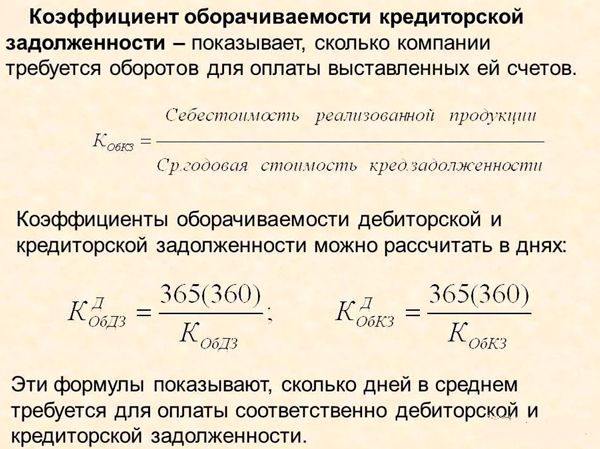

Receivables turnover rate. An example of receivables turnover analysis

The receivables turnover period is the period from the moment the goods are shipped until payment is received. To evaluate it, a coefficient is used; the indicator can also be calculated in days. The faster debts turn into money, the more stable the economic position of the company, and the lower the risk of a shortage of working capital liquidity.

The receivables turnover period is a coefficient that evaluates the period during which an enterprise receives payment from its debtors for goods shipped or services provided. This indicator is needed to assess the cash flows of an enterprise. Its calculation helps determine how stable the company’s position is, whether there are funds to pay accounts payable and make other payments.

In other words, the coefficient shows how much turnover accounted for one ruble of debt, what share of revenue is the debt of clients to the company. Any company needs to strive for the highest value, because... The larger it is, the faster the debts are repaid. Ideally, it is better to minimize debt, but if this is not possible, you need to increase the ratio in future periods.

Formula

Several formulas are used to calculate the indicator.

The general formula for calculating accounts receivable turnover for any period:

- KOdz - accounts receivable turnover ratio;

- B - revenue (RUB);

- DZ kp - accounts receivable at the end of the period;

- DZ np - accounts receivable at the beginning of the period.

Formula for calculating the turnover period in days:

![]()

- Ost dz - average balance of accounts receivable;

- IN - .

![]()

- SO dz - average balance of accounts receivable;

- 365 - the number of days in a year (if calculated for another period, take the actual number of days).

- 2110 - string value 2110;

- 1230 kp - line value 1230 at the end of the period;

- 230 np - the value of line 1230 at the beginning of the period.

Important!

- Revenue must be calculated on the date of shipment (service provision).

- There is no need to remove VAT and excise taxes from the revenue amount, because they are also contained in the receivables amount.

How to analyze the indicator

The ratio is used to analyze the cash flows of an enterprise over several periods. It is compared whether there was growth or decline. Growth means that the situation has become better, the share of receivables is decreasing. A decline is, on the contrary, a sad sign. It signals one thing: customer debts are growing.

It would be optimal to take data for the previous year and calculate the indicator quarterly or monthly.

An increase in the repayment period of receivables indicates that increased control over buyer payments is necessary in order to avoid financial instability and the need for additional financing.

Companies with pronounced seasonality should pay special attention to comparing values for similar periods of previous years, because analyzing the indicator only within the current year will not allow you to get a correct idea of the situation that occurs with maximum and minimum demand for goods/services.

If the company provides a deferred payment, and the period exceeds the turnover of accounts receivable in days, then this jeopardizes the entire activity of the company, because The company may have constant problems with liquidity and cash gaps. In this case, it is necessary to urgently take measures to reduce receivables, otherwise the company will have to take money from working capital, thereby reducing the effectiveness of its activities.

The longer the turnover period, the higher the risk of debt default. The indicator can be calculated separately in relation to:

- Individuals and legal entities.

- Types of clients (new, regular, key, etc., each enterprise has its own rules for distributing clients into groups).

- Work of the enterprise as a whole and individual types of products/services.

- Terms of contracts (tariffs, size of shipments, etc.).

- Sources of attracting clients.

- Region of location of the client.

- Managers who are busy with clients.

- Duration of debt (under contract and in fact).

Examples of calculations

The calculation of the indicator is given in the table ().

Thus, the average receivables turnover period for 2017 was 39 days. The fastest time to receive money from clients was in the 1st quarter - 37.5 days. Debts took the longest to be repaid in the 2nd quarter - 45 days. But by the end of the year the figure leveled off and became less than average - this is a good sign.

Summary

To ensure that an enterprise does not experience a shortage of working capital, it is necessary to receive money from customers for shipped goods or services in a timely manner (avoid delays) and reduce the period for repaying receivables. Otherwise, the company may have difficulties with solvency, and this will already leave an imprint on the activities of the company as a whole and will lead to losses in the future period.

Accounts receivable calculation - formula This calculation may vary from company to company. Find out what components it consists of and what it is used for from our material.

Why do you need to calculate accounts receivable?

Accounts receivable calculation(DZ) is a procedure familiar to balance sheet specialists. It is carried out during the preparation of financial statements, as well as when it is necessary to obtain information about remote control for management and (or) other purposes.

In order for data to appear in the balance sheet on line 1230 “Accounts receivable”, the following is required:

- Collect information on the accounting accounts on which the debt is recorded and analyze it (by amounts, types of debtors, repayment periods, etc.).

The material will tell you about the classification and types of remote sensing.

- Reconcile the amounts reflected in the accounting accounts with counterparties (for example, through bilateral agreement of mutual settlements in the reconciliation report).

- Take an inventory of settlements with counterparties (if an annual balance sheet is being drawn up or the debt is subject to write-off).

For an algorithm for conducting a remote control inventory, see the material.

- Identify doubtful debts and debts with expired statute of limitations.

- Create a reserve for doubtful receivables (if unpaid and unsecured debts are identified).

The following material will help you understand the receivables reservation procedure.

- Register the write-off of financial assets from the accounting accounts (if there are grounds for such a write-off).

- Carry out other preparatory procedures (distinguish between loan receivables with a repayment period of up to a year or more, which may be required when preparing transcripts on line 1230, etc.).

Why do you need decoding of the remote control and how to prepare it, see the material.

- Calculate the amount of receivables to be reflected in the balance sheet on line 1230.

We will tell you what formula to use to calculate remote sensing in the next section.

How to calculate accounts receivable?

There is no universal formula for calculating remote sensing. In each company, the structure of receivables may be different, and therefore the composition of the formula is adjusted.

In general, the following formula is used:

DZ = debit balance (account 60 + account 62 + account 68 + account 69 + account 70 + account 71 + account 73 + account 76) - account 63,

sch. 60 - “Settlements with suppliers and contractors” for prepayment related to the supply of materials, performance of work, etc.;

sch. 62 - “Settlements with buyers and customers” for products shipped, work performed, services provided;

sch. 68 - “Calculations for taxes and fees” in terms of existing tax overpayments;

sch. 69 - “Calculations for social insurance and security” for excess amounts paid to the Social Insurance Fund and the Pension Fund;

sch. 70 - “Settlements with personnel for wages” in the presence of wage overpayment;

sch. 71 - “Settlements with accountable persons” for funds paid to employees on account;

sch. 73 - “Settlements with personnel for other transactions” for the amounts of loans provided to employees or for other transactions;

sch. 75 - “Settlements with founders” for the debts of the founders on contributions to the authorized capital of the company;

sch. 76 - “Settlements with various debtors and creditors” in connection with accrued income from joint activities, sanctions recognized by debtors for failure to fulfill contractual terms, etc.;

sch. 63 — “Provisions for doubtful debts” based on the amount of the formed reserve.

The general form of the formula for calculating the remote control is adjusted depending on the presence or absence of:

- debit balance on separate accounting accounts;

- reserve for doubtful debts.

For example, the company has no doubtful debtors, overpayments of taxes and contributions to extra-budgetary funds, no money is issued on account and there are no other monetary transactions for settlements with employees in the reporting period, and the authorized capital is fully paid by the founders. In this case, the adjusted formula for calculating the remote control will look like:

DZ = debit balance (account 60 + account 62 + account 76).

When the DZ indicator is used in other formulas, read on.

What formulas involve the accounts receivable indicator?

The DZ indicator is used in calculating various financial ratios, for example:

- financial stability;

For an algorithm for calculating financial stability, see the material.

- liquidity and solvency;

You will find formulas for their calculation in the material.

- asset turnover, etc.

Results

The calculation of accounts receivable is necessary for reporting and management purposes. Based on the calculated amount of receivables, financial ratios are calculated and the company’s activities are assessed.

It must be said that accounts receivable (AR) include debts that its buyers (customers) have to the enterprise after the product (service) has been delivered (provided) to them.

If an enterprise owes money to its suppliers (contractors) or to pay taxes, government fees, or pay for work, then accounts payable (AC) appears on the balance sheet.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

The profit of the enterprise depends on the ratio of debt and debt; the faster debtors repay debts, the more current assets there will be that can be disposed of. And vice versa, the more the company has to pay off its debts, and the debtors’ payments will be insignificant, the faster it will end up in losses.

In fact, the extent to which the enterprise can be solvent and what its financial stability is depends on the turnover of the receivables and receivables. Calculation of loan turnover is necessary for constructing a credit policy to the extent that the enterprise itself can allow its clients (buyers) to pay with a delay. Analysis of the turnover of accounts receivable and accounts payable allows us to draw conclusions about the size of the annual turnover of funds.

In order to improve the operation of the settlement and payment system, and thereby speed up the process of financial turnover, attract other assets and pay off debts, enterprises use various methods, including planning.

The main purpose of the analysis is to determine the speed at which debts turn over and the time during which this occurs. Moreover, this is important at different stages of the enterprise’s activity, because it is necessary to know how quickly the turnover occurs, and money turns into goods, and the latter, in turn, into money. Turnover is characterized by a time period and can be expressed using coefficients that indicate the intensity of turnover.

Thus, the most popular ratios for financial analysis of an enterprise as a whole are turnover indicators:

- current assets and others;

- stocks;

- own capital;

Definition of the term

What is inventory turnover? In fact, this is the average time interval during which receivables are repaid, in other words, how quickly buyers (customers) pay for the delivered product (service). Moreover, the payment can be ordinary, when, according to the contract, the moment of payment has not yet arrived, and overdue, if the buyer misses the payment deadline. In any case, from the moment the goods are delivered, the enterprise has a liability.

If the buyer (customer) pays earlier for a product (service) that has not yet been delivered, then the company will have a shortfall. Deposit turnover, expressed in days, shows how efficiently the enterprise operates, and funds are freed up for new investments. If a large debt accumulates, then the company has to use borrowed funds.

The sales turnover ratio, which is calculated during its analysis, allows you to see how many times during a year or other period the company received payment for goods from customers.

For the calculation, it is not the buyer’s full payment that is taken into account, but the size of the average balance of the debt that is considered still unpaid (regular or overdue). Using this coefficient, you can determine the effectiveness of the enterprise’s work with its clients (customers).

What is needed for this

The turnover ratio allows you to see how stable the company's financial position is in a market economy. Having a high ratio, you can understand that the company manages to pay off accounts receivable as quickly as possible.

If the turnover ratio of a subsidiary decreases or is already low, this means that the enterprise:

- quite a lot of buyers who, for certain reasons, have become insolvent or simply do not pay on time for the goods (services) received;

- a soft policy towards buyers, because today it is necessary to conquer a large part of the market, i.e. many receive long deferments on payments, etc.

If an enterprise has a low turnover ratio and a high profitability, then there is a greater need for working capital, due to which it is necessary to increase sales, and vice versa. Therefore, in such cases it is often necessary to use borrowed funds, which entails an increase in the cost of goods and other expenses.

Basic indicators

The turnover of not only accounts payable, but also accounts payable turnover can be characterized by the following key indicators:

- turnover in days;

- turnover ratio.

To analyze the turnover of household goods, it is necessary to take into account that there are other indicators:

| Revenues from sales | In the calculation formula it is taken into account as the numerator. DP can be formed (increase or decrease) as payment for goods (services) is received, i.e. it directly depends on sales. |

| Industry average | It is compared with the turnover ratio of a particular enterprise. If the ratio increases, it means that the company is reducing sales on credit. When it decreases, the credit policy regarding the increase in payment time becomes more lenient. |

| Period for repayment of debts by debtors |

|

| Turnover ratio |

|

| Share of receivables in current assets (OA) | It is calculated as a percentage and represents the result of the private PD and OA, multiplied by 100%. If during the reporting period there was an increase in the share of remote work, then the work of the enterprise can be assessed negatively. |

| The share of overdue debts of debtors in the composition of debt | This indicator is calculated as the quotient of the overdue claim to the total amount of claim, multiplied by 100%. If during the period, which is most often chosen as a year (365 days), there is an increase in the indicator, this means that the number of overdue payments by debtors has increased. |

| Classification of property records by statute of limitations | It is better to calculate this indicator monthly separately for each customer and buyer. The dates for the formation of DM are considered to be:

|

Calculation formula

Receivables turnover can be determined in days, or the so-called average period that a company requires for customers to pay it off.

In this case, the debt collection turnover will be calculated as the debt collection period (DCP) using the formula:

- the average annual DZ (AGDZ) must be divided by the annual sales revenue (GVR);

- multiply the resulting result by the number of days (CD) in the reporting period (365).

DZ turnover:

PSD = SGDZ / GVR * KD

To calculate the coefficient (indicator) of turnover of household goods (KobDZ), another formula can be used when sales revenue for the year (GVR) must be divided by the average annual revenue (AGDZ).

Turnover rate:

KobDZ = GVR / SGDZ

To calculate the turnover of remote parts with the smallest error, it is necessary:

- leave in the total revenue from sales for the period the amount of indirect taxes;

- Please note that sales revenue is calculated upon shipment of the goods, and payment for it occurs much later.

Example for 3 years and table

Inventory and reserves account for the majority of the total working capital, approximately 80%. At the same time, the company's reserves and creditors' debts account for approximately a third of all assets (30%).

The balance on the DZ balance is influenced by many factors:

- payment system adopted by the enterprise;

- Kind of activity;

- manufactured products;

- other.

To control remote work, it is necessary to constantly analyze its turnover in order to determine how the enterprise should act in the near future. It is also important to select buyers (customers) at the stage of concluding supply contracts (work performance).

To do this, the buyer must determine:

- financial stability;

- current solvency;

- payment discipline;

- financial opportunities;

- conditions in which a particular enterprise operates.

Typically, the turnover of household items is analyzed for 3 years, the indicators are presented in the form of a table, after which the appropriate conclusions can be drawn:

| Required indicators | 2014 | 2015 | 2016 | Deviations | |

| 2015 from 2019 | 2016 from 2019 | ||||

| GWR (thousand rubles) | 1300 | 1500 | 1600 | 200 | 100 |

| SGDZ (thousand rubles) | 90 | 70 | 300 | -20 | 230 |

| KobDZ = GVR / SGDZ (times) | 14 | 21 | 5 | 7 | -16 |

| PSD = SGDZ / GVR * CD (days) | 25 | 17 | 68 | -8 | 51 |

Thus, the results of the table show that turnover first increased and then sharply decreased. But the period for debt repayment by debtors, on the contrary, was initially shorter, and then increased sharply.

Factor analysis of accounts receivable turnover

One of the indicators that is used to calculate debt turnover is the turnover or debt collection period (DCP). The formula for its calculation was presented above. In order to determine the efficiency of individual employees or departments of the enterprise, the actual value of design and estimate documentation is compared with the standard.

It is possible to determine how their actions could affect the work of the entire enterprise by determining the deviation from the norm, which, in turn, must be decomposed into influencing factors. Only after this can appropriate conclusions be drawn. One of the factors is the average annual PD.

To determine the average annual remote control (AGDZ) it is necessary:

- sum up the balance of the loan at the beginning and end of the reporting period;

- divide the result by 2.

Average annual remote control:

SGDZ = (DZNOP + DZKOP) / 2

The balance of the loan at the end of the period will depend on the balance at the beginning and receipts of revenue during the period and other income.

In fact, the following factors influence the PSD (turnover period):

- DZNOP (at the beginning of the reporting period);

- receipts during the reporting period (OP);

- accrued income for OP;

- number of days in OP.

The actual analysis of household turnover is carried out according to the formula, where:

- the numerator contains the actual value of the turnover period of the DZ (PSD), multiplied by the quotient of the number of days in the period (CD) and actual income (revenue - FGVR);

- the denominator is the planned value of the turnover period of the DZ (PSD), multiplied by the quotient of the number of days in the period (CD) and planned income (revenue - PGVR).

FGVR and PGVR – actual and planned annual sales revenue. Otherwise, the actual and planned ratio of the turnover period of the DZ (PSD) may look like the ratio of the actual DZf, divided by the actual income (Df), to the planned DZ (DZp), divided by the planned income (Dp).

The ratio of planned and actual income is a final value. Next, the factors influencing turnover will have to be divided into the average indicators of the debt that actually arose at the enterprise and was planned.

It is necessary to take into account that the planned design and estimate documentation does not always correspond to the standard adopted for the turnover of remote parts.

Therefore, when carrying out factor analysis, it is necessary to decompose the deviation of the actual value of PSD from the planned value into 2 components:

- deviation of the actual design estimate from the planned one;

- deviation of the planned design and estimate estimate from the norm.

Availability of accounts payable

The analysis of receivables turnover is influenced by the short-term turnover. Accounts payable turnover (AC) should be understood as the amount of debts of an enterprise to creditors, which must be repaid within a certain period. It also includes current purchases or goods/services that were purchased from the supplier.

The short-term loan turnover ratio shows how many times during the year the average short-term amount was repaid. If an enterprise has high balances on its balance sheet, this means its solvency and financial stability are reduced.

Despite this, until the company repays its debts to creditors, it is actually using “other people’s” money. As long as the KZ exists, free “other people’s” money is always available, which can be used as a source of financing for business activities.

In its own way, this is a benefit for the enterprise; the higher the turnover of the DZ compared to the turnover of the KZ, the more stable the financial position of the enterprise. But it is beneficial for the company’s creditors if it has a high short-term turnover ratio.

Typical mistakes in an enterprise

The formulas used to analyze home ownership turnover do not always give correct results. One of the mistakes is to perform the actual analysis using the above formula.

Using the example of the activities of a particular enterprise, one can see that the most determining factor is the deviation in the level of income of the enterprise - actual and planned. But in reality it doesn't exist. Also in this case there is no deviation of the actual remote control from the planned one.

When calculating, it turns out that there is an increase in income, and the turnover period (TRP) of receivables becomes shorter. But actually it is not.

There are limitations to the formula, which is widely used in accounting:

- the average annual PD should be an average, not an arithmetic one, i.e., for the reporting period, an indicator should be derived whose fluctuations will be minimal;

- income and receipts for the reporting period should differ slightly.

In fact, in practice, it is best to calculate the weighted average DCI (debt collection period), which must be carried out for each specific payment document. To do this, the specific date of payment of the enterprise for the product (service) is subtracted from the planned payment date. This value is weighted by the payment amount.

Optimal value

It is impossible to apply clear standards to the turnover of household goods, because it directly depends on the activities of the enterprise. For example, in trade, the turnover of the asset will always be high, and the asset itself will always be low. If an enterprise makes sales on credit, then the profit margin will always be high and the turnover ratio will be low, but this does not mean that the operation of the enterprise is ineffective.

From the above examples, we can say that a constant analysis of loan turnover allows any enterprise to draw conclusions on how to build a credit policy with customers.

Accounts receivable turnoverindicates how long it takes to repay the customers' debt for the delivered goods. This indicator, among others, characterizes the financial stability of the company.

Why is the accounts receivable turnover ratio calculated?

The accounts receivable turnover ratio is used to conduct a financial analysis of the company's sustainability in a competitive market environment. The calculated accounts receivable turnover ratio will show how effectively the company collects debts for goods supplied.

A decrease in the coefficient may indicate that:

- The company increased the share of insolvent customers.

- The company decided to pursue a more lenient policy with customers in order to gain a larger market share by providing longer payment deferrals to its customers. Accordingly, the lower the specified ratio, the higher the company's need for working capital, which is necessary to increase sales volumes.

To calculate the accounts receivable turnover ratio, a simple formula can be used that looks like this:

Kob = Op / DZsg,

Kob - debtor debt turnover ratio;

Op - sales volume at the end of the year (revenue from sales);

DZsg - average annual debt of debtors.

To determine the average annual DZ, the following formula is used:

DZsg = (DZng + DZkg) / 2,

DZng - debt as of the beginning of the year;

DZkg - debt as of the end of the year.

The receivables turnover period is defined as the ratio of receivables to revenue

By calculating how quickly receivables will be repaid in days, you can determine the average period required for the company to collect debts from buyers. To calculate it, the receivables turnover formula is used, which looks like this:

Psb = DZsg / Op × Dn,

PSB - debt collection period;

Days—number of days in the billing period. If the calculation is made for a year, then Day will be equal to 365.

As a result, the receivables turnover period is determined as the ratio of the amount of average annual “receivables” to the volume of revenue. If the repayment period of receivables needs to be calculated in daily terms, then their number in the calculation period is added to the denominator.

How to determine the turnover period of accounts receivable without errors?

- abandon the practice of using the value of revenue cleared of indirect taxes (excise taxes, VAT), since receivables, as a rule, contain these indirect taxes;

- Please note that sales revenue is calculated when products are shipped, while payment for them is made later.

How to analyze accounts receivable turnover?

Accounts receivable turnover (value in days) shows the average length of deferred payment that the company offers to its customer customers.

The lower the receivables turnover value is, the more efficiently the company’s capital works, since funds are released faster for new investments. If borrowed funds are used for turnover, then reducing the period of use of these funds makes them cheaper.

Results

Without calculating accounts receivable turnover, the company will not be able to build its own credit policy for working with customers. The decision to grant a deferred payment and its duration should be made taking into account all information about the financial condition of the company and its strategic plans.

Having analyzed its own resources/capabilities and compared them with its goals, the company determines the maximum and minimum limits of possible deferment of payment by customers. This value will subsequently be used when concluding transactions with them. This can significantly reduce the repayment period of accounts receivable.

DEFINITION

Using the amount of receivables, the monetary obligations of third-party counterparties are reflected. Accounts receivable includes funds for shipped products (services provided) not paid by customers.

The formula for the repayment period of receivables reflects how quickly funds for products (services) will be returned, while characterizing the effectiveness of interaction between the company and counterparties. At the same time, the higher the accounts receivable turnover ratio, the faster the company makes settlements with its customers.

The formula for the repayment period of receivables is a way to increase the profitability of an enterprise, since the calculation of the indicator for it shows the dynamics of receivables. Accounts receivable management is about increasing turnover. This is possible by increasing revenue or reducing accounts receivable.

Accounts receivable period formula

There are two options for calculating the receivables collection period formula, with the first option being calculated as follows:

DSO = (360*DZsr) /V

Here DSO is an indicator of the receivables repayment period,

DZ av - average amount of receivables (for example, average annual),

B is the amount of revenue.

The second option for calculating the formula:

DSO = 360/RTR

Here RTR is an indicator of accounts receivable turnover.

The average annual amount of accounts receivable (AAR) can be calculated by summing the values of accounts receivable for each day and dividing by the number of working days.

The second option for calculating the formula is carried out by summing the values of accounts receivable at the end of all months and then dividing by 12.

If only annual data is available (at the beginning and end of the year), then they are added and then divided by 2 (or multiplied by 0.5).

DZsr = (DZng + DZ kg) / 2

Receivables turnover formula

The calculation of the receivables turnover ratio (RTR) is necessary for the second version of the formula for the repayment period of receivables and is determined by the data of the balance sheet (Form 1) and the income statement (Form 2).

The general formula for accounts receivable turnover is as follows:

RTR = V/DZ

Here RTR is the accounts receivable turnover ratio,

B is the company’s revenue for the corresponding period,

DZ – the amount of receivables (for example, the average for the year when calculating annual values).

The value of the receivables repayment period

The accounts receivable period is a tool for determining the effectiveness of customer relationships, reflecting the time they pay invoices. Using the indicator, you can evaluate the payment discipline of customers.

By applying the formula for the repayment period of receivables, analysts calculate the level of effective management of receivables. For example, if an enterprise has established a maximum period for consumer commodity lending of 15 days, then the repayment period for receivables should not exceed this value.

Examples of problem solving

EXAMPLE 1

EXAMPLE 2

| Exercise | The following accounting information is given for two companies: 1 company The amount of accounts receivable at the beginning of the period is RUB 352,200, At the end of the period - 421,200 rubles, 2 company The amount of accounts receivable at the beginning of the period is RUB 411,500, At the end of the period - 405,000 rubles, Revenue amount 1 company RUB 11,315,000, 2 company RUB 11,828,000, Determine the repayment period for receivables. |

| Solution | Let's calculate the average value of accounts receivable for each company: DZ avg.(1) = (352,200+421,200)/2=386,700 rub. DZ avg.(2) = (411,500+405000)/2=408,250 rub. DSO = (360*DZsr) /V DSO(1) = 360*386,700/11,315,000=12.3 days DSO (2) = 360*408250 / 11,828,000=12.43 days |

| Answer | DSO (1) = 12.3 days DSO (2) = 12.43 days |