Applications for clarification of the tax period. How to write a letter to the tax office about payment clarification

A letter to clarify the purpose of payment is drawn up when employees of organizations discover an error or inaccuracy in an already executed payment order. This letter is not just part of business correspondence, it refers to the primary documentation of the company.

FILES

When and what errors occur

Errors in payments between counterparties are made by the compilers, i.e. employees of accounting departments. In this case, incorrect data can be in a variety of points in the document: for example, the number of the agreement under which funds are transferred is incorrectly indicated, the purpose of the payment is incorrectly written, or, sometimes, VAT is allocated where it is not necessary, etc.

This can be corrected unilaterally by sending a letter to the partner to clarify the purpose of the payment.

In this case, the other party is not obliged to send a notification of receipt of this message, but it will not be superfluous to make sure that the letter has been received.

Is it possible to challenge a new payment assignment?

Typically, changing the “Payment purpose” parameter occurs by mutual agreement and without any special consequences. But in some cases complications are possible. For example, if the tax inspectorate during an audit discovers such a correction and considers it a way to evade taxes, sanctions from the regulatory authority can be considered inevitable. It happens that friction regarding the purpose of payment arises between counterparties, especially in terms of payments on debts and interest. In most cases, in order to challenge the correction, the party protesting it will have to go to court, and no one will give guarantees of winning the case, since such stories always have many nuances.

An important condition necessary in order to avoid possible problems is that information about changes in the purpose of the payment must be transmitted to the banks through which the payment was made. To do this, you just need to write similar letters in a simple notification form.

Who writes a letter to clarify the purpose of payment?

This letter is drawn up by the company that transferred the funds.

Usually the text itself is written by a specialist in the accounting department or another employee authorized to create this type of correspondence and who has access to the generated payments.

In this case, the document must be signed by the head of the company.

How to write a letter correctly

A letter to clarify the purpose of payment does not have a unified template that is mandatory for use; accordingly, it can be written in any form or according to a template approved in the company’s accounting policy. At the same time, there is a number of information that must be indicated in it. This:

- name of the sending company,

- his legal address,

- information about the addressee: company name and position, full name of the manager.

- a link to the payment order in which the error was made (its number and date of preparation),

- the essence of the admitted inaccuracy

- corrected version.

If there is several incorrectly entered information, then they must be entered in separate paragraphs.

All amounts must be entered on the form in both numbers and words.

When writing a letter, it is important to adhere to a business style. This means that the wording of the message should be extremely clear and correct, and the content should be quite brief - strictly to the point.

How to format a letter

The law makes absolutely no requirements for both the informational part of the letter and its design, so you can write it on a simple blank sheet or on the organization’s letterhead, and both printed and handwritten versions are acceptable.

The only rule that must be strictly followed: the letter must be signed by the director of the company or a person authorized to endorse such documentation.

It is not necessary to stamp the message, since since 2016 legal entities have been exempted by law from the need to do this (provided that this requirement is not specified in the company’s internal regulations).

The letter must be written as a minimum in four copies:

- you should keep one for yourself,

- transfer the second to the counterparty,

- the third to the payer's bank,

- the fourth to the recipient's bank.

All copies must be identical and properly certified.

How to send a letter

There are several ways to send such a letter.

- personally from hand to hand,

- courier delivery,

- via Russian Post by registered mail with acknowledgment of delivery,

- through the Internet.

When sending via the Internet, it is important that the company has an officially registered electronic digital signature, although even this does not guarantee that the recipient will read the letter.

How and for how long to store a letter

After sending, all letters about clarification of the purpose of payment must be registered in the journal of outgoing documentation, and one copy must be placed in the folder of the current “primary” company. Here it should be for the period established for such documents by law or internal regulations of the company, but at least three years. After losing its relevance and expiration of the storage period, the letter can be transferred to the archive of the enterprise or disposed of in the manner prescribed by law.

Most errors in payments can be clarified by submitting an application for payment clarification. For example, TIN, KPP, OKTMO. But there are two fields in which information cannot be clarified. What to do in these cases and how to fill out an application for clarification of payment in 2019 - read in this article.

Attention! The following documents will help you process payments without errors:

It is convenient to work with documents in . It is suitable for organizations and individual entrepreneurs. The program will automatically generate and print all the necessary primary data. It also includes uploading transactions to 1C, automatic generation of any reporting, and much more.

What errors in a payment order can be corrected by clarifying the payment?

Errors in instructions can be corrected, although not all of them. In the table we will show which data can be clarified and which cannot.

Table. What errors in the payment can be clarified

Just two errors in a document cannot be corrected. This is an incorrect Treasury number and the name of the recipient's bank. Therefore, the company will have to re-introduce the payment to the budget and return the erroneous transfer upon application.

If mistakes were made in the recipient’s KBK, INN or KPP, the tax authorities will first send a notification to the Treasury. And based on the results of the department’s response, they will inform the company about the results of the clarifications. In total, they are given 10 working days for this.

Most often, errors occur in the KBK. And this is quite understandable. After all, even a typo in one number is already an unreliable detail. For example, instead of KBK for contributions, they wrote down for personal income tax - 182 1 01 02010 01 1000 110 . Then that’s right, enter the code - 182 1 02 02010 06 1000 160 .

Companies also make mistakes in the TIN/KPP of the payer and recipient of money, status in field 101, purpose of payment, etc. These shortcomings can be corrected, the Federal Tax Service and the Pension Fund reported this in a joint letter dated 06.06.2017 No. 3N-4-22/10626a/ NP-30-26/8158.

Payment clarification in 2019: sample

Due to an error in the payment slip, the payment falls into the “unclarified” category, which means that there will be an arrears on the card and penalties will be charged. If the error can be corrected, submit a payment clarification request as soon as possible. The algorithm is as follows.

Step 1. Complete an application for payment clarification. There is no official form for the document, so you can compose it arbitrarily. In the header, write down the company details: name, INN, OGRN, address and telephone number so that inspectors can contact you. Next, on the right edge of the letter, indicate the details of the inspection where you are submitting your application. In this case, it is enough to write down: name and full name. head of the Federal Tax Service.

Place the title of the document in the center. For example, “Application for clarification of payment.” And only then, below in the text, explain in detail what exactly the company did wrong and how the details will be recorded correctly.

Step 2. Submit an application to the inspectorate. You can do this in several ways:

– submit the document in person to the Federal Tax Service;

– send the document by courier;

– by registered mail with acknowledgment of delivery;

- through the Internet.

The company can choose any method of sending a letter; there are no restrictions in the code. The only thing is that when sending a document via the Internet, sign it with an electronic digital signature. Then the file will be considered reliable.

The company must record all outgoing letters in a journal; an application for clarification of payment is no exception. Therefore, assign a serial number and date to the document when you send the document to the inspectors. Then reflect the details in the journal.

Step 3. Check the budget settlement card . Inspectors must respond to the application within 5 working days. Moreover, if their decision is positive, then they will reverse the penalty on the date when you actually sent the payment (clause 7 of Article 45 of the Tax Code of the Russian Federation). But if controllers have questions, they will ask for reconciliation of calculations and additional explanations. Therefore, the procedure for clarifying payment may take a long time.

The company can order a reconciliation at any time. To do this, submit an arbitrary application to the Federal Tax Service with a request to provide a certificate of settlements with the budget. You can submit your application on paper, but it’s faster to do it through an ED operator or your personal account on the Federal Tax Service website.

How to fill out a payment order in accounting programs

Instructions - how to fill out a payment form in Bukhsoft Online, 1C: Enterprise and Kontur.Accounting.

Bukhsoft Online

1. Go to the “Accounting” module and select the “Service/Our Accounts” section. Click "Change" and enter your bank details. After that, click the “Basic” button.

2. In order for the payment order to reflect the details of the recipient’s bank, you need to add a bank in the directory of counterparties, in the “Current Accounts” tab, then place the cursor on the line with the bank and click the “Main” button.

3. In the “Accounting” section, go to “Bank”. In the selection window, select the bank where you are sending the payment. Select a period and click Add. Fill out the form that opens. Save.

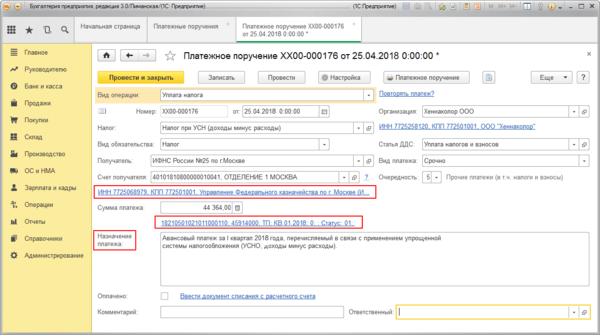

1C:Enterprise

1. Go to the menu: Bank and cash desk/Bank/Payment orders.

2. Click “Create”, select the type of transaction “Tax payment”.

3. Fill in all the necessary details using the hyperlinks in the “Payment Order” document.

4. Save the document using the “Save” button.

5. To output the document in printed format, click “Payment order”.

Kontur.Accounting

1. Start creating payment documents from the “Requirements” page. P Follow the “Pay” link.

2. Enter your bank details and payment amount. The payment amount can be corrected. You can specify the type of payment, and the remaining data is distributed automatically in the appropriate fields of payment documents. In addition to the standard payment order, you will be able to generate receipts for which you will transfer money to the Bank of Russia during a personal visit.

3. The finished tax payment slip can be saved in word format, and then printed and paid at the bank. You can also generate a special text file and upload it to your online bank.

A payment order is a payment document that has a unified form (0401060). Appendix No. 2 to the order of the Ministry of Finance of the Russian Federation dated November 12, 2013 No. 107n approved the rules for filling out the form. It is especially important to fill out the payment form correctly when transferring taxes and contributions. If an error was nevertheless made, then in a number of cases the taxpayer has the right to submit to the tax office an application to clarify the payment (clause 7 of Article 45 of the Tax Code of the Russian Federation).

Why is it not always possible to get by with a clarifying letter to the Federal Tax Service? The legislator gives the payer this opportunity only in cases where, despite a typo, the payment was received in the budget system of the Russian Federation to the appropriate account of the Federal Treasury. It turns out that if the recipient’s bank and the Federal Treasury account number are indicated correctly, and the typo is contained in other fields of the payment order, then it is quite possible to correct the erroneous data using an application to the tax office to clarify the payment.

Thus, the most dangerous details are:

- name of the recipient's bank;

- Russian Treasury account number.

IMPORTANT! Errors in them cannot be corrected.

Features of submitting an application to the tax office for clarification of payment

We list the key nuances of filing an application for clarification:

- For each incorrect payment order, a separate application is drawn up, but in duplicate.

- The sooner the organization corrects the inaccuracy in the payment, the less likely it is for further disputes with the tax authorities.

- The deadline for the tax inspectorate to make a decision on an application for clarification cannot be found in the Tax Code. In practice, tax authorities make a decision to clarify the payment within 5-10 days after receiving the application, and inform the taxpayer about this within 5 days.

- The taxpayer can submit an application directly to the Federal Tax Service. In this case, the second copy is given to the applicant with the tax stamp. It is also possible to send a letter by mail or through an electronic reporting operator.

We have selected excellent electronic reporting services for you!

Don't know your rights?

What does an application for clarification of payment look like (sample)

You will have to clarify the payment in any form, since there is no regulated one. But, according to paragraph 7 of Art. 45 of the Tax Code of the Russian Federation, it is required to attach a correctable payment order, duly certified by the bank.

An application for clarification of payment to the Federal Tax Service usually has a structure dictated by the rules of document management.

Basic instructions:

- The header contains information about the applicant company and the tax office to which the application is being submitted.

- The title of the letter follows. Wording may vary. For example, “application for clarification of tax payment.”

- In accordance with the organization's standards, the date and originating document number are given.

- The body of the letter contains information about the error (in which payment order what typos were made), as well as a request to clarify the payment and consider the new payment order details correct.

- The head puts a signature, which is certified by the seal of the organization (if any).

You can download a sample application for clarification of payment to the tax office using the link below:

If an organization made a non-critical error in a payment document and the obligation to pay tax was fulfilled, then an application to the tax office to clarify the payment will help correct the situation. The application is drawn up in free form. You can use the sample presented in this article.

Application for clarification of payment order details for the transfer of payments to the budget

Some errors in the tax payment form, due to which the payments were “unclarified,” will be clarified by the inspectorate if the company writes a corresponding statement. First of all, we mean errors in the KBK, TIN, KPP or name of the organization, taxpayer status. According to the company, tax officials must not only clarify payments, but also remove penalties accrued on the debt arising due to the overlay (clause 7 of Article 45 of the Tax Code).

True, it will be possible to clarify the KBK without problems only if the erroneous and correct codes relate to the same tax (clause 2 of section V of the Recommendations on the procedure for maintaining the database “Accounts with the budget” in the tax authorities, approved by order of the Federal Tax Service of Russia dated March 16, 2007 MM -3-10/138@). Otherwise, you will have to transfer the tax again using the correct code, and then ask the tax office for a refund and pay late fees.

Although the Tax Code does not establish such a restriction, it will most likely be necessary to prove the illegality of penalties if the payment slip names the BCC of another tax. Please note that tax authorities access the information reflected in the payment purpose only if a non-existent code is indicated in field 104.

It will be possible to clarify OKATO without any problems if the payment was transferred to the federal or regional budget and did not participate in the formation of local budget revenues. If the tax has already been credited to the “erroneous” local budget, then the error can be corrected by transferring the tax and penalties using the correct details. In this case, the overpayment is returned to the current account. Another option for clarification and the illegality of accruing penalties will again have to be defended in court.

An error in such details as the tax period, grounds or type of payment can also be corrected by writing a statement to the inspectorate to clarify the payment. But in this situation, payments will still be credited to the budget and reflected in the budget settlement card, so this error may not be corrected.

It must be said that now in some regions tax authorities independently clarify most of the payments that fall into the category of unclear. Of course, we mean situations where, from other payment details, one can judge the true identity of the payment. For example, the company indicated a non-existent budget classification code, but the payment purpose correctly indicated the transferred tax. Moreover, no penalties will be charged in this case. The fact is that after clarification such

the amounts are included in the settlement card with the budget on the date indicated in the payment order.

If the Federal Treasury account number and the name of the recipient's bank are written incorrectly, then the penalties will not be reset. In this case, the amount will not be credited to the budget, which means that the obligation to pay tax is considered unfulfilled (subclause 4, clause 4, article 45 of the Tax Code of the Russian Federation). In such a situation, you will have to write an application for a tax refund and submit it to your tax office. Moreover, this also applies to cases where the tax was credited to the account of the Federal Treasury of another constituent entity of the Russian Federation.

You can create a document in any form. It must indicate the specific error that was made in the payment order and its details. In addition, you must provide the correct information necessary to reflect the amount in the budget settlement card.

Documents confirming payment of tax to the budget should be attached to the application. You can print out an electronic copy from the Client-Bank system and certify it with the signature of the general director and the company seal. True, some inspections require it. so that the payment order bears a bank mark. In addition, for particularly demanding inspectors, an extract from the current account can be attached to the application, from which it can be seen that the money has been debited from the company’s current account.

If, as a result of an error, the payment was untimely reflected in the budget settlement card, then the application also asks to recalculate the penalties.

The application is sent as needed - when an error is discovered. There are no specific deadlines for this.

Download the application to clarify the details of the payment order for the transfer of payments to the budget &rarr

Invalid KBK: how to fix the error

When filling out payment orders for the transfer of insurance premiums to the Pension Fund, accountants often make mistakes. As practice shows, the most common among them are errors in the KBK. Read what these shortcomings lead to and how to correct them in the article prepared by our colleagues from Salary magazine.

From January 1, 2012, payment orders for the transfer of insurance contributions to the Pension Fund must contain the KBK, which are given in Appendix No. 1 to the Federal Law of November 30, 2011 No. 373-FZ On the budget of the Pension Fund of the Russian Federation for 2012 and for the planning period 2013 and 2014

In field 104 of the payment order, payers of insurance premiums indicate one of the following BCCs:

392 1 02 02010 06 1000 160 - when transferring insurance contributions to compulsory pension insurance, credited to the Pension Fund for payment of the insurance part of the labor pension

392 1 02 02020 06 1000 160 - when transferring insurance contributions to compulsory pension insurance, credited to the Pension Fund for the payment of the funded part of the labor pension.

KBK is incorrect, but the payment was received by the Pension Fund

Let's consider a situation where the payer, instead of the BCC of the insurance part of the labor pension, indicated the BCC of the funded part.

Consequences of an error

Since insurance premiums for the insurance and funded parts of the pension are transferred to the same account of the territorial administration of the Federal Treasury, opened for the PFR branch, the funds will be transferred in full to the PFR account.

The fact that the KBK was incorrectly indicated in this case will not be the basis for recognizing the obligation to pay insurance premiums as unfulfilled (Clause 4, Part 6, Article 18 of Federal Law No. 212-FZ of July 24, 2009, hereinafter referred to as Law No. 212-FZ). The judges drew attention to this in the decision of the Federal Antimonopoly Service of the Volga District dated 08/09/2011 in case No. A57-12787/2010 and in the Ruling of the Supreme Arbitration Court of the Russian Federation dated 02/09/2012 No. VAS-368/12 in case No. A14-11622/2010.

Since the payment was received by the extra-budgetary fund to the appropriate account, penalties are not accrued, since the condition for their accrual is the late payment of insurance premiums (Article 25 of Law No. 212-FZ). This was indicated by the judges in the decision of the Federal Antimonopoly Service of the Central District dated January 24, 2012 in case No. A14-1357/2011.

The procedure for clarifying the type and nature of payment

Let's consider the procedure for clarifying the payment, the actions of the policyholder and the Pension Fund branch.

Policyholder's application. The policyholder can submit an application to the Pension Fund of Russia office to clarify the payment due to an error, attaching documents confirming his payment of insurance premiums. This is stated in paragraph 8 of Article 18 of Law No. 212-FZ. The recommended application form is given in the letter of the Pension Fund dated 04/06/2011 No. TM-30-25/3445. See below for a sample of how to fill it out.

Reconciliation of payment of insurance premiums. Based on the application of the policyholder, the Pension Fund of the Russian Federation, as the administrator of budget revenues, may invite him to conduct a joint reconciliation of paid insurance premiums. Its results will be documented in an act signed by the payer of insurance premiums and an authorized official of the Pension Fund of Russia branch (Part 9 of Article 18 of Law No. 212-FZ).

Documents for transfer. The Pension Fund branch may also require from the bank a copy of the payer’s payment order for the transfer of insurance premiums. The bank is obliged to submit it within five days from the date of receipt of the request (Part 10, Article 18 of Law No. 212-FZ).

Notification of clarification of the type and nature of the payment. Based on the documents listed above, the PFR branch issues a notification to clarify the type and nature of the payment on the day of actual payment of insurance premiums.

Within five days after the decision is made to clarify the type and nature of the payment, the PFR branch must notify the payer of insurance premiums (Part 11, Article 18 of Law No. 212-FZ) and the Federal Treasury (Clause 2, Article 160.1 of the Budget Code).

To do this, the Pension Fund uses the generally accepted form given in Appendix No. 8 to the Procedure for cash services for the execution of the federal budget and the procedure for the implementation by territorial bodies of the Federal Treasury of certain functions of financial bodies. approved by order of the Treasury of the Russian Federation dated October 10, 2008 No. 8n.

If the error is reflected in the report

A situation is possible when an error is made towards the end of the reporting period, and the attribution of the payment is clarified after its end.

Before it becomes known that the erroneous payment has been clarified, in lines 111-113 of section 1 of the RSV-1 Pension Fund form, the policyholder must reflect the amounts of insurance premiums paid for the insurance and funded parts of the labor pension in the actual breakdown in accordance with the details of the erroneous payment orders.

After clarification of the incorrect payment (the PFR will notify the policyholder about this), the policyholder will have to submit the updated PFR form RSV-1. It must be submitted, since the date of clarification of the incorrect payment received to the PFR account is considered the date of debiting funds from the policyholder’s current account, that is, the date of the error in the ended period for which the PFR RSV-1 report was submitted, containing an erroneous distribution of paid insurance premiums and an erroneous distribution of their balances at the end of the reporting period.

In the updated form, the payer must show the correct distribution of paid contributions and balances thereon.

KBK is incorrect, payment was not received by the Pension Fund

Another situation is that the policyholder mistakenly indicated in the payment order the KBK, the payment administrator for which is another government agency, for example the Federal Tax Service.

In this case, the amount of insurance premiums will not go to the Pension Fund budget. The obligation to pay insurance premiums will not be considered fulfilled (clause 4, part 6, article 18 of Law No. 212-FZ).

Theoretically, there are two ways to correct the situation. The first is to clarify the payment by writing an application to the Federal Tax Service of Russia and the Pension Fund of Russia. The second is to pay insurance premiums to the correct KBK, and then return the erroneous payment from the Federal Tax Service of Russia. Let's take a closer look at them.

Payment clarification

How to clarify a payment made to an incorrect KBK was explained by the Russian Ministry of Finance in letter dated 03/04/2011 No. 03-02-07/1-64.

Financiers examined a situation where an organization mistakenly transferred the amounts of insurance premiums for compulsory insurance to the tax authority's cash register office instead of the cash register office of the territorial branch of the Pension Fund of Russia.

Policyholder statements. In order to return the funds, the organization must apply for clarification of the erroneously transferred amount of insurance contributions to the Federal Tax Service and the territorial branch of the Pension Fund. We have provided a sample application for clarification of payment to the Pension Fund above. The application to the inspection is written in any form. A sample of its composition is given below.

Actions of the Federal Tax Service. After receiving the payer’s application, the tax authority will send a notification to the Federal Treasury to clarify the type and nature of the payment, as well as that it is not the administrator of the specified amount of insurance premiums.

Treasury actions. Upon receipt of such a notification, the Federal Treasury will take into account the specified payment according to the budget classification code Unidentified receipts credited to the federal budget (clause 47 of the Procedure for accounting by the Federal Treasury of receipts into the budget system of the Russian Federation and their distribution between the budgets of the budget system of the Russian Federation, approved by order of the Ministry of Finance of Russia dated September 5, 2008 No. 92n. further - Procedure for accounting for receipts).

Actions of the Pension Fund. In turn, the Pension Fund, as the income administrator, will send a notification to the Federal Treasury to clarify the type and nature of the payment for uncleared revenues credited to the federal budget.

Based on this notification, the Federal Treasury will reflect the specified receipts on the personal account of the Pension Fund of Russia specified in the notification, according to the specified BCC (clause 47.1 of the Procedure for accounting for receipts).

Will the Federal Tax Service return incorrect payment of insurance premiums?

It is possible that the payer of insurance premiums, having discovered an error in the KBK, transfers the payment a second time to the correct KBK.

In this case, the amount of insurance premiums will go to the PFR budget to the corresponding account of the Federal Treasury and the obligation to pay insurance premiums will be considered fulfilled.

Is it possible to return a payment made by mistake to the Federal Tax Service of Russia?

If the payer of insurance premiums contacts the tax authority, he will be denied a refund of the specified amounts, since the body controlling the payment of insurance premiums is the Pension Fund.

The tax authority is empowered to return only amounts of overpaid taxes, fees, penalties, and fines in accordance with Article 78 of the Tax Code of the Russian Federation.

The article was prepared based on materials

News

New application form for clarification of payment of pension contributions

Please note that an application for clarification of payment is submitted in the following cases:

1. An error was made in the payment order, but the contributions were received by the Pension Fund budget.

2. An error in the payment order resulted in non-payment of contributions to the Pension Fund budget.

Let's consider these cases.

1. The policyholder has the right to submit to the Pension Fund an application to clarify the payment if an error was made in the payment order, but the contributions were received into the account of the Federal Treasury and were transferred to the Pension Fund budget (Part 8, Article 18 of the Federal Law of July 24, 2009 No. 212- Federal Law). In this case, the error does not prevent the payment from entering the fund’s budget, therefore the obligation to pay contributions is considered fulfilled and penalties for the period of payment clarification are not accrued (Letter of the Pension Fund of the Russian Federation dated October 25, 2010 No. TM-30-25/11272).

For example, errors in the following details will not lead to non-payment of contributions:

INN and KPP of the payer

Payer status

KBK - if the error did not prevent the amount from entering the Pension Fund budget

Basis and type of payment

Reporting or billing period.

Let us repeat that submitting an application for clarification of payment in these cases is the right, and not the obligation, of the contribution payer. However, we recommend taking into account the rules of tax legislation, according to which the payment order will be a document confirming the reduction of certain taxes.

For example, if you are a profit tax payer, then you include the amount of insurance premiums as expenses. Thus, a payment order with an erroneous indication of the reporting period for which contributions are transferred will not confirm that the income tax was reduced for the required period. In this case, it is better to clarify the payment period. And, for example, an incorrect indication of the organization’s checkpoint will not entail any negative consequences, so an application for clarification of payment does not need to be submitted.

However, we emphasize that if the errors did not result in non-payment of contributions, then the claims of the PFR inspectors regarding insurance contributions for compulsory pension insurance are not justified, including the accrual of penalties.

If you decide to submit an application, then you need to attach a document confirming the payment of insurance premiums - a copy of the payment order by which you previously transferred contributions to the budget or a copy of a bank statement.

2. Situations where an error in a payment order resulted in non-payment of contributions for compulsory pension insurance.

Errors made in all of the above details (except for KBK) do not entail non-payment of insurance premiums. But there are other errors that prevent funds from being transferred to the required budget.

Thus, non-payment of contributions may result from incorrect indications on the payment slip:

Federal Treasury account numbers

Budget classification code - KBK

Name of the recipient's bank.

In this case, the funds received by the Federal Treasury are credited to the account of unidentified receipts (clause 10 of the Procedure for accounting by the Federal Treasury of receipts into the budget system of the Russian Federation and their distribution between the budgets of the budget system of the Russian Federation, approved by Order of the Ministry of Finance of Russia dated September 5, 2008 No. 92n, hereinafter referred to as Procedure No. 92n ). After funds are credited to the account of unknown receipts, the Federal Treasury generates requests in order to clarify whose personal account the funds should go to (clause 47 of Procedure No. 92n).

Until the funds are credited to the account of the Pension Fund of Russia, the policyholder’s obligation to pay contributions is considered not fulfilled (Clause 4, Part 6, Article 18 of Law No. 212-FZ). Therefore, the Pension Fund of Russia has the right to charge penalties for late transfer of insurance premiums.

In this situation, it is necessary to pay the amount of insurance premiums again using the required details. And then try to return or offset the incorrectly transferred payment. If the amount of contributions is too large to pay again, you can submit an application to clarify the payment both to the body into whose account the paid contributions were received and to the relevant body of the Pension Fund of the Russian Federation (recommendations of the Ministry of Finance of Russia set out in Letter dated January 21, 2011 N 03 -02-07/1-15). However, in this case, you will have to pay penalties for the period of non-payment of insurance premiums.

Despite the fact that Law No. 212-FZ does not establish a procedure for clarifying payment in the event of non-receipt of contributions to the Pension Fund budget, Art. 160.1 of the Budget Code states that the administrator of budget revenues must make a decision on the offset (clarification) of payments to various budgets and submit a corresponding notification to the Federal Treasury. Therefore, the Pension Fund, as the administrator of pension contributions, has the authority to clarify the payment.

Note that the Pension Fund cannot impose a fine for failure to transfer contributions in this case, since there is no corpus delicti under Art. 47 of Law No. 212-FZ.

We will also consider several options related to incorrect indication of KBK in the payment order:

1) The KBK was indicated incorrectly, but in it the code of the payment administrator - the Pension Fund body - was given correctly. If the Federal Treasury account is correctly indicated and the funds are credited to the Pension Fund budget. then the obligation to pay the contribution will be considered fulfilled, and penalties will not be charged on the amount of the specified payment.

For example, this situation may arise if The payment order for payment erroneously indicated the KBK for the insurance part of the pension instead of the KBK intended for contributions to the funded part of the pension. In this case, the funds will go to the Pension Fund budget, and there will be no arrears.

This position is confirmed by the judiciary in Resolutions of the Federal Antimonopoly Service of the North-Western District dated 01.06.2006 No. A13-16214/2005-08, FAS Volga District dated 11.03.2006 in case No. A55-22333/05-53, FAS Central District dated 27.01.2009 in case No. A35-4629 /08-С26 and others ).

2) The specified BCC does not exist or is administered by another body. Then the paid contributions will not go to the PFR budget, since the Federal Treasury records cash receipts and their distribution between budgets according to the BCC (clause 5 of Procedure No. 92n). Consequently, the payer of insurance premiums has an arrears and penalties are charged. Moreover, if the BCC indicated in the payment order does not exist, the Treasury will classify the contribution as unidentified income (clause 10 of Procedure No. 92n).

For example, When paying insurance premiums to the Pension Fund, the organization mistakenly indicated the BCC for income tax. The administrator of pension contributions is the Pension Fund of Russia, the administrator of income tax is the Federal Tax Service of Russia. As a result of an error, the payment will not be sent to the correct account.

The Pension Fund body must consider the application for clarification of payment and make a decision on it. The policyholder must be notified of the decision made within 5 days after its adoption (Clause 11, Article 18 of the Federal Law of July 24, 2009 No. 212-FZ).

You can view and download a sample application to clarify the details of insurance contributions for compulsory pension insurance in the Useful documents section.

HOW TO CLEAR THE TAX PAYMENT?

Clarifying the payment allows you to correct those errors in the payment order that did not lead to the fact that the tax did not go to the budget of clause 7 of Art. 45 of the Tax Code of the Russian Federation.

To do this, you must submit to the Federal Tax Service, at the location of which the tax was paid, an application to clarify the payment in any form. In your application please indicate:

1) date, number, amount and purpose of payment indicated in the payment order in which the error was made

2) which payment details are filled in incorrectly?

3) how correctly this detail should be filled out.

A copy of the payment order in which the error was made must be attached to the application.

Before making a decision to clarify the payment, the tax authority may invite you to conduct a joint reconciliation of tax calculations.

The decision to clarify the payment of the Federal Tax Service must be made by Letter of the Ministry of Finance dated July 31, 2008 N 03-02-07/1-324:

If a joint reconciliation of tax payments was carried out - within 10 working days from the date of signing the reconciliation report

If a joint reconciliation of tax calculations has not been carried out, within 10 business days from the date the Federal Tax Service Inspectorate received your application for clarification of payment.

The Federal Tax Service must inform you of the decision made within 5 working days after its adoption.

If, due to an error in the payment order, you were charged penalties, then after making a decision to clarify the payment, the Federal Tax Service will reverse them, clause 7 of Art. 45 of the Tax Code of the Russian Federation.

Sample application for clarification of tax payment

Related questions

Additionally in ConsultantPlus Guides

Publishing house "Glavnaya Kniga", 2015. Collection of typical situations. 2015-05-25.

IN _______________________________________

_________________________________________

(name of tax authority)

from ___________________________________

________________________________________

Phone number _______________________________

STATEMENT

on clarification of payment order details

to transfer payments to the budget

In the payment order dated __.__.20__ No. _______ for transfer (specify tax) to the budget in the amount of __________ rubles, the details(s) were incorrectly specified: ________________________________________________. __________________________________________________ should have been indicated.

Enclosure: payment order No. ______ dated __.__.20__ for the amount of _______ rubles, bank statement for current account No. _________________________ dated __.__.20__.

Formation of an application for clarification of payment to the tax service occurs in cases where the taxpayer, whether an individual entrepreneur or a legal entity, makes any inaccuracy.

FILES

What gives the right to clarify payment

The right to correct errors in a payment order is given by the tax code, or more precisely, paragraph 7 of article 45 of the Tax Code of the Russian Federation. However, it should be noted that not all information can be corrected on the basis of this legal norm.

What can and cannot be adjusted

There are a number of errors that are considered non-critical in payment orders, i.e. subject to editing (for example, incorrectly entered - budget classification code, name of organization, etc.) and it is they who are corrected by submitting the appropriate application to the tax office.

At the same time, there are inaccuracies that cannot be corrected in the manner described above:

- incorrectly specified name of the receiving bank;

- Invalid federal treasury account number.

In cases where the sender of the payment made errors in such details, the function of paying the contribution or tax will not be considered completed, which means the money will have to be transferred again (including late fees, if any).

What happens if you don't submit an application?

If the taxpayer company’s specialists discover errors in a timely manner, they must immediately try to correct them.

Otherwise, you will again have to transfer the tax or contribution again, and it will be possible to demand a refund of the previously paid amount and the cancellation of accrued penalties only through the courts.

Moreover, administrative sanctions from the tax service (in the form of fairly large fines) cannot be ruled out.

Who draws up the document

Typically, the responsibility for filing an application to clarify the payment to the tax office lies with the employee of the accounting department who made the payment, or with the chief accountant. In this case, the application itself must be signed not only by the employee who compiled it, but also by the head of the company.

Features of drawing up an application

An application for clarification of payment to the tax service today does not have a unified uniform form, so employees of organizations and enterprises have the opportunity to write it in any form or, if the company has a developed and approved document template, based on its sample. The main thing is that office work standards are observed in terms of the structure of the document, and some mandatory information is also entered.

In the header you need to indicate:

- addressee: name and number of the tax service department to which the application is sent, its location, position, last name, first name and patronymic of the head of the territorial inspection;

- similarly, information about the applicant company is entered into the form;

- then in the middle of the line the name of the document is written, and just below it is assigned an outgoing number and the date of preparation is indicated.

In the main part of the application you should write:

- what kind of mistake was made, indicating a link to the payment order (its number and date);

- Next, you need to enter the correct information. If we are talking about some amounts, it is better to write them in numbers and words;

- Below it is advisable to provide a link to a provision of law that allows for the inclusion of updated data in previously submitted documents;

- if any additional papers are attached to the application, this must be reflected in the form as a separate item.

What to pay attention to when filling out the form

Just like the text of the application, there are no special requirements for its execution, so it can be formed on a simple sheet of any convenient format (usually A4) or on the organization’s letterhead.

You can write the application by hand or type it on a computer.

The main thing is that the document contains a “living” signature of the head of the applicant company or a person authorized to act on his behalf (in this case, the use of facsimile autographs, i.e. printed by any method, is prohibited).

There is no strict need to certify the form with a seal - this should be done only if the use of stamp products is enshrined in the regulatory legal acts of the enterprise.

The statement should be made in duplicate, one of which is transferred to the tax office, and the second remains in the hands of the representative of the organization, but only after the tax specialist puts a mark on it accepting the document.

How to submit an application

The application can be submitted in different ways:

- The simplest, fastest and most accessible way is to come to the tax office in person and hand over the form to the inspector.

- Transfer with the help of a representative is also acceptable, but only if he has a notarized power of attorney.

- It is also possible to send the application via regular mail by registered mail with acknowledgment of receipt.

- In recent years, another method has become widespread: sending various types of documentation to government accounting and control services via electronic means of communication (but in this case the sender must have an officially registered one).

After sending the document

When tax inspectors receive the application, they will be required to check it. Sometimes (not in all cases) payments are reconciled with the taxpayer.

Five days after the application is submitted to the tax office, the inspectors will be required to make a decision and notify the applicant about it.