Accounting for leasing operations by the lessee in 1C. Accounting info

The concept of leasing appeared in our country relatively recently. This is a kind of form of lending to an enterprise when it purchases fixed assets. Leasing objects can be: equipment, structures, enterprises, transport, etc. In essence, leasing is a long-term lease of property with subsequent acquisition of ownership.

Lease purchase and registration

To record leasing on the lessee’s balance sheet, the 1C 8.3 program provides a special document “Receipt of leasing”, which can be found in “OS and intangible assets - Receipt of OS”.

Fig.1

Inside the document, please note that the accounting account is 76.07.1. We will also enter data on the purchased equipment into the tabular section. We indicate the accounting account 08.04.2* – “Acquisition of fixed assets”.

*Does not work on account 08.04.2 release 3.0.66.60.

Fig.2

We carry it out and check the accounting entries.

- Type of operation – equipment (in our example);

- Number/date – fill in the date, the number is entered automatically;

- MOL (material-responsible person) – we select and appoint an employee of the organization;

- In the location we indicate where the equipment will be used;

- OS event – in accordance with our task, we indicate what will be registered and put into operation.

After that, fill out the tabs that are below, the first of them is Non-current asset. We fill in the following information:

- Under a leasing agreement;

- Counterparty - lessor;

- Agreement – indicate our leasing agreement;

- Equipment is a leased item;

- Warehouse – indicate the warehouse where our equipment will be delivered;

- Our account is 08.04.2 “Purchase of OS”.

Fig.4

The OS tab is filled out from the directory of the same name, where we must create a new position. Click “+” and proceed to filling out the directory.

Fig.5

Fill in the following fields in the form that opens:

- Accounting group – vehicles;

- Name – we have “Car”;

- Included in the group - OS.

Fig.6

Click “Save and close.” A new position has appeared in the directory, so we feel free to continue filling out the tab by selecting our new fixed asset from the list; the inventory number is assigned automatically.

Fig.7

Filling out data for accounting purposes is carried out in the tab of the same name in the following fields:

- Account – 01.03 Leased property;

- The order is from the “Depreciation calculation” list;

- Method – Linear;

- In the accrual account we put 02.03 “Depreciation of leased property”;

- In the display of expenses, we set the debit of which accounting account the depreciation will be reflected. We have 20.01 “OS”.

- In the term, we indicate how many years we plan to depreciate this equipment; in our example, 10 years x 12 months equals 120 months.

Fig.8

On the next tab, fill in the tax data in the following fields:

- In order of inclusion in expenses – Depreciation;

- Initial cost - indicates the amount of costs excluding VAT of the lessor for the purchase of equipment. This information can be found in the leasing agreement;

- In the method of displaying costs for leasing payments, set “Depreciation” (account 20.01);

- On a monthly basis – 10 years x 12 months. That is, it turns out that the equipment is planned to be depreciated over 120 months.

Fig.9

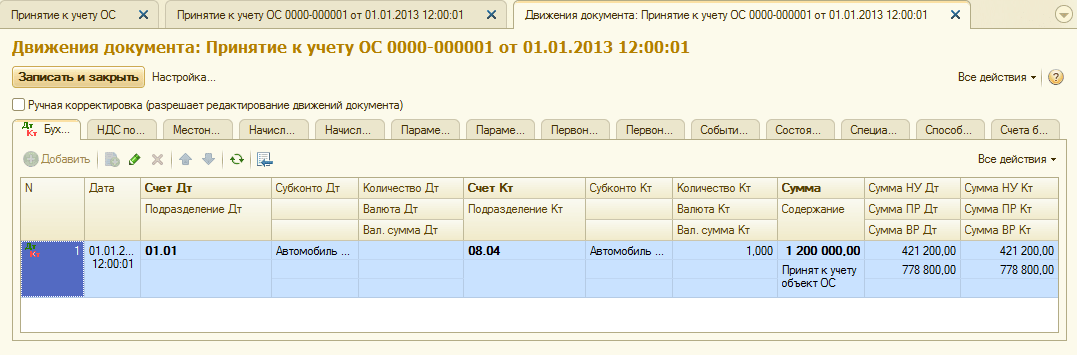

We post the document and use the DtKt button to control the postings: Dt 01 – Kt 08 “The asset has been accepted for accounting.”

The lessor will issue a monthly invoice for leasing services. To reflect these services in the 1C 8.3 program, “Receipts (acts, invoices)” is used, which is located in the “Purchases” menu.

Fig.10

When creating a receipt, indicate “Leasing services”.

Fig.11

We begin to fill out the document, be sure to indicate the number and date of the act received from the lessor, the details of the leasing agreement, as well as the organizations of the lessor and the lessee. In the “Nomenclature” we indicate “Leasing payment”, in “Amount” - the amount from the lessor’s act (invoice). Fill in the invoice number and date and click the “Register” button.

Fig.12

Please also note that our accounting account for settlements with the counterparty is 76.07.2, and for advances – 60.02.

Fig.13

The receipt data is filled in, select Post. Records of expenses for leasing services are generated in accounting and accounting records. Click DtKt and check the generated wiring.

Fig.14

In accounting, leasing payments are not included as expenses, but are accounted for as a debit 76.07.1 Lease obligations. The cost of leased equipment is recorded as a credit to this account. Thus, after all leasing payments have been made under the leasing agreement, account 76.07.1 will be closed.

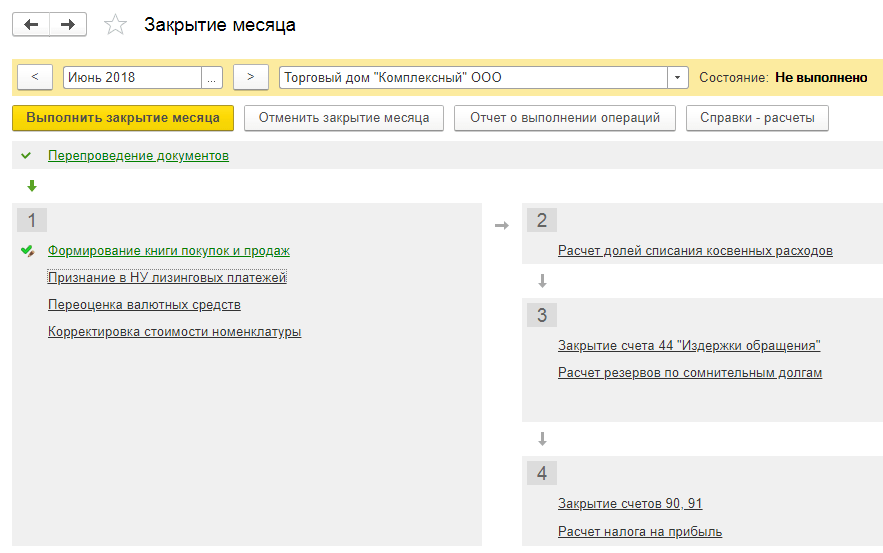

Although equipment purchased on lease is not the property of the organization, it still must be registered and depreciated accordingly. This is done through the routine operation of closing the month in “Operations - Closing the period”.

Fig.15

In conclusion, it is important to pay attention to the fact that for leasing transactions there is a difference between accounting and tax accounting, since in the latter leasing expenses are taken into account minus tax depreciation. The 1C 8.3 program will automatically calculate depreciation and leasing expenses, and also reflect the difference between accounting and tax accounting. To do this, in 1C 8.3 it is necessary to correctly draw up the accounting policy of the enterprise.

Leasing is one of the most common types of business lending. With the help of leasing, organizations can acquire ownership of expensive equipment, vehicles, and real estate. Accounting for leasing on the lessee's balance sheet in 1C 8.3 is carried out in several stages. How exactly? Read in this article.

Read in the article:

Property acquired under a leasing agreement can be accounted for in two ways:

- on the lessor's balance sheet;

- on the balance sheet of the lessee.

There is a mandatory condition in the leasing agreement that specifies who has the property on their balance sheet. If the contract specifies the method “on the lessor’s balance sheet,” then the acquired property in 1C 8.3 is reflected in off-balance sheet account 001 “Leased fixed assets.” If the agreement states “on the balance sheet of the lessee,” then use account 08 “Investments in non-current assets.” To organize leasing accounting on the lessee’s balance sheet in 1C 8.3, you need to go through 5 steps.

Step 1. Create the “Receipt for leasing” operation in 1C 8.3

The cost of the leased property is equal to the sum of all lease payments that will be transferred under the lease agreement, taking into account advances. It is this amount that must be reflected in 1C 8.3 when filling out the “Receipt for leasing” form. To do this, go to the “Fixed assets and intangible assets” section (1), click on the link “Access to leasing” (2). The “Receipt for leasing” window will open.

In the window that opens, click on the “Create” button (3). A form will open for filling out data for the “Receipt of leasing” operation.

Step 2. Fill out the “Receipt for leasing” form in 1C 8.3

In the “Receipt for leasing” window, indicate:

- your organization (1);

- lessor (2);

- details of the leasing agreement (3);

- the warehouse where the property was received (4);

- name of property (5);

- price of property (6). It consists of all lease payments.

To reflect in accounting 1C 8.3 records on the receipt of leased property, click the “Post and close” button (7).

Click on “DtKt” (8) to view the accounting entries for accounting for the operation of receiving property under lease.

In the 1C 8.3 posting window, we see that the cost of leased property without VAT (9) is reflected in the debit of account 08.04.1 “Purchase of components of fixed assets” and the credit of account 76.07.1 “Rental obligations”. The amount of VAT (10) is recorded in the debit of account 76.07.9 “VAT on lease obligations” and the credit of account 76.07.1 “Rease obligations”.

Step 3. Create in 1C 8.3 the operation “Acceptance for accounting of fixed assets”

Go to the section “Fixed assets and intangible assets” (1) and click on the link “Acceptance for accounting of fixed assets” (2). A window will open to reflect this operation.

In the window that opens, click on the “Create” button (3). A form will open for filling out the “Acceptance for accounting of fixed assets” operation.

At the top of the form please indicate:

- your organization (1);

- financially responsible person (2);

- subdivision where the property is located (3).

In the “Non-current asset” tab (4), fill in the fields:

- “Method of entry” (5). Select the value “Under a leasing agreement”;

- "Counterparty" (6). Specify the lessor;

- "Treaty" (7). Provide the details of the leasing agreement;

- "Equipment" (8). Select the property received under a leasing agreement;

- "Warehouse" (9). Indicate the warehouse where the property is located.

Step 4. Fill out the “Fixed Assets” tab

In the “Fixed Assets” tab (1) you need to create a new fixed asset in the “Fixed Assets” directory. To do this, click on the “+” button (2). A form for creating a fixed asset in the directory will open.

Fill out the fields in this form:

- “Assets accounting group” (3). Select the value that suits you from the list, for example “Vehicles”;

- “Name” and “Full name” (4). Indicate the name of the fixed asset;

- “Part of the group” (5). Select the appropriate group from the list, for example “Transport”.

After filling in the fields, click on the “Record and close” button (6). There is now a new fixed asset in the Fixed Assets directory.

Indicate this fixed asset in field (7). The tab is full.

Step 5. Complete the Accounting Tab

In the “Acceptance for accounting of fixed assets” form, go to the “Accounting” tab (1). Fill in the fields:

- “Accounting procedure” (2). Select “Depreciation calculation” from the list;

- “Method of calculating depreciation” (3). Specify "linear";

- “Method of reflecting depreciation expenses” (4). Here, indicate in the debit of which account the depreciation will be reflected, for example, “Depreciation (account 20.01)”;

- “Useful life (in months)” (5). In this field, write the depreciation period in months. For example, if the property is planned to be depreciated over 8 years, then the period will be 96 months (8 years x 12 months).

Step 6. Complete the “Tax Accounting” tab

In the “Tax Accounting” tab (1), fill in the fields:

- “The procedure for including costs in expenses” (2). Select “depreciation calculation”;

- "Initial cost" (3). Here, indicate the amount of expenses (excluding VAT) of the lessor for the purchase of property. Information on these costs can be found in the leasing agreement;

- “Method of reflecting expenses on leasing payments” (4). Specify the value “Depreciation (account 20.01)”;

- “Useful life (in months)” (5). In this field, write the depreciation period in months in tax accounting. For example, if the property is planned to be depreciated over 8 years, then set it to 96 months (8 years x 12 months).

To reflect in the accounting records on the acceptance of property for accounting, click “Record” (6) and “Post” (7). The following entries will be made in accounting:

DEBIT 01 CREDIT 08

- fixed assets object is accepted for accounting

To see the postings in 1C 8.3, click on the “DtKt” button (8).

Step 7. Reflect leasing services in 1C 8.3

The lessor will issue you a monthly invoice for leasing services. In 1C 8.3 there is a special act to reflect expenses for them. To create it, go to the “Purchases” section (1) and click on the link “Receipts (acts, invoices) (2). A window for creating an act will open.

In the window that opens, click the “Receipt” button (3) and select “Leasing Services” (4). An act for reflecting leasing services “Receipt of leasing services” will open.

Indicate in it:

- number and date of the act received from the lessor (5);

- your organization (6);

- lessor (7);

- details of the leasing agreement (8).

In the “Nomenclature” field (9) indicate “Leasing services”, in the “Amount” field (10) - the amount according to the act (invoice). To generate an invoice, enter its number (11) and date (12), and click the “Register” button (13). The act is completed, click on the “Post and close” button (14). Now in accounting and tax accounting there are entries for expenses for leasing services.

After closing the act, you will again be taken to the “Receipts (acts, invoices)” window. It contains a list of all created acts. To view accounting and tax entries for leasing expenses, click on the act and press the “DtKt” button (15). Postings will open in accounting 1C 8.3.

The entries show that in accounting, leasing payments are not included as expenses, but are recorded as a debit to account 76.07.1 “Lease obligations” (16). It is the credit of this account that reflects the amount of equipment received for leasing. Thus, after all lease payments are paid according to the schedule, account 76.07.1 will be closed.

Leasing expenses are taken into account for tax purposes minus tax depreciation of leased property. 1C 8.3 automatically calculates depreciation of such property and leasing expenses for tax accounting purposes. This is done by the “Month Closing” operation, which we wrote about in detail in this article. In this case, the operation “Recognition of leasing payments in NU” is automatically created.

Please note that for leasing transactions there is a difference between accounting and tax accounting. 1C 8.3 will automatically reflect these differences. To do this, in 1C 8.3 you need to set up an accounting policy, indicating in it that your organization keeps records in accordance with the current edition of PBU 18.

Reflection of transactions under leasing agreements in the program

"1C:Accounting 8" (edition 3.0)

The word "leasing" is borrowed from the English language. It comes from the verb “to lease”, which means “to rent, to rent”. Indeed, there are many similarities between leasing and renting. However, these concepts should not be identified.

Rent consists of the lessor transferring his property for use and temporary possession to the lessee for a fee. The object of lease can be both movable and immovable property, including land plots.

Leasing(the so-called financial lease) consists in the fact that the lessor undertakes to acquire ownership of new property specified by the lessee from a specific supplier and provide this property to the lessee for a fee for temporary possession and use (clause 4 art. 15 Federal Law dated October 29, 1998 No. 164-FZ). The subject of a leasing agreement can be any non-consumable items. As a rule, these are fixed assets, with the exception of land plots and environmental management facilities. Moreover, depending on the terms of the agreement, the lessee has the right to buy this property at the end of the leasing agreement by paying the redemption price, or return it to the lessor.

Thus, unlike a lease agreement, a leasing agreement implies the emergence of legal relations between three parties: the seller of the property, the lessor and the lessee, and also gives the lessee the right to acquire ownership of the leased asset at the end of the agreement.

The redemption price is paid either in a lump sum at the end of the leasing agreement, or in equal shares as part of the leasing payments. According to Art. 28 Federal Law “On financial lease (leasing)” “Leasing payments mean the total amount of payments under the leasing agreement for the entire term of the leasing agreement, which includes reimbursement of the lessor’s costs associated with the acquisition and transfer of the leased asset to the lessee, reimbursement of costs associated with the provision of other provided service leasing agreement, as well as the lessor’s income. The total amount of the leasing agreement may include the redemption price of the leased asset if the leasing agreement provides for the transfer of ownership of the leased asset to the lessee."

In the event that, at the end of the contract, the property becomes the property of the lessee, the purchase price of the property must be indicated in the contract (or an addition/appendix to it) (letters from the Ministry of Finance of the Russian Federationdated 09.11.2005 No. 03-03-04/1/348 And dated 09/05/2006 No. 03-03-04/1/648 ) and the procedure for its payment. At the same time, the presence or absence of a redemption price in the contract affects only the tax accounting of leasing transactions.

The redemption price is taken into account for tax purposes separately from the other amount of lease payments in any order of its payment (letter from the Ministry of Finance of the Russian Federationdated 02.06.2010 No. 03-03-06/1/368 ). No matter how the redemption price is paid: in parts during the term of the contract as part of leasing payments, or at some point in full, or in several separate payments, the lessee is an advance paid. Like any other advance paid, until the transfer of ownership, the redemption price is not an expense taken into account when calculating income tax. Thus, the lessee's expense taken into account when calculating income tax is only reimbursement of the lessor's costs associated with the acquisition and transfer of the leased asset to the lessee, reimbursement of costs associated with the provision of other services provided for in the leasing agreement, as well as the lessor's income.

At the time of transfer of ownership, the redemption price paid to the lessor forms the initial tax value of the depreciated property. Depreciation is charged by the lessee in the usual manner, as when purchasing used property.

Accounting for transactions related to a leasing agreement is regulated Instructions on the reflection in accounting of operations under a leasing agreement, approved. by order of the Ministry of Finance of Russia dated February 17, 1997 No. 15.

During the period of validity of the leasing agreement, depending on its terms, the property may be on the balance sheet of the lessor or on the balance sheet of the lessee. The most difficult case from the point of view of accounting and tax accounting of leasing operations is the case when the property is on the balance sheet of the lessee (accounting from the position of the lessee). Let us consider, using a specific example, the sequence of accounting operations in the program “1C: Accounting 8”, edition 3.0 (hereinafter referred to as the “program”) for the lessee in the specified case, taking into account the options when the property is purchased at the end of the leasing agreement or returned to the lessor.

Example

Yantar LLC (lessee) entered into leasing agreement No. 001 dated January 1, 2013 with Euroleasing LLC (lessor) for a period of 6 months. The subject of leasing is a FIAT car, which was accepted on the balance sheet of Yantar LLC on January 1, 2013. The costs of its acquisition by the lessor amount to 497,016 rubles. (including VAT 18% - RUB 75,816). Under the terms of the leasing agreement, the cost of a FIAT car, taking into account the redemption price, is 1,416,000 rubles. (including VAT 18% - RUB 216,000). In this case, the redemption price of the vehicle is paid in equal monthly installments along with leasing payments. The monthly amount of leasing payments is 106,200 rubles. (including VAT 18% - 16,200 rubles). The redemption price is 778,800 rubles. (including VAT 18% - 118,800 rubles) and its monthly amount is 129,800 rubles. (including VAT 18% - RUB 19,800). The useful life of the vehicle is 84 months. Depreciation is calculated using the straight-line method. At the end of the contract, the FIAT car becomes the property of Yantar LLC.

The following transactions must be generated in the program (Table 1).

Table 1 - Accounting entries under the leasing agreement

|

Debit |

Credit |

||||||||

|

For accounting and tax accounting, appropriate entries are made in analytical registers |

|||||||||

As a result of posting the “Receipt of goods and services” document, the following transactions will be generated (Fig. 2).

Rice. 2 - Postings of the document “Receipt of goods and services”

As mentioned above, until the transfer of ownership of the property to the lessee, the redemption price is not taken into account when calculating income tax. Therefore, we will resort to manual adjustment of document movements and in the columns “Amount NU Dt”, “Amount NU Kt” we will enter the amount of the lessor’s expenses for the acquisition of property (excluding VAT) - 421,200 rubles. Redemption price 778,800 rubles. We will reflect the difference as a constant, putting it in the appropriate columns (Fig. 3).

Rice. 3 - Manual adjustment of entries in the “Receipt of goods and services” document

3. To perform the operation of accepting a fixed asset for accounting, you must create a document “Acceptance for accounting of fixed assets” (Fig. 4). This document registers the fact of completion of the formation of the initial cost of a fixed asset item and (or) its commissioning. When creating a fixed asset, it is advisable to create a special folder in the “Fixed Assets” directory for fixed assets received on lease.

The initial cost of the object, which is planned to be taken into account as fixed assets, is formed on account 08 “Investments in non-current assets”.

Rice. 4 - Acceptance of fixed assets for accounting

We will also fill in the “Accounting” and “Tax Accounting” tabs of the document “Acceptance of fixed assets for accounting”, as shown in Fig. 5 and 6.

Rice. 5 - Filling out the “Accounting” tab

Rice. 6 - Filling out the “Tax Accounting” tab

As a result of the document “Acceptance for accounting of fixed assets”, the following transactions will be generated (Fig. 7).

Rice. 7 - Postings of the document “Acceptance for accounting of fixed assets”

4. At the end of the first month of the leasing agreement, the next leasing payment is accrued. To reflect this operation, you can enter the operation manually or use the “Debt Adjustment” document (the “Purchases and Sales” tab, the “Settlements with Counterparties” section) with the “Debt Transfer” operation type (Fig. 8).

Rice. 8 - Filling out the “Debt Adjustment” document

In the “Amount” field, we will manually enter the amount of the next lease payment of 236,000 rubles. = 1,416,000 rub. / 6 months (contract time).

In the “New accounting account” field, indicate account 76.09 “Other settlements with various debtors and creditors.” It is he who will appear as a loan account as a result of posting the document (Fig. 9).

Rice. 9 - Posting the accrual of the lease payment

All other monthly lease payments can be calculated in the same way.

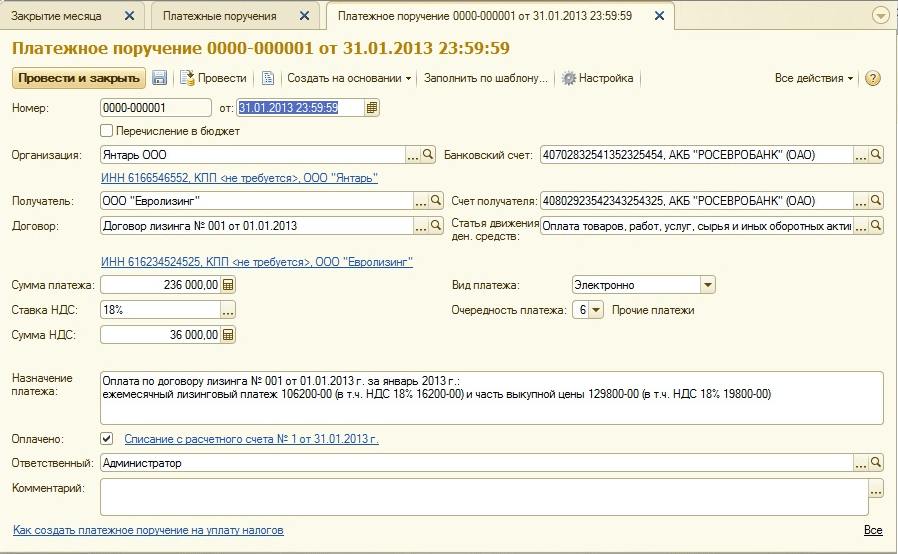

5. We will transfer the next lease payment to the lessor. To do this, we will first create the document “Payment order” (Fig. 10), and then, based on this document, we will enter the document “Write-off from the current account” (Fig. 11).

Rice. 10 - Payment order for transfer of lease payment

Rice. 11 - Debiting the lease payment from the current account

After receiving a bank statement, which records the debiting of funds from the current account, it is necessary to confirm the previously created document “Writing off from the current account” to generate transactions” (checkbox “Confirmed by bank statement” in the lower left corner of the form in Fig. 11).

When posting the document, posting Dt 76.09 - Kt 51 is generated (Fig. 12), because according to the conditions of our example, the fact of receiving material assets (fixed assets) is first recorded, then the fact of payment, i.e. at the time of payment there was an account payable to the supplier. As a result of business transactions, accounts payable were repaid.

Rice. 12 - Result of posting the document “Write-off from the current account”

6. The initial cost of the leased object is included in expenses through depreciation charges. Since the leased asset is on the balance sheet of the lessee, he charges monthly depreciation charges on the leased asset in the amount of the depreciation rate calculated based on the useful life of this object.

To calculate the amount of depreciation charges, we will perform the “Month Closing” procedure in the “Accounting, Taxes, Reporting” section (this can also be done using the routine operation “Depreciation and depreciation of fixed assets” on the “Fixed Assets and Intangible Assets” tab). First, we will close January (depreciation will not be accrued in January, since fixed assets were taken into account in this month), and then February (Fig. 13). Before calculating depreciation and carrying out any other routine operations to close the month, it is necessary to monitor the sequence of documents.

Rice. 13 - Calculation of depreciation using the “Closing of the month” operation

As a result, the following wiring will be generated (Fig. 14)

As you can see, the posting reflects a constant difference of 9271.43 rubles, which arose due to the difference in the cost of fixed assets in accounting and tax accounting. This difference will be formed throughout the entire period of depreciation in tax accounting.

In addition to depreciation deductions, expenses in the form of leasing payments minus the amount of depreciation on the leased property are recognized monthly in the tax accounting of the lessee. In this regard, taxable temporary differences arise, which lead to the formation of deferred tax liabilities, reflected in the debit of account 68 “Calculations for taxes and fees” and the credit of account 77 “Deferred tax liabilities”. The adjustment amount is determined as the difference between the monthly lease payment excluding VAT and the amount of depreciation, multiplied by the income tax rate.

If the monthly depreciation amount exceeds the lease payment amount, only depreciation on the leased object will be taken into account in tax accounting expenses.

Obviously, in our example, the amount of monthly depreciation deductions is less than the amount of leasing payments. The difference is

200,000 - 14,285.71 = 185,714.29 rubles.

Therefore, it is necessary to reflect this difference as temporary for tax accounting purposes.

To pay off monthly deferred tax liabilities in accounting, you can use the operationentered manually (tab “Accounting, taxes, reporting”, section “Accounting”, item “Operations (accounting and accounting)”). The generated wiring is shown in Fig. 15. The amount of the entered transaction is equal to the above temporary difference multiplied by the income tax rate:

185,714.29 * 0.2 = 37,142.86 rubles.

Rice. 15 - Entering a manual transaction to settle a deferred tax liability

7. To reflect VAT on the lease payment accepted for deduction, we will create a document “Reflection of VAT for deduction” (tab “Accounting, taxes, reporting”, section “VAT”). Let's fill it in as shown in Fig. 16. As a payment document, we will indicate the “Debt Adjustment” document corresponding to this lease payment.

Rice. 16 - Reflection of VAT on lease payment for deduction

It is also necessary to create an invoice received based on the created document (Fig. 17).

Rice. 17 - Form “invoice received” for lease payment

The posting generated by the document “Reflection of VAT for deduction” is shown in Fig. 18

Rice. 18 - Result of conducting the document “Reflection of VAT for deduction”

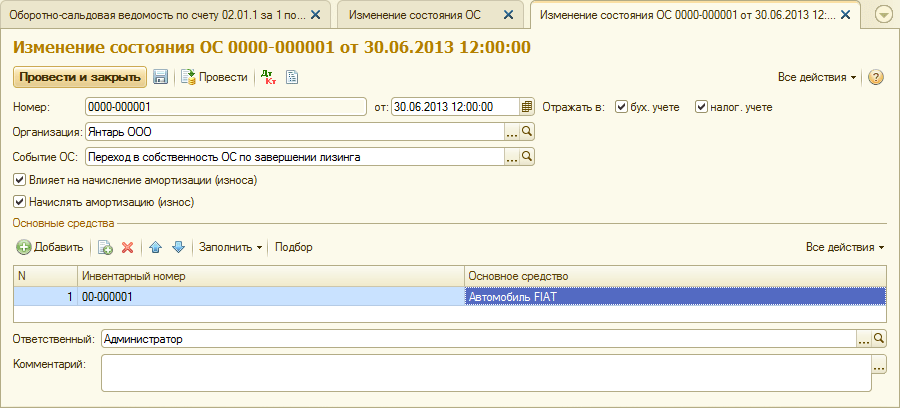

8 . Upon expiration of the lease agreement and payment of the entire amount of lease payments, including the redemption price, the object is transferred to its own fixed assets.

To reflect changes in the state of the OS, the document “Changes in the state of OS” can be used (tab “Fixed assets and intangible assets”). Let's fill out its form, as shown in Fig. 19. If the “Transition of ownership of the OS upon completion of leasing” event is not in the “Asset Event” list, it must be created. When creating, specify the OS event type as “Internal movement”.

Rice. 19 - Changing the OS state

After the transfer of ownership, depreciation parameters may change due to a change in the value of the fixed assets in tax accounting or a change in the acceleration coefficient (Fig. 20).

Rice. 20 - Changing depreciation parameters

The remaining useful life of the asset in months is indicated here (84 - 6 = 78), and the redemption price is entered in the “Depreciation (PR)” column (the difference in the initial estimate of the cost of the asset in the accounting book and NU). In the future, depreciation in NU will be calculated based on the redemption price.

In conclusion, let us consider the case when the property is returned to the lessor upon completion of the leasing agreement.

To register this fact in the program, you must use a manual operation (Fig. 21).

Rice. 21 - Reflection of the return of property to the lessor

We generate transactions Dt 01.09 (“Disposal of fixed assets”) - Kt 01.01, as well as Dt 02.01 - Kt 01.09. Thus, the property was returned to the lessor with full depreciation value.

Your company has already entered into a leasing agreement and you have questions about how to reflect leasing in accounting? In this article you can find the necessary information and examples of accounting entries for various leasing transactions.

Accounting for transactions under a leasing agreement is regulated by Order of the Ministry of Finance of the Russian Federation No. 15 dated February 17, 1997.

Leasing transactions depend on whose balance sheet the leased property is reflected in: the lessor or the lessee. The party on whose balance sheet the leased property is accounted for must be indicated in the leasing agreement.

Accounting for leasing when reflecting property on the lessor’s balance sheet

payment schedule .

If the leasing agreement provides for the reflection of the leased asset on the lessor's balance sheet, the lessee reflects the leased property on off-balance sheet account 001 "Leased fixed assets".

The accrual of leasing payments is reflected in the credit of account 76 “Settlements with various debtors and creditors” in correspondence with cost accounts: 20, 23, 25, 26, 29 – when accounting for leasing payments on property that is used in production activities, 44 – on property used in the activities of a trade organization, 91.2 - for property that is used for non-production purposes. Further, for simplicity, in the leasing accounting examples, only entries for the 20th account will be given.

Dt 001 - 1,000,000(the leased asset is accepted for accounting at cost excluding VAT)

Dt 60 – Kt 51 – 236,000(advance payment (down payment) under the leasing agreement has been paid)

It is necessary to take into account that the advance payment under the leasing agreement can be charged as expenses (offset of the advance payment) not immediately, but throughout the entire agreement. In the above payment schedule, the advance payment under the contract is offset evenly (RUB 6,555.56 each) over 36 months.

Dt 20 – Kt 76 – 29,276.27(accrued leasing payment No. 1 – 34,546 minus VAT – 5,269.73)

Dt 19 – Kt 76 – 5,269.73(VAT charged on lease payment No. 1)

Dt 20 – Kt 60 – 5,555.56(part of the advance payment under the leasing agreement is credited - 6,555.56 minus VAT 1,000)

Dt 19 – Kt 60 – 1,000(VAT is calculated based on the advance payment)

Dt 68 – Kt 19 – 6,269.73(VAT submitted to the budget)

Dt 76 – Kt 51 – 34 546(listed leasing payment No. 1)

The commission that is paid at the beginning of the leasing transaction (commission for concluding the transaction) is charged in accounting to the same expense accounts as current leasing payments.

Postings for the redemption of the leased asset

If there is a buyout price in the leasing agreement (this amount is not included in the leasing payment schedule, for example, let’s take it equal to 1,180 rubles including VAT), the following entries are made in accounting:

Dt 08 – Kt 76 – 1,000(reflects the costs of repurchasing the leased asset upon transfer of ownership to the lessee)

Dt 19 – Kt 76 – 180(VAT is charged when purchasing the leased asset)

Dt 68 – Kt 19 – 180(VAT submitted to the budget)

Dt 76 – Kt 51 – 1 180(the amount of redemption of the leased asset has been paid)

Dt 01 – Kt 08 – 1 000(the leased asset was accepted for accounting as part of its own fixed assets)

Accounting for leasing when reflecting property on the lessee’s balance sheet

The legislation regulating leasing accounting does not contain unambiguous instructions on the reflection of transactions under a leasing agreement if the lessee is the balance holder of the property.

Currently, the practice of communication between lessees and leasing companies with auditors and inspection bodies has developed, and a certain scheme of leasing transactions has been formed.

Accounting for leasing when reflecting property on the lessee’s balance sheet

If, under the terms of the leasing agreement, the property is taken into account on the lessee’s balance sheet, upon receipt of the leased asset in the lessee’s accounting, the value of the property minus VAT is reflected in the debit of account 08 “Investments in non-current assets” in correspondence with the credit of account 76 “Settlements with various debtors and creditors”.

When a leased asset is accepted for accounting as part of fixed assets, its value is written off from credit 08 of account to debit 01 of account “Fixed Assets”.

The accrual of lease payments is reflected in the debit of account 76, subaccount, for example, “Settlements with the lessor” in correspondence with account 76, subaccount, for example, “Settlements for leasing payments”.

Depreciation on the leased asset is calculated by the lessee. The amount of depreciation of the leased asset is recognized as an expense for ordinary activities and is reflected in the debit of account 20 “Main production” in correspondence with the credit of account 02 “Depreciation of fixed assets, subaccount for depreciation of leased property.

Tax accounting of leasing when reflecting property on the lessee’s balance sheet

In the tax accounting of the lessee, leased property is recognized as depreciable property.

The initial cost of the leased asset is determined as the amount of the lessor's expenses for its acquisition.

For profit tax purposes, the monthly depreciation amount is determined based on the product of the original cost of the leased asset and the depreciation rate, which is determined based on the useful life of the leased property (taking into account the classification of fixed assets included in depreciation groups). In this case, the lessee has the right to apply a coefficient of up to 3 to the depreciation rate. The specific size of the increasing coefficient is determined by the lessee in the range from 1 to 3. This coefficient does not apply to leased property belonging to the first to third depreciation groups.

Leasing payments minus the amount of depreciation on leased property are expenses associated with production and sales.

An example of accounting for leasing when reflecting property on the lessee’s balance sheet

Leasing transactions correspond to the payment schedule for property leasing located at the link

The lessee received a passenger car under a leasing agreement, payment schedule parameters:

- leasing agreement term – 3 years (36 months)

- the total amount of payments under the leasing agreement is 1,479,655.10 rubles, incl. VAT – 225,710.10 rubles

- advance payment (down payment) – 20%, 236,000 rubles, incl. VAT – 36,000 rubles

- car cost – 1,180,000 rubles, incl. VAT – 180,000 rubles

The expected period of use of the leased property is four years (48 months). The car belongs to the third depreciation group (property with a useful life of 3 to 5 years). Depreciation is calculated using the straight-line method.

Let's determine the amount of monthly depreciation in accounting. Because the cost of the property (including the leasing company's remuneration) is equal to 1,253,945 rubles (1,479,655.10 - 225,710.10), monthly depreciation will be 1,253,945: 48 = 26,123.85 rubles.

A passenger car belongs to the third depreciation group, therefore, a period of 48 months can be established in tax accounting. The monthly depreciation rate is 2.0833% (1: 48 months x 100%), the monthly depreciation amount is 1,000,000 x 2.0833% = 20,833.33 rubles.

In accordance with paragraph 10 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation, the amount of the lease payment recognized monthly as an expense for profit tax purposes is 8,442.94 rubles (34,546 (lease payment) - 5,269.73 (VAT as part of the lease payment) – 20,833.33 (monthly depreciation in tax accounting)).

Expenses under the leasing agreement are formed monthly in accounting due to depreciation (26,123.85 rubles), in tax accounting - due to depreciation (20,833.33 rubles) and leasing payment (8,442.94 rubles), a total of 29,276 ,27 rubles.

Because in accounting, the amount of expenses over 36 months (the term of the leasing agreement) is less than in tax accounting, this leads to the emergence of taxable temporary differences and deferred tax liabilities.

During the term of the leasing agreement, the lessee has a monthly taxable temporary difference in the amount of 3,152.42 rubles (29,276.27 - 26,123.85) and a corresponding deferred tax liability arises in the amount of 630.48 rubles (3,152.42 x 20% ).

Separately, it is necessary to say about accounting for advance payments (down payment under the contract). The following situations are possible:

1. When transferring property for leasing, the lessor provides an invoice for the full amount of the advance(in the given schedule of leasing payments - by 236,000 rubles). In this case, the entire amount of the advance payment of the advance payment, minus VAT, in tax accounting is recognized as an expense for profit tax purposes.

I would like to note that under the leasing agreement, services are provided throughout the entire contract and the fiscal authorities have no reason to assess compliance with the criteria of paragraph 4, paragraph 2 of Article 40 of the Tax Code of the Russian Federation on the comparability of leasing payments, because individual payments cannot be considered as separate transactions, and the price under a leasing agreement must be analyzed in aggregate for all payments in the agreement.

2. The advance payment under the leasing agreement is offset in equal payments throughout the entire leasing term. In this case, the offset portion of the advance payment is recognized as an expense in tax accounting for profit tax purposes.

In the given example of a leasing payment schedule, it is assumed that an advance invoice is issued to the lessee when the property is leased, i.e. In tax accounting, when transferring property into leasing, expenses in the amount of 200,000 rubles are reflected (the advance payment, which is a leasing payment, is not deducted, since in the first month when transferring property into leasing, it is not yet accrued). At the same time, a taxable temporary difference arises in the amount of 200,000 rubles and a corresponding deferred tax liability in the amount of 40,000 rubles (200,000 rubles x 20%).

At the end of the leasing agreement, the lessee will continue to accrue monthly depreciation in accounting in the amount of 26,123.85 rubles. There will be no expenses in tax accounting. This will lead to a monthly decrease in deferred tax liabilities in the amount of 5,224.77 rubles (26,123.85 rubles x 20%).

Thus, based on the results of the agreement, the total amount of deferred tax liabilities will be equal to zero:

40,000 (deferred tax liability for the advance payment) + 22,697 (630.48 x 36 – deferred tax liability for current lease payments) – 62,697 (5,224.77 x 12 – reduction of deferred tax liabilities for 12 months of depreciation in the accounting accounting after the end of the leasing agreement).

Postings upon receipt of the leased asset

Dt 60 – Kt 51 – 236,000(advance paid under the leasing agreement)

Dt 08 – Kt 76 (Settlements with the lessor) – 1,253,945(debt under the leasing agreement is reflected without VAT)

Dt 19 – Kt 76 (Settlements with the lessor) - 225,710.10(VAT reflected under the leasing agreement)

Dt 01 – Kt 08 – 1 253 945(a car received under a leasing agreement is accepted for registration)

Dt 76 – Kt 60 – 236,000(advance payment paid upon concluding the leasing agreement is included)

Dt 68 (Income tax) – Kt 77 – 40,000

Dt 68 (VAT) – Kt 19 – 36,000(VAT submitted on advance payment)

Postings for current lease payments

Dt 20 – Kt 02 – 26 123.85

Dt 76 (Settlements with the lessor) - Kt 76 (Settlements for leasing payments) - 34,546(leasing debt has been reduced by the amount of the lease payment)

Dt 76 “Calculations for leasing payments” – Kt 51 – 34,546(leasing payment transferred)

Dt 68 (VAT) – Kt 19 – 5,269.73(VAT is presented on the current lease payment)

Dt 68 (Income tax) – Kt 77 – 630.48(deferred tax liability reflected)

Postings at the end of the leasing agreement

Dt 01 (Own fixed assets) – Kt 01 (Fixed assets received under leasing) – 1,253,945(reflects the receipt of the car into ownership)

Dt 02 (Depreciation of leased property) – Kt 02 (Depreciation of own fixed assets) – 940,458.60(accrued depreciation on the car is reflected)

Postings within 12 months after the end of the leasing agreement

Dt 20 – Kt 02 (Depreciation of own fixed assets) – 26,123.85(depreciation has been calculated on the car)

Dt 77 – Kt 68 (Income tax) – 5,224.77(reflects a decrease in deferred tax liability)

There is also a method in which the initial cost of the leased asset in accounting is equal to the cost of purchasing a car from the lessor, i.e. coincides with the value in tax accounting. In this case, on account 76, when the property is accepted for accounting, only the debt for the value of the property is reflected.

Leasing payments are accrued monthly on credit 20 of account in correspondence with account 76 in the amount of the difference between accrued depreciation and the amount of the monthly lease payment.

Selecting the most reasonable option for reflecting leased property on the balance sheet of the lessor or lessee, as well as agreeing with the leasing company on the optimal scheme for reflecting lease payments, is a very complex task that requires good knowledge of the specifics of accounting for leasing operations and the peculiarities of the wording in the leasing agreement and primary documents.

Leasing is a popular form of financing capital investments. After all, without incurring significant one-time costs compared to the value of the property, the lessee, having concluded a leasing agreement with the lessor and paying lease payments, will receive the necessary property for temporary possession and use (Article 2 of Federal Law No. 164-FZ of October 29, 1998).

We will show you with examples in our consultation how to keep accounting records for the lessee if the object is accounted for on the balance sheet of one or the other party to the agreement.

Leasing transactions if the property is on the lessor’s balance sheet: example

Let's imagine typical leasing transactions with the lessee, if the object is listed on the lessor's balance sheet, using the following example.

In accordance with the leasing agreement, the fixed asset object is transferred to the lessee for a period of 5 years. The total amount of leasing payments for this period is 3,540,000 rubles, incl. VAT 18%. Payments under the agreement are made monthly.

The leasing agreement also stipulates that at the end of its validity period the object is purchased by the lessee at the redemption price of 34,220 rubles, incl. VAT 18%.

| Operation | Account debit | Account credit | Amount, rub. |

|---|---|---|---|

| Leased property is registered off balance sheet | 001 “Leased fixed assets” | 3 540 000 | |

| Monthly lease payment transferred (3 540 000 / 60) | 76 “Settlements with various debtors and creditors”, subaccount “Debt on leasing payments” | 51 “Current accounts” | 59 000 |

| Monthly lease payment taken into account (59 000 * 100/118) | 20 “Main production”, 26 “General business expenses”, 44 “Sales expenses”, etc. | 50 000 | |

| VAT included in the leasing payment (50 000 * 18%) | 19 “VAT on purchased assets” | 76, subaccount “Debt on leasing payments” | 9 000 |

| Accepted for deduction of VAT on leasing payment | 19 | 9 000 | |

| ………… | |||

| Leased property was written off off-balance sheet due to the expiration of the leasing agreement | 001 “Fixed assets” | 3 540 000 | |

| 60 “Settlements with suppliers and contractors” | 51 | 34 220 | |

| Leased property was accepted for accounting at redemption value as part of inventory | 10 "Materials" | 60 | 29 000 |

| VAT is included on the redemption value of the property | 19 | 60 | 5 220 |

| Accepted for deduction of VAT from the redemption price | 68 “Calculations for taxes and fees” | 19 | 5 220 |

Leasing transactions if the property is on the balance sheet of the lessee: example

Let's present the accounting of leasing on the lessee's balance sheet (posting) using the example discussed above, supplementing it with information that depreciation on leased property is calculated using the straight-line method.

| Operation | Account debit | Account credit | Amount, rub. |

|---|---|---|---|

| The leasing object was accepted for accounting (3,540,000 * 100 / 118) | 08 “Investments in non-current assets” | 3 029 000 | |

| Presented VAT by the lessor | 19 | 76, subaccount “Rental obligations” | 545 220 |

| The object is accepted for accounting as part of fixed assets | 01 “Fixed assets”, subaccount “Property under lease” | 08 | 3 029 000 |

| Lease payment transferred (3,540,000 / 60) | 76, subaccount “Debt on leasing payments” | 51 | 59 000 |

| Monthly lease payment taken into account | 76, subaccount “Rental obligations” | 76, subaccount “Debt on leasing payments” | 59 000 |

| Accepted for deduction of VAT regarding the lease payment | 68 | 19 | 9 000 |

| Monthly depreciation accrued (3 029 000 / 60) | 20, 26, 44, etc. | 02 “Depreciation of fixed assets”, subaccount “Property under lease” | 50 483 |

| ………… | |||

| The debt for the redemption value of the leased property is reflected | 76, subaccount “Rental obligations” | 34 220 | |

| The redemption value of the leased property is listed | 76, subaccount “Debt for redemption of property” | 51 | 34 220 |

| Fixed assets were transferred from leased to owned | 01, subaccount “Own fixed assets” | 01, subaccount “Property on lease” | 3 029 000 |

| Depreciation on leased property that has become the property of the lessee is reflected | 02, subaccount “Property on lease” | 02, subaccount “Own fixed assets” | 3 029 000 |