depreciation on these fixed assets is accrued in the generally established manner; at the same time, debit 98 and credit 91 “Other income and expenses” are posted for the amount of accrued depreciation charges.

Acceptance for accounting of fixed assets contributed by the founders on account of their contributions to the authorized capital is reflected by posting debit 08 credit 75, then debit 01 credit 08.

When purchasing fixed assets from a foreign supplier (for import), the initial cost of fixed assets is the amount of actual costs for their acquisition. Costs incurred by an organization in foreign currency are reflected in the corresponding accounting accounts in rubles at the exchange rate of the Central Bank of the Russian Federation on the date of the transaction. When the received fixed asset is accepted for accounting, the exchange differences that arise are written off to account 91 “Other income and expenses.”

Under a fixed asset lease agreement, the lessor undertakes to provide the tenant with the property for temporary possession for a fee. The lessor records the leased property on its balance sheet as part of its own fixed assets. The lessee records property received for temporary use under a lease agreement in off-balance sheet account 001 “Leased fixed assets.”

An enterprise can independently manufacture or construct fixed assets. In this case, the debit of account 08 “Investments in non-current assets” reflects all the actual costs of the enterprise associated with the creation of the facility, namely: the cost of materials used, wages of employees and contributions to extra-budgetary funds, the cost of work by third-party organizations, depreciation of fixed assets of the enterprise, used to create a new fixed asset, other expenses. This method of creating fixed assets is called economic.

An organization may also enter into an agreement for the creation of fixed assets with a specialized organization. In this case, the debit of account 08 will reflect the cost of work performed in accordance with the contract. This method of creating fixed assets is called contracting.

When purchasing fixed assets, the buyer, in addition to the cost of the fixed asset, pays the seller the amount of value added tax. The amount of VAT on the acquisition of fixed assets is taken into account on b/ac 19 subaccount “Value added tax on the acquisition of fixed assets”. After actual payment and if there is an invoice, this VAT amount is written off from the credit b/ac 19 -1 to the debit b/ac 68 “Calculations with the budget”.

Subaccount 19-1 “Value added tax on the acquisition of fixed assets”, active:

When equipment requiring installation is received, its cost is reflected in the debit of account 07 “Equipment for installation” in correspondence with account 60 “Settlements with suppliers and contractors”. The amount of VAT on received equipment is reflected in the debit of account 19 “VAT” and the credit of account 60.

Installation of equipment is recorded by the presence of expenses in a certificate of the volume of work performed on the installation of this equipment, drawn up in the prescribed manner.

When carrying out construction and installation work using an economic method, the cost of equipment transferred for installation is written off from the credit of account 07 to the debit of account 08.

Account 07 “Equipment for installation”, active:

Accounting for depreciation of fixed assets.

Depreciation(depreciation) is a reflection of the cost of physical and moral depreciation of fixed assets. Depreciation makes it possible to transfer part of the book value of fixed assets to the cost of production.

If materials and raw materials are written off to cost as they are written off for production in full, then fixed assets are written off in parts.

Firstly, this is due to the fact that fixed assets are not transferred directly to products (works, services). Secondly, the service life of fixed assets exceeds one year. Thirdly, the cost of fixed assets is usually high and including it immediately in the cost price will cause undesirable financial consequences.

Depreciation of fixed assets is carried out using one of the following methods of calculating depreciation charges:

linear method

reducing balance method

method of writing off cost by the sum of numbers of years of useful life,

method of writing off cost in proportion to the volume of products (works, services).

The application of one of the methods for a group of homogeneous fixed asset objects is carried out during the useful life of the fixed asset object. The useful life of an item of fixed assets is determined by the organization when accepting the item for accounting.

The useful life of a fixed asset item is determined based on:

the expected life of the facility in accordance with its expected productivity or capacity;

expected physical wear and tear, depending on the operating mode (number of shifts), natural conditions and the influence of an aggressive environment, the repair system;

regulatory and other restrictions on the use of this object (for example, rental period).

In cases of improvement (increase) of the initially adopted standard indicators of the functioning of a fixed asset object as a result of reconstruction or modernization, the organization revises the useful life of this object.

During the useful life of an object of fixed assets, the accrual of depreciation charges is not suspended, except in cases where they are under reconstruction and modernization by decision of the head of the organization, and fixed assets transferred by decision of the head of the organization for conservation for a period of more than 3 months.

Fixed assets costing no more than 2,000 rubles per unit, as well as purchased books, brochures, etc. publications are allowed to be written off as production costs (sales costs) as they are released into production or operation. In order to ensure the safety of these objects in production or during operation, the organization must organize proper control over their movement. Objects of fixed assets whose consumer properties do not change over time (land plots and environmental management facilities) are not subject to depreciation.

The accrual of depreciation charges for an object of fixed assets begins on the first day of the month following the month in which this object was accepted for accounting, and is carried out until the cost of this object is fully repaid or this object is written off from accounting.

The accrual of depreciation charges for an object of fixed assets ceases from the first day of the month following the month of full repayment of the cost of this object or the write-off of this object from accounting.

At linear method, the amounts of deductions are the same for the entire period of operation. The second and third methods are nonlinear. When they are used, the amount of depreciation charges in previous years is greater than in subsequent years.

Using reducing balance method the annual amount of accrued depreciation is determined based on the residual value of the fixed asset item, accepted at the beginning of each reporting year, and the depreciation rate calculated when registering this item based on its useful life and the acceleration factor, which is established by the legislation of the Russian Federation. Currently, it is possible to apply increasing coefficients in accordance with Decree of the Government of the Russian Federation dated 08/19/94 No. 967 (as amended on 06/24/98).

Depreciation is calculated using the following formula:

And = First *(On /100)*(K1 + K2 + ... +Kn - n + 1), Where

AND- depreciation for the reporting period,

First- initial cost of fixed assets,

On- depreciation rate,

TO- correction factors (applied in case of deviation from the standard conditions for the use of fixed assets).

The amount of depreciation for fully depreciated fixed assets is not accrued.

Accounting for accumulated depreciation on fixed assets is carried out on account 02 “Depreciation of fixed assets”, on the credit of which the amount of annual depreciation charges is recorded, and on the debit - the accumulated depreciation of sold, liquidated or otherwise disposed of fixed assets.

Account 02 “Depreciation of fixed assets”, passive:

Analytical accounting for account 02 “Depreciation of fixed assets” is carried out by type and individual inventory items of fixed assets.

By accruing depreciation, the enterprise transfers part of the cost of fixed assets to the cost of fixed assets, which is equal to the difference between the original (replacement) cost and depreciation.

In the balance sheet, this process is reflected by a decrease in non-current assets, which are accounted for at their residual value.

Depreciation is not charged for:

machines, equipment and other similar means of labor that are listed at the enterprise as goods or finished products;

housing stock;

external improvement facilities and other similar forestry, road facilities, specialized navigation facilities, etc.;

productive livestock, buffalo, deer;

perennial plantings that have not reached operational age;

mobilization capacities, unless otherwise provided by the legislation of the Russian Federation.

The accrual of depreciation is suspended on objects that, by decision of the head of the organization, are undergoing modernization - as work on their restoration with a period of more than 12 months (previously - for a period of 3 months).

Thus, depreciation is accrued for all fixed assets during their useful life, with the exception of the time the objects are in use:

conservation for a period of more than three months. In this case, the conservation procedure is established by the head of the organization, and it applies to objects located in a certain complex, or objects that have a completed production cycle;

restoration (carrying out reconstruction, modernization, major repairs and other repair and restoration work on them) with a period of work exceeding 12 months.

Accounting for costs of maintenance and repair of fixed assets.

Depending on the volume and nature of the repair work carried out, they are divided into: capital And Maintenance fixed assets. They differ in complexity, volume and deadlines.

Current repairs consist of daily maintenance of machinery and equipment in order to maintain them in working order at all times. The scope of work for routine repairs includes lubrication and adjustment of individual components and parts, replacement of some of them with new ones, but without disassembling the unit. For other types of fixed assets (buildings, structures, etc.), other deadlines and a different nature of repairs (whitewashing, painting, etc.) are established.

Major repairs mean:

for equipment and vehicles - complete disassembly of the unit, repair of base and body parts and assemblies, replacement or restoration of all worn parts and assemblies with new and more modern ones, assembly, adjustment and testing of the unit;

for buildings and structures - replacement of worn-out structures and parts or replacing them with more durable and economical ones that improve the operational capabilities of the objects being repaired, with the exception of the complete replacement of the main structures, the service life of which in a given object is the longest (stone and concrete foundations of buildings, pipes of underground networks , reel supports, etc.).

Repairs of fixed assets can be carried out in-house (by the organization itself) or by contract (by third-party organizations).

In both cases, a list of defects is created for each repaired object. It states:

work to be performed

start and end dates of repairs,

parts scheduled for replacement,

time standards for work and production of replacement parts,

estimated cost of repairs by expense item.

Organizations can debit actual expenses associated with carrying out repairs or paying for repairs of fixed assets to the debit of production cost accounts (20 “Main production”, etc.) from the credit of the corresponding material, cash and settlement accounts (account 10 “Materials” , 70 “Payroll calculations”, etc.). In the accounts of production costs and distribution costs, expenses for the repair of fixed assets are reflected according to the corresponding cost elements (material costs, labor costs, etc.).

For major repairs carried out by contract, the organization enters into an agreement with the contractor. Acceptance of completed major repairs is documented by an acceptance certificate (form no. OS -3). Completed capital works are paid to the contractor based on the estimated cost of their actual volume.

Organizations can create a repair fund to accumulate funds for repair work, especially in organizations with seasonal production. To account for the repair fund, a subaccount “Reserve for repairs of fixed assets” is opened to account 96 “Reserves for future expenses”.

Subaccount “Reserve for repairs of fixed assets” to account 96 “Reserves for future expenses”, passive:

Account 96 “Reserves for future expenses”

Organizations can initially account for the costs of repairing fixed assets as a debit to account 97 “Deferred expenses” (from the credit of material, settlement and other accounts), and from this account, as a rule, evenly write off throughout the year to production (circulation) costs. This option for accounting for the costs of repairing fixed assets is advisable to use in those organizations in seasonal industries where the bulk of the costs for repairing fixed assets occur in the first months of the year, when the repair fund has not yet been created.

VAT on expenses for repairs of fixed assets, carried out both by business and contract methods, is accounted for on account 19 in the generally established manner. A subaccount “Value added tax on work performed, services provided” can be opened to this account.

Repair and maintenance of fixed assets for non-production purposes is carried out at the expense of the organization's profits. Actual expenses for the repair of such fixed assets are written off to the debit of account 99 “Profits and losses” from the credit of material, cash and settlement accounts (10, 70, 60, 69, 76, etc.). VAT on the repair of fixed assets for non-production purposes is written off as a debit to account 99 and does not apply to the reduction of settlements with the budget.

Accounting for disposal of fixed assets.

The cost of an item of fixed assets that is disposed of or is not constantly used for the production of products, performance of work and provision of services, or for the management needs of the organization, is subject to write-off from accounting.

Disposal of a fixed asset item occurs in the following cases:

sales of other legal entities and individuals;

write-off or liquidation due to moral or physical wear and tear;

transfers under contracts of exchange, donation and other types of gratuitous transfer of objects;

liquidation of fixed assets in case of accidents, natural disasters and other emergency situations;

transfer to the tenant in connection with the transfer of ownership of objects previously leased with the right to purchase;

non-use for the purposes of production of products or work or for other management needs;

for other reasons.

If a fixed asset is written off as a result of its sale, then the proceeds from the sale are accepted for accounting in the amount agreed upon by the parties to the agreement.

Income and expenses from writing off fixed assets from accounting are reflected in accounting in the reporting period to which they relate. Income and expenses from writing off fixed assets from accounting are subject to credit to the profit and loss account as operating income and expenses.

Accounting for disposal of fixed assets is carried out as follows. On account 01, a subaccount “Retirement of fixed assets” can be opened. The debit of this subaccount reflects the initial cost of fixed assets, and the credit reflects the amount of accumulated depreciation on retiring fixed assets. The residual value of the retiring fixed asset is written off to the debit of account 91 “Other income and expenses” in correspondence with account 01.

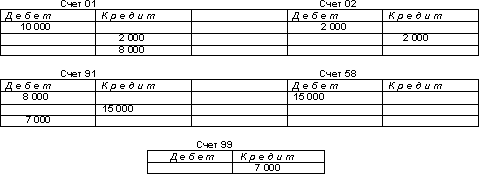

For example, the initial cost of a retiring fixed asset is 10,000 rubles. The amount of depreciation on this fixed asset at the time of disposal was 2,000 rubles.

Fixed assets transferred as a contribution to the authorized capital of other organizations are reflected at the cost determined by agreement of the parties, in the debit of account 58 “Financial Investments” and in the credit of account 91. The initial cost of the transferred fixed assets is written off from the credit of account 01 “Fixed Assets” to the debit subaccount “Retirement of fixed assets”, and the amount of depreciation is the debit of account 02 “Depreciation of fixed assets” and the credit of the subaccount “Disposal of fixed assets”. Additional expenses associated with the transfer of fixed assets are written off to the debit of account 91 from the credit of the corresponding accounts.

For example, the initial cost of a fixed asset subject to contribution to the authorized capital is 10,000 rubles, the amount of depreciation is 2,000 rubles. By agreement of the parties, fixed assets are contributed to the authorized capital at a cost of 15,000 rubles.

2.5. Forms of primary documents for accounting of fixed assets.

Accounting for fixed assets is carried out on the basis of the following primary documents:

act of acceptance and transfer of fixed assets, invoice for internal movement of fixed assets;

act of acceptance and transfer of repaired, reconstructed and modernized facilities;

act on liquidation of fixed assets;

act on liquidation of vehicles, inventory card for accounting of fixed assets;

card for recording the movement of fixed assets, inventory list of fixed assets;

inventory book of fixed assets.

The receipt of fixed assets is documented by an acceptance certificate, which is drawn up and signed by a commission appointed by the head of the enterprise.

The acceptance certificate indicates:

characteristics of the fixed asset item;

its location;

source of financing for its acquisition;

year of manufacture or construction;

date of commissioning;

test results, etc.

Simultaneous acceptance(posting) of the same type of tools, machine tools, household equipment, etc. objects of the same value can be formalized in one act.

Each fixed asset item accepted for accounting is assigned inventory number. It is preserved throughout the entire operation of the object and is indicated on it (a token is attached, an inscription is made with paint, etc.). It is not allowed to assign inventory numbers of written-off fixed assets to newly received objects, as this may lead to accounting errors.

The acceptance certificate is transferred to the accounting department, where an inventory card is created indicating the inventory number of the object and basic data about it (initial or replacement cost, depreciation rates, amount of depreciation at the time of acceptance).

2. 6. Inventory of fixed assets.

The procedure for conducting an inventory of fixed assets and reflecting its results in accounting is regulated by the “Methodological guidelines for the inventory of property and financial liabilities” (approved by order of the Ministry of Finance of the Russian Federation dated June 13, 1995).

Purpose of inventory– confirm the availability of fixed assets in kind at the places of their operation or location according to accounting data.

Inventory of fixed assets is a mandatory procedure in the following cases:

when reorganizing an enterprise (merger, division, accession, separation, transformation) as of the date of drawing up the balance sheet);

when changing financially responsible persons (on the day of acceptance and transfer of cases);

after natural disasters (immediately after their end);

upon detection of facts of theft, as well as damage to such property (immediately after such facts have been established);

in other cases provided for by the legislation of the Russian Federation or regulations of the Ministry of Finance of the Russian Federation.

An inventory of fixed assets can be carried out once every three years, and an inventory of the book stock of libraries - once every five years.

The head of the enterprise has the right to set other deadlines for conducting the inventory. He also determines the composition of the inventory commission.

Before conducting an inventory, the correctness of the preparation of primary accounting documentation on the presence and movement of fixed assets (inventory cards or books, technical passports, acceptance certificates, etc.) is also clarified.

Financially responsible persons must confirm in writing that all incoming and outgoing documents for fixed assets have been submitted to the accounting department. Accepted objects are capitalized, and disposed objects are written off as expenses. This approach will further avoid possible conflicts between members of the inventory commission and persons with financial responsibility.

The actual presence and technical condition of objects are established by members of the inventory commission together with financially responsible persons through direct inspection at the location.

The results of the inspection are entered into inventory lists (form no. inv.-1) manually or by means of computer technology in the context of each name of the object, with the obligatory indication of their inventory number.

Unaccounted for fixed assets, as well as fixed assets for which a shortage has been identified, are recorded in a separate inventory list (form number inv.-18).

For fixed assets used by an enterprise under a lease, regardless of its nature (short-term or long-term), a separate inventory list is drawn up in two copies. One copy remains with the enterprise, and the other is sent to the lessor.

Objects that in accounting belong to the active part of fixed assets (machinery, equipment, vehicles) are shown in the inventory list with a detailed explanation of their technical characteristics and factory inventory number.

If an object has undergone restoration, reconstruction, expansion or re-equipment and, as a result, its main purpose has changed, then it is included in the inventory under the name corresponding to the new purpose.

The commission transfers the appropriately completed inventory records to the accounting department for the preparation of a matching statement. This statement includes only those objects for which there are discrepancies with accounting information.

Identified surpluses of fixed assets are accounted for in the debit of account 01 “Fixed assets” and the credit of account 99 “Profits and losses”. If there is a shortage or damage to fixed assets, the amount of depreciation is written off by posting: debit account 02 “Depreciation of fixed assets” and credit account 01. The residual value of fixed assets is written off from the credit of account 01 to the debit of account 94 “Shortages and losses from damage to valuables.” When specific culprits are identified, missing or damaged fixed assets are assessed at market value and written off from the credit of account 94 to the debit of account 73 “Settlements with personnel for other operations.” The difference between the market price and the residual value of fixed assets is reflected in the debit of account 94 and the credit of account 98 “Deferred income”. As the debtor repays the debt, the corresponding part is written off from account 98 to the credit of account 99 “Profits and losses”.

If the specific culprits are not identified, then the missing and damaged fixed assets are written off from the credit of account 94 for production (circulation) costs by decision of the head of the organization.

1. Fixed assets are assets that have a tangible form, used by an organization in economic activities for a long (more than 12 months) period, the cost per unit of which exceeds the amount established by the accounting policy of the organization in accordance with the law (currently - up to 30 basic units).

Fixed assets of enterprises are varied in type and purpose. For planning, accounting and reporting, they are classified according to various criteria:

Depending on the nature of participation in the reproduction process, fixed assets can be either production or non-production.

By economic sector: fixed assets of industry, fixed assets of agriculture,…

Depending on the purpose and functions of fixed assets, they are divided into the following types:

building; - structures; - transfer devices; - machinery and equipment; - vehicles; - tools; - production equipment and accessories; - household equipment; - working and productive livestock - perennial plantings - capital costs for land improvement; - other (for example, a library ).

Based on ownership, fixed assets are divided into owned, leased, and long-term leased.

Based on their use, fixed assets are divided into operating and non-operating (in warehouse, in reserve, in storage).

Fixed assets are valued at their original cost, replacement cost and residual value.

IN originalthe cost of fixed assets includes the costs of their construction or acquisition, delivery and installation costs.

Under restorativecost refers to the cost of their reproduction in modern conditions. The replacement value of fixed assets is received instead of the original value as a result of revaluation. Fixed assets are reflected at their original or replacement cost on account 01 of accounting. This cost is not subject to change during the entire service life of this fixed asset.

During operation, fixed assets wear out, causing their value to decrease. The monetary expression of the loss of objects of their physical and technical-economic qualities is called depreciation of fixed assets. And the process of transferring this cost to production costs is depreciation. To account for it, account 02 “Depreciation of fixed assets” is used. The original cost minus depreciation is residualcost of fixed assets. In this assessment, fixed assets are shown on the balance sheet.

For each item received, the accounting department creates an inventory card. The initial cost on account 01 remains unchanged throughout the operation of the object, except in cases of revaluation and modernization.

The receipt of fixed assets is documented by an acceptance and transfer certificate (Form No. OS-1) or an acceptance and delivery certificate of repaired, reconstructed and modernized facilities (Form No. OS-3).

The act is drawn up for each individual object by the acceptance committee appointed by order of the head of the enterprise. It indicates the year of manufacture (construction) of the object, the date of entry into operation, the initial cost, the amount of wear and tear, the results of technical inspection and testing.

After registration, the act, together with the attached technical documentation, is transferred to the accounting department for opening inventory cards. The technical documentation is then sent to the technical department (department of the chief mechanic), and the report is sent to the accounting department or to the CC to receive summary documents on the movement of the operating system.

The reasons for the disposal of fixed assets can be: - liquidation of an object completely due to dilapidation, wear and tear, natural disasters, accidents; - liquidation of part of the inventory object in connection with modernization, reconstruction; - free transfer to another enterprise; - sale (for a fee) of unused equipment; - shortage identified during the inventory; - reconstruction and technical re-equipment of the enterprise.

To determine the unsuitability of the OS and prepare the necessary documentation for its write-off, the enterprise creates a permanent commission consisting of: - chief engineer; - heads of structural units (shops, services); - chief accountant or his deputy; - persons who are responsible for safety.

Commission:- inspects the object and establishes its unsuitability for further use and restoration; - establishes specific reasons for decommissioning; - identifies persons through whose fault the OS object was prematurely retired from service; - determines the possibility of using individual components, materials from the decommissioned object and produces them assessment; - controls the withdrawal and delivery of non-ferrous and precious metals to the warehouse; - draws up acts for write-off: act on liquidation of fixed assets (form No. OS-4) or act on liquidation of vehicles (form No. OS-4a). The acts indicate the year of manufacture of the object, the date of receipt by the enterprise, the time of commissioning, the initial cost of the object, the useful life, the amount of accrued depreciation according to accounting data, the number of major repairs carried out, reasons for disposal, liquidation costs, income.

The acts drawn up by the commission are approved by the head of the enterprise. Only after this is it possible to dismantle and disassemble the OS into parts and assemblies. The executed act of liquidation of the OS is transferred to the accounting department of the enterprise, which notes in the inventory card and inventory the date of disposal and the number of the liquidation act. Free transferThe fixed assets and the sale are formalized by an act of acceptance and transfer of the fixed assets, indicating the original cost and the amount of depreciation. An inventory card is attached to the act (a mark is made in the inventory and inventory list). The OS is sent to the recipient enterprise. After receiving notification from them about the posting of objects, the accounting department records the disposal of the object on the accounting accounts.

Depreciation is the process of transferring the cost of fixed assets to the cost of products, works, and services produced with their use in the process of entrepreneurial activity. It includes: - distribution in a rational way of the depreciable cost of objects between reporting periods, which together constitute the useful life of each of them; - systematic inclusion of depreciation charges (the cost of used objects related to a given reporting period) in production costs, sales costs or operating expenses.

The depreciable cost of each fixed asset item used in business activities is included in parts in production costs and costs of selling products, in operating expenses during the useful life not used in business activities - in parts included in non-operating expenses of a commercial organization or repaid from targeted revenues (financing) of a non-profit organization during the standard service life. The standard service life of fixed assets is established in relation to each position of fixed assets included in the current classification of depreciable fixed assets upon its acquisition by each owner.

Depreciation is accrued (depreciation deductions are made) monthly until the cost of the object is fully repaid or its disposal in one of the following ways.

The straight-line method consists of the organization accruing depreciation evenly (over the years) over the entire standard service life or useful life of the fixed asset. In this case, the annual amount of depreciation charges is determined based on the depreciable cost of the item of fixed assets or intangible assets and the standard service life or useful life of it by multiplying the depreciable cost by the accepted annual linear depreciation rate.

The non-linear method consists in the uneven (over the years) accrual of depreciation by the organization during the useful life of an object of fixed assets or intangible assets. The organization has the right to establish a non-linear method of calculating depreciation in relation to transmission devices; workers, power machines and mechanisms; equipment; computer and office equipment, vehicles and other fixed assets that are directly involved in the production process; instrument; draft animals; intangible assets (except for brand names and trademarks), as well as leasing objects.

The non-linear method of calculating depreciation does not apply to the following types of machinery, equipment and vehicles:

machines, equipment and vehicles with a standard service life of up to 3 years, passenger cars (except for those operated as official vehicles and used for taxi services); - certain types of civil aviation equipment, the useful life of which is determined based on the established resources; - unique equipment and equipment intended for use only for certain types of testing and production of a limited type of specific product; - interior items, including office furniture; - items for recreation, leisure and entertainment.

With the non-linear method, the annual amount of depreciation is calculated using the sum of numbers of years method or the reducing balance method with an acceleration factor of 1 to 2.5 times. The rates of depreciation in the first and each of the subsequent years of the period of application of the non-linear method may be different.

The application of the sum of numbers of years method involves determining the annual amount of depreciation based on the depreciable cost of fixed assets and the ratio, the numerator of which is the number of years remaining until the end of the useful life of the object, and the denominator is the sum of the numbers of years of the useful life of the object.

With the declining balance method, the annual amount of accrued depreciation is calculated based on the under-depreciated cost determined at the beginning of the reporting year (the difference between the depreciable cost and the amount of depreciation accrued before the beginning of the reporting year) and the depreciation rate calculated based on the useful life of the object and the acceleration factor (from 1 to 2 ,5 times) accepted by the organization.

The productive method of calculating depreciation of an object of fixed assets or intangible assets is to charge the organization with depreciation based on the depreciable cost of the object and the ratio of natural indicators of the volume of products produced in the current period to the resource of the object - the expected volume of work or products for the entire period of operation of the object.

The monthly rate (or amount) of depreciation for the linear and non-linear methods of its calculation is 1/12 of its annual rate (or amount) from the month in which depreciation began to be calculated, with the exception of objects whose operation is seasonal.

The different durability of parts causes the need for partial restoration of the machine’s performance during its operation, i.e. need in repairs.

Work aimed at restoring the consumer qualities of the OS is called repair.

In accounting, there are two types of repairs: current and capital. Current repairs mean partial replacement of parts, minor repairs of doors, individual parts, whitewashing of walls and other types of work to maintain the OS in working order. A major overhaul of the operating system is accompanied by a complete disassembly of the units and includes the repair of basic parts and the replacement of all worn-out components and structures.

With the economic method, major repairs of the OS are carried out by the repair shops of the enterprise itself.

All costs for this method of repair are preliminarily collected on account 23 - “Auxiliary production”, and then the actual cost of the certified repair is written off to general production and general business expenses (account 25.26), being an independent item in the estimate of these expenses. In case of a greater deviation of actual production costs from the estimate, the enterprise reserves funds to cover the costs of upcoming repairs (account 96) or temporarily assigns them to account 97 - “Future expenses”

Major repairs of fixed assets are carried out in accordance with annual plans (broken down by quarter), drawn up in monetary terms (at estimated cost) and in physical terms on an object-by-object basis.

Major repairs can be carried out in-house or by contract.

With the contract method, all types of work are performed by a third-party organization in accordance with the contract. Acceptance of completed work is carried out according to the acceptance certificate for repaired, reconstructed and modernized facilities (form No. OS-3). The certificate is accompanied by a certificate from the accounting department about the estimated and actual cost of the repair work performed.

Based on the act, the contractor issues and submits invoices or payment requests to the customer company. In the customer's accounting department, the following entry is made on the accounts:

Dt 25 Kt 60 material material economic residual

At the end of the year in December, the remaining amount of the reserve for current repairs of fixed assets is written off to reduce the general production costs of the corresponding workshop, and the balance amount on account 97 is additionally included in December costs.

Entries are made in statements No. 12 and No. 15.

Rent - provision of property in accordance with an agreement for temporary use for rent. The party providing the property is the lessor. The party receiving it is the tenant. Renting allows the lessor to receive income from temporarily free unused equipment, and the lessee to expand (or start) production with significantly less capital investment.

The procedure for recording an asset lease transaction in accounting depends on the form of the lease. There are 3 forms of lease based on duration: long-term (leasing) - up to 3 years, medium-term (hiring) from 1 to 3 years, short-term (renting) - up to 1 year.

Based on economic conditions, a distinction is made between current and financed leases. Current (production, short-term) is the rental of individual objects for a certain period to satisfy the temporary needs of the tenant. At the end of the rental period, the property is returned. The rights and obligations of the owner remain with the lessor. The tenant has only the right of ownership of the leased property.

A financed lease is the lease of property for a long period of time (long-term). Moreover, the tenant assumes the responsibilities of the owner (responsibility for safety, proper operation). The tenant can buy the leased property.

Individual objects are rented out under current (short-term) lease conditions: residential and industrial premises, individual machines, rental cars. Since the ownership rights remain with the lessor, they remain in accounting on his balance sheet, on 01 (a separate sub-account). The tenant's fixed assets are reflected on the balance sheet, in account 001 provided for this purpose, since fixed assets received for rent do not increase the property owned by the enterprise. The transfer of OS is carried out on the basis of a lease agreement. The tenant does not open inventory cards for the OS accepted for lease. Uses copies of inventory cards or extracts from inventory books received from the lessor. Analytically, accounting in account 001 is carried out by objects, by lessors in the amount of cost specified in the lease agreement.

Depreciation is charged in the usual manner by lessors according to depreciation rates. The amount of accrued depreciation is included in Debit 91, Credit 02.

For a lessee, the calculation of rent replaces the calculation of depreciation. This is a form of reimbursement for OS costs, that is, its amounts are included in the cost of production:

Lt 25.26 Kt 76

Leased fixed assets may be subject to repairs. Repair costs are borne by either the tenant or the landlord, depending on the terms of the lease agreement.

The form of financed (long-term) lease is characterized by the following features: - the lease period is close to the useful life of the leased property; - the amount of rent for the entire lease period characterizes the value of the leased property in current prices at the time of conclusion of the agreement; - ownership passes to the lessee; - during the rental period, the tenant has the right to purchase the leased property. You can think of a financed lease as a form of lending. The amount of rent is equal to the value of the property and the amount of rental interest.

Sometimes leasing companies only pay for objects transferred for long-term lease. The lessee independently receives and installs equipment from the manufacturer and is responsible for its safety, performance, etc.

Intangible assets include property rights owned by the owner to: - objects of industrial property: inventions, utility models, industrial designs, topologies of integrated circuits, production secrets (know-how), selection achievements, brand names, trademarks, etc. - works of science, literature and art that are objects of copyright: literary and scientific articles, monographs, reports, translations, abstracts, reviews, musical arrangements, other adaptations of works of science, literature and art; - computer programs and computer databases; - use of intellectual property arising from license and copyright agreements; - use of natural resources, land; - other: licenses to carry out a type of activity, licenses to carry out foreign trade and quota-based operations, licenses to use the experience of specialists, rights of trust management of property.

Intangible assets do not include: - intellectual and business qualities of the organization’s personnel, their qualifications and ability to work, since they are inseparable from their carriers and cannot be used without them; - scientific research that is not completed and/or not formalized in the manner prescribed by law , experimental design and technological work; - financial instruments of the derivatives market, providing the right to carry out a specific transaction under certain conditions;

organizational expenses (made during the process of privatization and corporatization of an organization, during state registration or re-registration of an organization, and others); - the cost of the organization’s business reputation (goodwill).

Intangible assets are accepted for accounting at their original cost and are reflected in the debit of account 04 in correspondence with the credit of account 08 or settlement accounts.

The initial cost of intangible assets registered with the organization is determined (estimated) in accordance with the actual costs of their acquisition.

Actual costs associated with the acquisition of intangible assets from organizations and individuals under sales contracts are reflected in the debit of account 08 - “Capital investments” in the amounts specified in the primary accounting documents, less value added tax, in correspondence with the loan accounts 60 - “Settlements with suppliers and contractors”, 76 - “Settlements with various debtors and creditors”.

Tutoring

Need help studying a topic?

Our specialists will advise or provide tutoring services on topics that interest you.

Submit your application indicating the topic right now to find out about the possibility of obtaining a consultation.

Fixed assets

Fixed assets are classified as non-current assets of the enterprise. That is, these are the means of the organization that are used by it in its activities for more than one year. This main criterion must be taken into account when classifying the economic assets of an enterprise into the category of fixed assets. In PBU 6/01 "Accounting for fixed assets", approved By order of the Ministry of Finance of the Russian Federation of March 30, 2001 N 26n the criteria for classifying economic assets as fixed assets have been determined. The asset is accepted by the organization to accounting as fixed assets, if the following conditions are simultaneously met:

a) the object is intended for use in the production of products, when performing work or providing services, for the management needs of the organization, or to be provided by the organization for a fee for temporary possession and use or for temporary use;

b) the object is intended to be used for a long time, i.e. a period lasting more than 12 months or the normal operating cycle if it exceeds 12 months;

c) the organization does not intend the subsequent resale of this object;

d) the object is capable of bringing economic benefits (income) to the organization in the future.

Classification of fixed assets:

Production assets include fixed assets who take part in the sphere of material production and serve it. The degree of their participation in the production process is different: some participate in production as tools (machines, equipment, tools), others ensure the uninterrupted production process (transfer devices, structures), others create the necessary conditions for the production process (production buildings), storage or movement of inventory and finished products (warehouses, vehicles, etc.).

Non-productive assets include fixed assets, which do not participate directly or indirectly in the production process, but are intended for the purposes of non-productive consumption, housing and socio-cultural services for workers (fixed assets of housing and communal services, healthcare, culture, etc.).

Depending from a natural material character, i.e. By type, fixed assets are divided into groups:

· land;

· capital costs for land improvement;

· buildings and constructions;

· working and power machines and equipment;

· measuring and control instruments and devices;

· computer and office equipment;

· vehicles;

· tools, production and household equipment;

· working and productive livestock;

· perennial plantings;

· on-farm roads;

· environmental management facilities;

· other fixed assets.

Accounting documents

Upon receipt of fixed assets (fixed assets), fixed assets are accepted for accounting at original cost. Initial cost of fixed assets purchased for a fee, the amount of actual expenses of the organization for the acquisition is recognized, construction and manufacturing, excluding value added tax and other refundable taxes

All operations for capitalization of fixed assets, write-off and other operations are documented.

These include, in particular,

- Certificate (invoice) of acceptance and transfer of fixed assets (form N OS-1);

- Acceptance certificate for repaired, reconstructed and modernized facilities (Form N OS-3);

- Act on write-off of fixed assets (form N OS-4);

- Act on write-off of motor vehicles (form N OS-4a);

- Inventory card for accounting of fixed assets (form N OS-6);

- Certificate of acceptance of equipment (form N OS-14);

- Certificate of acceptance and transfer of equipment for installation (form N OS-15);

- Report on identified equipment defects (Form N OS-16).

+ supplier documents and technical passports of manufacturers for complex technical products.

All operations on capitalization of fixed assets, write-offs and other operations with fixed assets are documented with the above documents. It should be noted that the Law of the Russian Federation “On Accounting” No. 402-FZ dated December 6, 2011 does not regulate the forms of primary accounting documents. Above are the forms used before 01/01/2013, in accordance with the resolution of the State Committee of the Russian Federation on Statistics dated October 30, 1997 N 71a “On approval of unified forms of primary accounting documentation for accounting of labor and its payment, fixed assets and intangible assets, materials of low value and wearable items, work in capital construction", i.e. before the new law comes into force. Therefore, in order to maintain accounting records, it is necessary in the Order “On Accounting Policies for Accounting Purposes” to discuss the use of the above forms or, according to the new law, the use of new ones developed by the enterprise itself,

in this case, banks are designed with mandatory details on them. .

Accounting and postings

Accounting for fixed assets is carried out on account 01 “Fixed Assets”. (Account Active) In this account, fixed assets are accounted for at their original cost.

Upon receipt of the OS, on the basis of the supplier’s documents, entries are made to capitalize the OS on the balance sheet, with the execution of the Acceptance and Transfer Certificate OS-1, namely:

1) Dt 08 Kt 60 Initial cost Operation "Registration of documents of OS suppliers"

2)Dt19-1 Kt 60 VAT supplier Instead of account 60 in accounts N1 and 2, there may be another account, for example, 71 “Settlements with accountable persons”, when purchasing fixed assets for cash.

3) Dt 01 Kt 08 Operation "Commissioning of OS"/at original cost, Price without VAT/.The acceptance certificate is drawn up by the commission and signed by the head of the organization.

During the operation of the fixed asset, the cost of fixed assets is written off to cost in the form of depreciation charges. All fixed assets are legally divided into depreciation groups with different service lives. The Classification of fixed assets included in depreciation groups is used (approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 “On the Classification of fixed assets included in depreciation groups”). During the reporting period year, depreciation charges for fixed assets are accrued monthly regardless of the calculation method used in the amount of 1/12 of the annual amount

The annual amount of depreciation is calculated depending on the method of calculating depreciation chosen by the enterprise in accordance with the Regulations on Accounting Policies for accounting purposes. As a rule, this is a linear method, which is most often used in enterprises and organizations. At linear method the annual amount of depreciation is determined based on the original cost of the fixed asset and the depreciation rate calculated based on the useful life of the fixed asset, according to the depreciation group to which the fixed asset belongs. Except linear method There are other depreciation calculations: reducing balance methodmethod of writing off cost by the sum of numbers of years of useful life,method of writing off cost in proportion to the volume of products (works). Due to the brevity of this course and very rare application, these methods are not considered in this work. Since January 1, 2002, for tax accounting purposes, the Classification of fixed assets has been used, approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 “On the Classification of fixed assets included in depreciation groups”). OS according to this classification are divided into the following groups:

First group- all short-lived property with a useful life from 1 year to 2 years inclusive

Second group- property with a useful life of more than 2 years up to 3 years inclusive

Third group- property with a useful life of more than 3 years up to 5 years inclusive

Fourth group- property with a useful life of over 5 years up to 7 years inclusive

Fifth group- property with a useful life of over 7 years up to 10 years inclusive

Sixth group- property with a useful life of over 10 years up to 15 years inclusive

Seventh group- property with a useful life of over 15 years up to 20 years inclusive

Eighth group- property with a useful life of over 20 years up to 25 years inclusive

Ninth group- property with a useful life of over 25 years up to 30 years inclusive

Tenth group- property with a useful life of over 30 years

Not subject to depreciation:

- land and other natural resources (water, subsoil and other natural resources), as well as inventories, goods, capital construction projects in progress, securities, financial instruments of futures transactions (including forwards, futures contracts, option contracts).

- property of budgetary organizations, with the exception of property acquired in connection with business activities and used to carry out such activities;

- property of non-profit organizations received as earmarked proceeds or acquired at the expense of earmarked proceeds and used for non-commercial activities

- and property acquired (created) using budget funds for targeted financing. This norm does not apply to property received by the taxpayer during privatization

- external improvement facilities (forestry facilities, road facilities, the construction of which was carried out with the involvement of sources of budgetary or other similar targeted funding, specialized navigation facilities) and other similar facilities

- productive livestock, buffaloes, oxen, yaks, deer, other domesticated wild animals (except for draft animals);

The use of one of the methods for calculating depreciation for a group of homogeneous fixed assets is carried out throughout the entire useful life of the objects included in this group. Calculation of depreciation charges for an object of fixed assets begins on the first day of the month following the month in which this object was accepted for accounting, and is carried out until the cost of this object is fully repaid, or this object is written off from accounting. Accrual of depreciation charges stops from the first day of the month following the month of full repayment of the cost of this object, or write-off of this object from accounting. During the useful life of the fixed asset, the accrual of depreciation charges is not suspended, except in cases transferring it, by decision of the head of the organization, to conservation for a period of more than three months, as well as during the period of restoration of the object, the duration of which exceeds 12 months. Accrual of depreciation charges for fixed assets is carried out regardless of the organization’s performance in the reporting period and is reflected in the accounting records of the reporting period to which it relates. Monthly depreciation is calculated using the accounting entry: Dt 20,23,26 Kt 02 "Depreciation of fixed assets". When calculating depreciation of fixed assets, different cost accounts 20, 23 and 26 are debited, depending on the use of fixed assets, namely in the main production (Dt 20), in auxiliary production (Dt 23) or non-production fixed assets or general purpose fixed assets (Dt 26).

During the operation of the OS, the need for their repair arises. In addition to repairs, operating systems can be subject to modernization and reconstruction. Modernization and reconstruction differ from repairs in that they significantly change the consumer properties of the operating system and have a capital nature of costs. For example, reconstruction of a building increases the usable area of the task - the costs are of a capital nature. Whitewashing and painting a building are current costs that do not significantly change the consumer properties of the building. Accordingly, costs for the repair of the operating system and the modernization and reconstruction of the operating system are reflected differently in accounting. All types of OS repairs are included in current costs, and the costs of modernization and reconstruction lead to an increase in the cost of the OS. Accordingly, these operations are taken into account with this economic content, namely with the following entries:

Current OS repair

Executed by contract: Dt 20,23,26 Kt 60 "Settlements with suppliers and contractors" - cost of OS repairs

Dt 19 Kt 60 - VAT is taken into account by the OS repair supplier

Made by the company itself (economic method) Dt 20,23,26 Kt 10,70,69,69 - repair cost expressed as the amount of costs from the credit of the corresponding accounting accounts, according to materials - Kt account 10, for wages - Kt account 70, for personal income tax with salary - Kt account. 68, for deductions to extra-budgetary funds from the salary fund - Kt account 69

Reconstruction and modernization of the OS

Executed by contract: 1) Dt08 Kt 60 “Settlements with suppliers and contractors” - cost of OS repairs

2) Dt19 Kt 60 - VAT of the supplier for reconstruction.OS

3) Dt01 Kt 08 Increase in the cost of fixed assets by the amount of reconstruction and modernization

When reconstructing by contract, in addition to the invoice, it is necessary to draw up a certificate of work performed, an estimate is drawn up in construction, and upon completion, in addition to the certificate of work performed F2-KS, a certificate of the cost of work performed F3-KS is drawn up

Reconstruction and modernization of the OS, carried out by the enterprise itself ( economic method):

- Dt 08 Kt 10,23,70,68,69 material, labor costs and deductions of taxes and contributions to modernization funds

- Dt 01 Kt 08 increase in OS cost by the amount of modernization costs

During the operation of the enterprise fixed assets are retired from economic turnover. Disposal of fixed assets is carried out for various reasons: due to damage and write-off of fixed assets, when selling fixed assets, transferring fixed assets to another legal entity as a contribution to the authorized capital, etc. The disposal of fixed assets is recorded using the following transactions:

1. Write-off and disposal due to OS unsuitability for further use

- The initial cost of the operating system is written off from the balance sheet. Acts for write-off of fixed assets are drawn up in the form OS-4, OS-4a or OS-4b

Dt 91 Kt 01 "Sub-account for disposal of fixed assets"- The residual value is written off from the balance sheet for the financial result of the write-off.

2. Write-off (disposal) in connection with the sale of fixed assets

Dt 01 "Sub-account for disposal of fixed assets" Kt 01- The initial cost of the fixed assets is written off from the balance sheet. Acceptance and transfer certificates of OS-1, forms OS-1a, OS-1b are drawn up.

Dt 02 Kt 01 "Sub-account for disposal of fixed assets"- The depreciation of the fixed assets accrued at the time of disposal during the operation of the fixed assets is written off from the balance sheet

Dt 91 Kt 01 "Sub-account for disposal of fixed assets"- The residual value is written off to the financial result from write-off

Dt62 Kt91_1- Revenue from the sale of fixed assets is reflected at the sales price, an invoice is issued for the sale of fixed assets

Dt 91 Kt68- VAT is charged on the amount of the sale of fixed assets, in accordance with the issued invoice for the sale of fixed assets

3. Write-off (disposal) in connection with the transfer as a contribution to the authorized capital of another legal entity

Dt 01 "Sub-account for disposal of fixed assets" Kt 01- The initial cost of the fixed assets is written off from the balance sheet. Certificates of acceptance and transfer of fixed assets are drawn up, form OS-1

Dt 02 Kt 01 "Sub-account for disposal of fixed assets"- The depreciation of the fixed assets accrued at the time of disposal during the operation of the fixed assets is written off from the balance sheet

Dt 58 Kt 01 "Sub-account for disposal of fixed assets"- Transfer of fixed assets as a contribution to the authorized capital.

Fixed assets are part of the organization’s property used as means of labor in the production of products, performance of work or provision of services, as well as for management for a period exceeding 12 months, or the normal operating cycle, if it exceeds 12 months.

In accounting, fixed assets worth no more than 40,000 rubles can be taken into account as part of inventories. From January 1, 2016, the limit on the value of fixed assets in tax accounting increased from 40,000 to 100,000 rubles. Fixed assets put into operation from January 1, 2016 are taken into account taking into account the new limit of 100,000 rubles (Federal Law of June 8, 2015 No. 150-FZ).

The unit of accounting for fixed assets is an inventory object:

- a separate item (for example, a safe);

- a single complex of several items that are mounted on a single foundation and have common control (for example, a computer, which includes a system unit, monitor, keyboard, mouse).

You must charge depreciation on fixed assets. How to proceed, see account 02 “Depreciation of fixed assets”.

Acquisition and commissioning of fixed assets

If your organization acquired fixed assets, then you must record them on the balance sheet at their original cost. The initial cost is the amount of actual costs for the acquisition of an item of fixed assets.

Reflect the capitalization of an item of fixed assets in the debit of account 08 “Investments in non-current assets”:

DEBIT 08 CREDIT 60 (75-1, 76, 98-2, …)

– an item of fixed assets has been capitalized.

DEBIT 01 CREDIT 08

Purchase of fixed assets

If your organization purchased fixed assets for a fee (under a purchase and sale or supply agreement), determine their initial cost as the sum of all costs associated with this purchase.

Such costs, for example, could be:

- amounts paid to the seller in accordance with the agreement;

- amounts paid for delivery and installation;

- amounts paid for information and consulting services related to the acquisition of this fixed asset;

- customs duties and fees;

- non-refundable taxes, state duties paid in connection with the acquisition of fixed assets;

- interest on loans and borrowings received for the acquisition of fixed assets, if it is an investment asset;

- other costs directly related to the acquisition of fixed assets.

You must first take into account the costs of acquiring fixed assets in the debit of account 08 “Investments in non-current assets” (without value added tax):

DEBIT 08 CREDIT 60 (76, …)

– costs directly related to the acquisition of fixed assets are taken into account (excluding VAT);

then, based on the invoices, reflect the amount of value added tax:

DEBIT 19 CREDIT 60 (76, …)

– VAT is taken into account on costs directly related to the acquisition of fixed assets.

After the fixed asset item is put into operation, make an entry to the debit of account 01:

DEBIT 01 CREDIT 08

– a fixed asset facility was put into operation.

Then report the value added tax deduction:

– a tax deduction has been made.

There are situations when a property requires state registration, but is already in use.

Until 2011, such objects could be accounted for in two ways: on account 08 “Investments in non-current assets” or on a separate sub-account opened to account 01 “Fixed Assets”.

Starting from 2011, temporarily operated real estate should be accounted for as part of fixed assets (with allocation in a separate sub-account).

The fact of submitting documents for state registration does not matter (clause 52 of the Guidelines for accounting of fixed assets, approved by order No. 91n dated October 13, 2003).

Depreciation on such fixed assets must be calculated in the usual manner: from the 1st day of the month following the month the property was accepted for accounting (letter of the Federal Tax Service of the Russian Federation dated August 29, 2011 No. ZN-4-11/13999@).

The fact of filing documents for state registration of ownership for the calculation of depreciation does not matter.

JSC Aktiv acquired a warehouse building under a sale and purchase agreement. According to the agreement, the cost of the warehouse is 1,180,000 rubles. (including VAT - 180,000 rubles). 15,000 rubles were paid for state registration of the building.

DEBIT 60 CREDIT 51

– 1,180,000 rub. – the seller’s invoice has been paid;

DEBIT 08 CREDIT 60

– 1,000,000 rub. – the building is capitalized on the organization’s balance sheet (excluding VAT);

DEBIT 19 CREDIT 60

– 180,000 rub. – the amount of VAT according to the seller’s invoice is taken into account;

DEBIT 01 subaccount “Fixed assets that are subject to state registration” CREDIT 08

– 1,000,000 rub. – the building is accounted for in a separate subaccount;

DEBIT 68 subaccount “VAT Calculations” CREDIT 19

– 180,000 rub. – tax deduction has been made.

After the building is ready for commissioning, the Aktiva accountant must make the following entries:

DEBIT 01 CREDIT 01 subaccount “Fixed assets that are subject to state registration”

– 1,000,000 rub. – the building is included in fixed assets.

Since now state registration takes place after the property is accepted for registration, it is impossible to take into account the costs of paying state duty in its original cost.

The amount of costs for paying the state duty must be taken into account as part of current expenses:

DEBIT 76 CREDIT 51

– 15,000 rub. – money was transferred to pay for state registration of ownership of the building;

DEBIT 26 CREDIT 68 subaccount “State Duty”

– 15,000 rub. – the amount of state duty for registering ownership of the building is taken into account.

If you use real estate objects that are reflected in your account 08 (not transferred to fixed assets in time) for the production of products, provision of services or for management needs, then property tax must be charged on such objects (Definition of the Supreme Arbitration Court of the Russian Federation dated 25 March 2013 No. BAS-3043/13).

Let us recall that in accordance with paragraph 6 of PBU 6/01, the accounting unit of fixed assets is an inventory item. An inventory item of fixed assets is an object with all its fixtures and accessories, or a separate structurally isolated item intended to perform certain independent functions, or a separate complex of structurally articulated items that constitute a single whole and are intended to perform a specific job. A complex of structurally articulated objects is one or more objects of the same or different purposes, having common devices and accessories, common control, mounted on the same foundation, as a result of which each object included in the complex can perform its functions only as part of the complex, and not independently.

Let's consider how a company can record the purchase of a personal computer in its accounting.

JSC Aktiv purchased a personal computer under a purchase and sale agreement. The invoice indicated the cost of the computer components:

- system unit – RUB 33,040. (including VAT – 5040 rub.);

- monitor – 13,570 rub. (including VAT – 2070 rub.);

- keyboard – 1180 rub. (including VAT - 180 rubles);

- mouse – 590 rub. (including VAT - 90 rubles).

Total: the cost of the computer is 48,380 rubles. (including VAT - 7380 rubles).

The components of a computer (system unit, monitor, keyboard, mouse) can only function as part of a single complex, so the Aktiva accountant accepted them for accounting as a single inventory object and made the following entries:

DEBIT 60 CREDIT 51

– 48,380 rub. – the seller’s invoice has been paid;

DEBIT 08 CREDIT 60

– 41,000 rub. (48 380 – 7380) – the computer was capitalized on the organization’s balance sheet (at the cost of its components excluding VAT);

DEBIT 19 CREDIT 60

– 7380 rub. – the amount of VAT according to the seller’s invoice is taken into account.

“Aktiv” additionally paid for the delivery of the computer (236 rubles, including VAT – 36 rubles) in cash from the cash register through an accountable person:

DEBIT 71 CREDIT 50

– 236 rub. – money was given from the cash register to the accountable person to pay for the delivery of the computer; v

DEBIT 08 CREDIT 71

– 200 rub. (236 – 36) – the delivery fee is taken into account in the book value of the computer (based on the advance report of the accountable person);

DEBIT 19 CREDIT 71

– 36 rub. – VAT is taken into account on delivery costs (based on the invoice of the transport organization).

When the computer was put into operation, the Aktiva accountant made the following entries:

DEBIT 01 CREDIT 08

– 41,200 rub. (41,000 + 200) – the computer is included in the organization’s fixed assets;

DEBIT 68 subaccount “VAT Calculations” CREDIT 19

– 7416 rub. (7380 + 36) – tax deduction has been made.

In exchange for goods, Aktiv receives a laptop from Passive LLC.

DEBIT 45 CREDIT 41

– 35,000 rub. – the cost of goods shipped under a goods exchange agreement is written off;

DEBIT 08 CREDIT 60

– 43,000 rub. – a laptop received under a commodity exchange agreement was capitalized.

After this, the Aktiva accountant must reflect the proceeds from the sale of the goods and write off its cost. For the procedure for recording these transactions, see standard situations “How to reflect revenue under a commodity exchange (barter) agreement” to account 90 “Sales”.

If the market price of the transferred property cannot be determined, then determine the value of the received fixed assets based on the prices at which the organization acquires similar fixed assets.

Fixed assets must be constantly maintained in working order, which requires certain costs.

Maintenance costs (technical inspection, maintenance, etc.) and all types of repairs (current, medium, capital) of fixed assets include the cost of production:

DEBIT 20 (23, 25, 26, 29, 44, …) CREDIT 10 (60, 69, 70, …)

– reflect the costs of maintenance and repair of fixed assets.

Expenses for all types of repairs are taken into account when taxing profits in the amount of actual costs. These expenses include the cost of production in the reporting period in which they arose (Article 260 of the Tax Code of the Russian Federation).

JSC Aktiv carried out routine repairs of the machine. Repair costs amounted to:

- workers' wages - 1000 rubles;

- contributions to the Pension Fund, Social Insurance Fund, Federal Compulsory Medical Insurance Fund and insurance against industrial accidents and occupational diseases accrued from workers’ salaries – 302 rubles;

- cost of purchased parts - 1416 rubles, including VAT - 216 rubles.

The Aktiva accountant made the following entries:

DEBIT 20 CREDIT 70

– 1000 rub. – the wages of the workers who carried out the repairs were written off as cost;

DEBIT 20 CREDIT 69-1, 69-2, 69-3

– 302 rub. – contributions to the Pension Fund, Social Insurance Fund, Federal Compulsory Medical Insurance Fund and contributions for “injury” are written off as cost;

DEBIT 71 CREDIT 50

– 1416 rub. – money was issued from the cash register to the accountable person to pay for the details;

DEBIT 10 CREDIT 71

– 1200 rub. (1416 – 216) – parts purchased for repairing the machine were capitalized;

DEBIT 19 CREDIT 71

– 216 rub. – VAT included;

DEBIT 68 subaccount “VAT Calculations” CREDIT 19

– 216 rub. – VAT is accepted for deduction;

DEBIT 20 CREDIT 10

– 1200 rub. – parts used to repair the machine are written off as cost.

A total of 2,502 rubles were written off for the cost of repairs. (1000 + 302 + 1200). This amount can be fully taken into account when taxing profits.

The initial cost of repaired fixed assets is not subject to change.

If you decide to revaluate fixed assets, then in the future you will need to do this every year.

Revaluation is carried out by indexation or direct recalculation based on documented market prices.

In this case, the following can be used (clause 43 of the Guidelines for accounting of fixed assets):

- data on similar products received from manufacturing organizations;

- information on price levels available from state statistics bodies, trade inspectorates and organizations;

- information on price levels published in the media and specialized literature;

- technical inventory bureau assessment;

- expert opinions on the current (replacement) cost of fixed assets.

However, for property tax purposes, the results of revaluation are taken into account.

The results of the revaluation are taken into account either in account 83 “Additional capital” or are included in financial results.

note

In tax accounting, the value of fixed assets is formed without taking into account revaluation. Depreciation is accrued in the same order and in the same amounts as before the revaluation of fixed assets (Article 257 of the Tax Code of the Russian Federation).

Disposal of fixed assets

If your organization has sold, liquidated, or transferred a fixed asset to another company, you must write off its value from the organization's balance sheet.

As you know, fixed assets are listed on the balance sheet at their residual value, which is determined as follows:

When writing off a fixed asset from the balance sheet, first write off the amount of accrued depreciation.

To do this, make the wiring:

DEBIT 02 CREDIT 01

– the amount of accrued depreciation of a fixed asset item is written off.

Thus, on the debit of account 01 the residual value of the disposed fixed asset item will be formed. You must debit this amount to account 91 “Other income and expenses”:

DEBIT 91-2 CREDIT 01

– the residual value of the fixed asset is written off.

To account for the disposal of fixed assets, you can open a separate subaccount “Retirement of fixed assets” for account 01.

If your organization decides to use the “Retirement of fixed assets” subaccount, when writing off a fixed asset item from the balance sheet, you must make the following entries:

DEBIT 01 subaccount “Retirement of fixed assets” CREDIT 01

– the original cost of the fixed asset item has been written off;

– the residual value of the fixed asset item is written off.

If an item of fixed assets is disposed of, the value of which was increased as a result of revaluation, then the amount of its revaluation, listed in account 83 “Additional capital”, is included in retained earnings:

DEBIT 83 CREDIT 84

– the amount of revaluation of the disposed fixed asset item is included in retained earnings.

If you account for property worth no more than 40,000 rubles as part of fixed assets, then depreciation on it is calculated in the usual manner.

In February, Aktiv JSC purchased a pneumatic motor worth RUB 17,700. (including VAT - 2700 rubles). Its useful life is 3 years. In accordance with the accounting policy of JSC Aktiv, property worth more than 10,000 rubles. taken into account as part of fixed assets. The pneumatic motor was put into operation in February.

The Aktiva accountant must make the following entries:

in February

DEBIT 08 CREDIT 60

– 15,000 rub. (17,700 – 2700) – the debt to the supplier is reflected;

DEBIT 19 CREDIT 60

– 2700 rub. – VAT included;

DEBIT 01 CREDIT 08

– 15,000 rub. – the pneumatic motor is put into operation;

DEBIT 68 subaccount “VAT Calculations” CREDIT 19

– 2700 rub. – accepted for VAT deduction;

in March

DEBIT 26 CREDIT 02

– 417 rub. (RUB 15,000: 3 years: 12 months) – depreciation has been calculated.

Sale of fixed assets

If your organization decides to sell a fixed asset, make the following entries:

DEBIT 62 (76) CREDIT 91-1

– income from the sale of fixed assets and the buyer’s debt are reflected;

DEBIT 51 (50, …) CREDIT 62 (76)

– funds have been received from the buyer;

DEBIT 91-2 CREDIT 68 subaccount “VAT calculations”

– VAT is charged;

DEBIT 01 subaccount “Retirement of fixed assets” CREDIT 01

– the original cost of fixed assets has been written off;

DEBIT 02 CREDIT 01 subaccount “Retirement of fixed assets”

– the amount of accrued depreciation is written off;

DEBIT 91-2 CREDIT 01 subaccount “Retirement of fixed assets”

– the residual value of fixed assets is written off;

– expenses related to the sale of fixed assets are written off (for example, expenses for dismantling equipment, dismantling a building, etc.).