Is it possible to return the overpayment of penalties? Application for crediting the amount of overpaid tax: sample

In 2019, the documents that legal entities and individuals must use to offset and return overpayments of taxes have changed. Let's look at what the application form for offset of overpayment of tax now looks like and how to fill out this document correctly.

Application forms used to offset and return amounts of overpaid (collected) taxes, fees, insurance premiums, penalties, and fines were approved by Order of the Federal Tax Service dated February 14, 2017 No. ММВ-7-8/182@. They should be used by both individuals and legal entities. But since 2019, small changes have been made to the Federal Tax Service order, which must be remembered.

When will new forms be needed?

According to Article 78 of the Tax Code of the Russian Federation, taxpayers who have overpaid can dispose of the overpaid amounts in different ways:

- offset them as future payments;

- pay off arrears on other mandatory payments;

- reduce or completely eliminate the debt on penalties and fines for offenses;

- demand a refund.

These rules apply to all fees and taxes introduced in the Russian Federation, including state duty (with some features listed in Article 333.40 of the Tax Code of the Russian Federation), VAT, advance payments. However, you must understand that the tax service will not return or offset the overpaid amount against future payments until the debt is paid off.

Sample application for offset of overpaid tax

If the taxpayer decides to reallocate his money, he needs to write a tax offset application. The form of this document is presented in the order of the Federal Tax Service from application No. 9. You can download it at the bottom of the page.

How to fill out such a document

Let’s say Kolosok LLC filed a transport tax return for 2018, but when paying it made a mistake, paying 3,112 rubles more. The organization applies to the interdistrict Federal Tax Service and asks for a credit for the overpayment of taxes; she writes in order to have the overpaid amount credited to her upcoming corporate property tax payments. Let's look at filling out such a document step by step.

Step 1. Traditionally, the TIN and KPP should be indicated at the very top. The individual entrepreneur’s identification number consists of 12 digits, so there should be no free cells left. Organizations enter only 10 numbers in the appropriate fields, and put dashes in the remaining two. When filling out the line intended for the checkpoint, applicants must act in the same way: if there are numbers, enter them, if not, put dashes.

Step 2. Enter the request number. Here they put down the number of times in the current year they applied for the test. Don’t forget about dashes if the number of numbers to be entered is less than the number of cells.

Step 3. Enter the code of the tax authority where the application will be sent. This should be an inspection of the Federal Tax Service at the place of registration of the individual entrepreneur or organization. In a consolidated group of taxpayers, the responsible member of this group must request a credit for the overpayment of income tax.

Step 4. We write down the full name of the applicant organization, for example, limited liability company “Kolosok”. Fill in the remaining cells with dashes. None of them should be left empty. When filling out this field by an individual entrepreneur, he must indicate his last name, first name and patronymic, if any. In addition, the status of the applicant, as whom he is applying, should be indicated in accordance with the instructions:

- taxpayer - code "1";

- fee payer - code "2";

- payer of insurance premiums - code "3";

- tax agent - code "4".

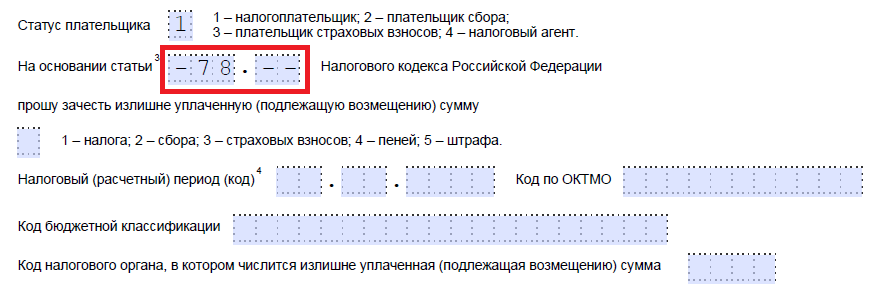

Step 5. We indicate the article of the Tax Code of the Russian Federation, on the basis of which the offset can be made. It will depend on which payment was overpaid. The Federal Tax Service left 5 cells to indicate a specific article. If some of them are not needed, dashes must be added. Here are the options for filling out this field:

- - for offset or return of overpaid amounts of fees, insurance premiums, penalties, fines;

- — for the return of overcharged amounts;

- — for VAT refund;

- — to return the overpayment of excise tax;

- — for a refund or offset of state duty.

Step 6. We write down what exactly the overpayment was for - taxes, fees, insurance premiums, penalties, fines.

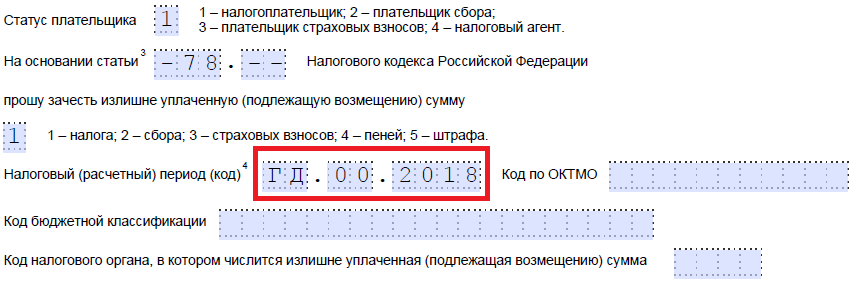

Step 7. The applicant specifies for what period the overpayment occurred. The developers provided 10 familiar places to indicate the code, of which two are dots. The first two of them can be filled in with one of the following options:

- MS - monthly;

- KV - quarterly;

- PL - six-monthly;

- GD - annual.

Specific values will depend on the reporting period provided for by law for the payment for which offset is planned.

In the 4th and 5th acquaintances, the reporting period is specified:

- if a monthly billing period is approved for payment, then enter the numerical value of the month (from 01 to 12) in the provided columns;

- if quarterly, indicate the value of the quarter (from 01 to 04);

- for payments with a semi-annual reporting period, enter values 01 or 02, depending on the semi-annual period;

- For the annual fee, zero values are provided, that is, “0” must be entered in both cells.

The last four familiar places are intended to indicate a specific year, for example 2019.

Instead of alphanumeric combinations, a specific date can be recorded, for example 01/25/2019. Such an entry is permitted if the legislation provides for a specific date for paying the fee or submitting a declaration.

Examples of filling out the billing period: “MS.02.2019”, “KV.03.2019”, “PL.01.2019”, “GD.00.2019”, “04.05.2019”.

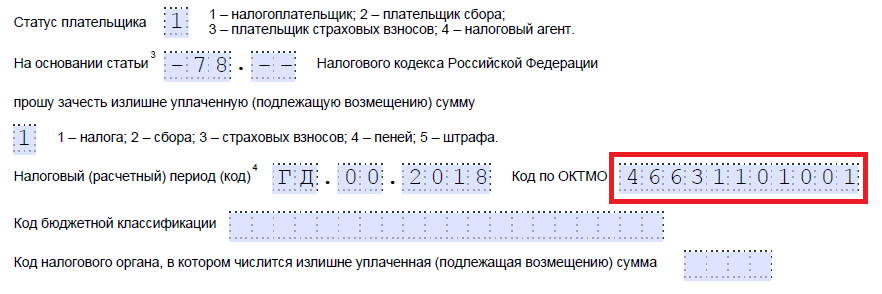

Step 8. Enter the OKTMO code. If you don’t know it or have forgotten it, you can call the Federal Tax Service at the place of registration or go to nalog.ru to find out the required code by the name of the municipality.

Step 9. We accurately enter the KBK for payment of the corresponding payment, using Order of the Ministry of Finance of Russia dated 06/08/2018 N 132n. You can also find out the code using the Federal Tax Service website or look at it on a previously completed payment order.

Step 10. We clarify to which Federal Tax Service the excess funds were transferred.

Step 11. On the first sheet, it remains to fill in how many sheets the application is submitted on and how many sheets of supporting documents are attached, as well as indicate information about the applicant himself. We recommend leaving these two small sections for later.

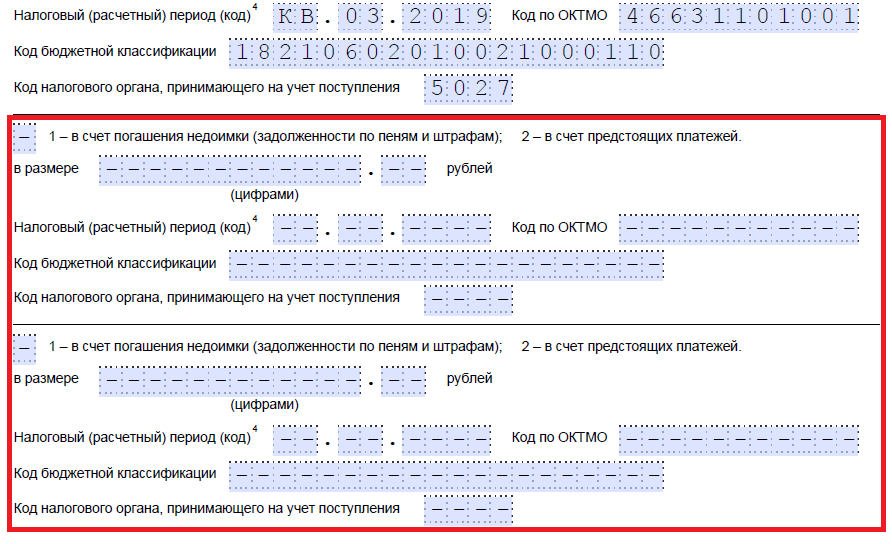

Let's continue filling on the second sheet. In the very first field where you need to indicate your last name, first name and patronymic, put dashes. Below we indicate what needs to be done with the overpayment - pay off the debt or leave funds for upcoming payments.

Step 12. We write down the specific amount that the applicant wants to offset. It is indicated in numbers, without text decoding.

Step 13. We fill in the period for the payment for which we plan to offset. In our case, the corporate property tax is quarterly, so we enter the quarter in which the overpayment should go.

Step 14. Write down the OKTMO code again. As a rule, it is duplicated.

Step 15. We specify the KBK for the transfer of funds, into which the excess amount will go. Ours is different from the previous KBK, since the taxes are different. If the overpayment goes towards future payments for the same fee, then the BCCs are the same. An exception is if the codes were previously changed by decision of the Ministry of Finance. Let us also recall that offsets can be carried out according to certain rules: they must relate to the same type: federal, regional or local. For example, it is not possible to offset the federal portion of the income tax against upcoming trade tax payments.

Step 16. The code of the Federal Tax Service, which accepts receipts, is usually duplicated.

Step 17. Since there are no more overpayments, in our example the following lines are not filled in. You can put spaces there. Also, organizations and individual entrepreneurs do not fill out the third sheet. It is intended for individuals who are not registered as individual entrepreneurs and who have not indicated their TIN.

Step 18. Return to the first sheet and enter the number of pages and attachments. Applicants indicate the relevant data in the provided fields.

Step 19. The last part of the application should not cause problems when filling out. Here you need to clarify who is submitting the appeal and when, as well as indicate a contact phone number. The right side remains blank: it is intended for marks from Federal Tax Service inspectors.

How to get your money back

If an entrepreneur (company) decides to return the overpayment amount, he needs to use another form from the Federal Tax Service order dated February 14, 2017 No. ММВ-7-8/182@, proposed in Appendix No. 8. It contains a form for returning the excess amount.

The rules for filling out this document are approximately the same. Therefore, we will not consider them in detail, but will give an example of a completed document. Let’s say Kolosok LLC overpaid VAT for the first quarter of 2019 in the amount of 15,732 rubles and now wants to return it. This is what an appeal from the head of an LLC will look like.

When and how to submit an appeal

According to Article 78 of the Tax Code of the Russian Federation, you can apply for credit and refund within 3 years from the date of payment of the fee. There are three ways to deliver documents:

- personally;

- by mail with a valuable letter with an inventory;

- in electronic form via telecommunication channels or through a personal account.

Having received such an application, the tax authority decides whether to satisfy it or not. The service notifies the entrepreneur of its decision within 10 days from the date of receipt of the application. As a rule, if the initiative comes from an organization or individual entrepreneur, the Federal Tax Service does a reconciliation of the calculations. If the inspector himself discovers the overpayment, the reconciliation may be refused. The entrepreneur is not relieved of the obligation to submit an application.

She explained the difference between clarifying the payment and offsetting the overpayment. If a taxpayer transferred the tax on time, but later discovered an error in the payment slip that did not result in non-payment of this tax to the budget, he has the right to submit an application for clarification of the payment. In this case, the date of payment of the tax will be considered the date of transfer of the incorrect payment. Accordingly, no penalties should be charged. And in case of offset, the obligation to pay tax is considered fulfilled from the day the decision on such offset is made. Therefore, when offsetting the overpayment to repay the arrears, penalties cannot be avoided.

Payment clarification

As is known, the tax is considered paid from the moment a payment order is presented to the bank for the transfer of funds from the taxpayer’s account (provided there is a sufficient cash balance on it) to the budget system to the appropriate account of the Federal Treasury (subclause 1, clause 3, article 45 of the Tax Code of the Russian Federation ). Paragraph 4 of Article 45 of the Tax Code specifies only two types of errors in the “payment” in which the tax is not considered paid: an incorrect Federal Treasury account number or an incorrect name of the payee’s bank.

Thus, if the error did not lead to non-transfer of tax to the budget (for example, an incorrect BCC was indicated), then arrears do not arise. In such a situation, the payment can be clarified (clause 7 of Article 45 of the Tax Code of the Russian Federation). To do this, you must submit to the Federal Tax Service documents confirming payment of the tax, and an application asking to clarify the basis, type, affiliation of the payment, tax period or payer status.

Offset of overpayment

The procedure for offsetting overpaid (collected) tax against arrears differs from the procedure for clarifying payment. The main difference is that as a result of clarification, the tax is actually recognized as paid properly. This means that there are no grounds for charging a penalty. And when offset, the obligation to pay tax is considered fulfilled from the date the tax authority makes a decision on offset (subclause 4, clause 3, article 45 of the Tax Code of the Russian Federation). Therefore, in the case of offset of the overpaid amount of tax against arrears on another tax, the accrual of penalties until the decision on offset is made is lawful.

Tax Code of the Russian Federation):

- offset against tax debt, penalties, fines;

- offset against future tax payments;

- return to bank account.

1. Offset of overpayment towards repayment of tax debt, penalties, fines

First of all, the amount of overpayment of tax must be offset against arrears on other taxes, debts on penalties and fines. There is no need to submit an application for such an offset, since the tax authority will carry out the offset on its own. From the date the inspectorate makes a decision to offset the arrears, penalties, and fines, they are considered paid (clause 4, clause 3, clause 8, article 45, clause 5, article 78 of the Tax Code of the Russian Federation).

2. Offset of overpayment towards payment of upcoming tax payments

To offset the amount of overpaid tax against upcoming payments for this or other taxes, you must submit an application to the tax authority (clause 4 of article 78 of the Tax Code of the Russian Federation).

An overpayment can only be offset against payment of tax (tax penalties) of the same type (Clause 1, Article 78 of the Tax Code of the Russian Federation). So, for example, an overpayment of a local tax can only be offset against the payment of this or another local tax (penalties on them).

Example. The procedure for offsetting overpayments of land tax against arrears of other taxes

A citizen has an overpayment of land tax and arrears of personal property tax and transport tax.

It is possible to offset the overpayment of land tax against the arrears of personal property tax, since both taxes are local. It is impossible to offset the overpayment of land tax against the arrears of transport tax, since transport tax is regional ( Art. Art. 14, 15, paragraph 1, Art. 78 Tax Code of the Russian Federation).

The fact that the objects of taxation for personal property tax, land and transport taxes are located in different regions (municipal areas or urban districts) does not matter.

Example. The procedure for offsetting overpayments on property taxes for individuals against arrears on other taxes

A citizen owns two apartments located in Moscow and a plot of land located in the Moscow region. A citizen has an overpayment of personal property tax and arrears of land tax. Since the arrears arose for the same type of tax, then, despite the location of taxable objects in different regions, the overpayment of property tax can be offset against the arrears of land tax ( Art. 15, paragraph 1, art. 78 Tax Code of the Russian Federation).

Note!

Overpayment of tax can be offset against the payment of a fine without taking into account the type of tax and regardless of the specific type of tax offense ( clause 1 art. 78 Tax Code of the Russian Federation).

3. Refund of the overpayment amount to a bank account

To return the overpayment amount to your bank account, you must submit an application to the tax authority (Clause 6, Article 78 of the Tax Code of the Russian Federation).

4. The procedure for contacting the tax authority with an application for offset or refund of overpayment

The period during which you can claim a credit or refund of the overpayment is three years from the date of payment of the tax (Clause 7, Article 78 of the Tax Code of the Russian Federation).

You need to contact the tax authority at your place of registration with a written application for a credit or refund of the overpayment. You can submit an application in person or through a representative directly to the tax authority, send it by mail or transmit it electronically, in particular through the taxpayer’s personal account (clause 1, article 26, clauses 2, 4, article 78 of the Tax Code of the Russian Federation).

The inspectorate must make a decision on offset or return of the overpaid amount within 10 working days from the date of receipt of the application or signing of the act of joint reconciliation of calculations, if such a reconciliation was carried out. Then, within five working days, the tax office will send you a message about its decision. Refund of the overpayment to your bank account must be made within one month from the date of receipt of the above application (

According to Art. 78 of the Tax Code of the Russian Federation, the offset of amounts of overpaid federal taxes and fees, regional and local taxes is carried out for the corresponding types of taxes and fees, as well as for penalties accrued on these taxes and fees. For example, the overpayment of income tax can be offset against payment of the same tax or other federal taxes. The Tax Code does not limit the possibility of carrying out an offset depending on which budget of the budget system of the Russian Federation the federal tax is payable to. Thus, the corporate income tax, which is federal, overpaid to the budget of one subject of the Russian Federation, can be offset against upcoming payments for this tax to the budget of another subject of the Russian Federation, taking into account the provisions of paragraphs 4 and 5 of Art. 78 Tax Code of the Russian Federation.

This is not the first time our magazine has addressed this topic.<1>. Today we will answer specific questions related to the offset (refund) of overpaid income tax, and also consider the situation with writing off an overpayment for which the deadline for applying for a refund has expired.

<1>See the articles “How to return or offset overpaid amounts of tax”, “Deadline for filing an application for a refund (offset) of overpaid tax”, 2011, No. 2.

Penalties for the period when the tax authority made a decision on offset

By virtue of paragraph 1 of Art. 45 of the Tax Code of the Russian Federation, the taxpayer is obliged to independently fulfill the obligation to pay tax, unless otherwise provided by the legislation on taxes and fees. This obligation must be fulfilled within the period established by law. The taxpayer has the right to fulfill the obligation to pay tax ahead of schedule.

According to paragraphs. 4 p. 3 art. 45, the obligation is considered fulfilled by the taxpayer from the day the tax authority, in accordance with the Tax Code, makes a decision to offset the amounts of overpaid or excessively collected taxes, penalties, and fines against the fulfillment of the said obligation.

The procedure for offsetting amounts of overpaid taxes is established by Art. 78 of the Tax Code of the Russian Federation, according to clause 1 of which the offset of overpaid federal taxes and fees, regional and local taxes is carried out for the corresponding types of taxes and fees, as well as for penalties accrued on the corresponding taxes and fees.

As a general rule, the Tax Code does not prohibit the offset of taxes in the payment of relevant types of taxes between the federal budget, regional and local budgets. Order of the Ministry of Finance of Russia dated September 5, 2008 N 92n<2>provides for interregional offset - carried out by tax authorities located in the territories of various constituent entities of the Russian Federation.

<2>"On approval of the Procedure for accounting by the Federal Treasury of revenues to the budget system of the Russian Federation and their distribution between the budgets of the budget system of the Russian Federation."

The offset of the amount of overpaid tax against the taxpayer's upcoming payments for this or other taxes is carried out on the basis of his written application by decision of the tax authority, which must be accepted within 10 days from the date of receipt of the taxpayer's application (clause 4 of Article 78 of the Tax Code of the Russian Federation). The tax authority does not have the right to independently (without the specified application) offset.

For your information. Paragraph 11 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 22, 2005 N 98 states: the period for offset of the amount of overpaid tax begins to be calculated from the date of filing the application for offset, but not earlier than from the moment of completion of the desk tax audit for the corresponding tax period or from the moment when such verification must be completed in accordance with Art. 88 Tax Code of the Russian Federation.

Clause 2 of Art.

A quick guide to the procedure for offsetting taxes, penalties and fines

57 of the Tax Code of the Russian Federation determines that when paying a tax in violation of the deadline, the taxpayer is charged penalties in the manner and under the conditions provided for by the Tax Code of the Russian Federation. Penalties are recognized as an established amount of money that a taxpayer must pay in the event of payment of due amounts of taxes or fees later than the deadlines prescribed by the legislation on taxes and fees (clause 1 of Article 75 of the Tax Code of the Russian Federation).

The Constitutional Court, in Ruling No. 202-O dated July 4, 2002, indicated that the penalty is an additional payment aimed at compensating for losses to the state treasury as a result of shortfalls in receiving tax amounts on time due to a delay in tax payment.

Thus, if the tax is credited to the budgets of different subjects and the decision to offset the amount of overpaid tax against upcoming payments for this tax is made by the tax authority in accordance with Art. 78 of the Tax Code of the Russian Federation deadlines, but after the established deadline for paying the tax, then from the day following the established day for paying the tax until the day such a decision is made by the tax authority, penalties will be charged on the amount of the resulting arrears.

For example, 01/20/2011, the organization sent an application via electronic communication to the tax authority to offset the amount of overpayment of income tax against VAT. The decision on offset was made by the tax authority on January 31, 2011, and penalties were assessed to the organization for the period from January 21, 2011 to January 31, 2011. The application for offset was submitted on January 20, that is, on the last day of the established deadline for paying VAT (before the arrears arose for this tax).

The tax authority did not violate the deadline for making a decision (within 10 days) on offsetting the amounts of overpaid corporate income tax against the payment of VAT and calculated penalties for late fulfillment of the obligation to pay tax correctly. This opinion was expressed by the Ministry of Finance in Letter dated July 25, 2011 N 03-02-07/1-260. Here he clarified that the Tax Code of the Russian Federation does not provide for the recalculation of the amounts of penalties accrued before the tax authority makes a decision to offset the amounts of overpaid tax in the circumstances under consideration (a similar opinion was expressed by financiers in Letter dated 02.08.2011 N 03-02-07/1 -273).

However, the arbitrators express a different opinion on this issue. For example, FAS PO in Resolution No. A57-14501/07-17 dated May 15, 2008, recognizing the tax authority’s accrual of penalties as unlawful, proceeded from the presence of an overpayment of taxes in earlier periods in an amount sufficient to cover the resulting arrears on other taxes. In addition, the taxpayer sent an application to offset the amounts of overpayment of one tax against the payment of another before the deadline for payment of the latter, therefore, promptly fulfilled the obligation to pay the above tax.

Overpayment of income tax, the deadline for applying for a refund has expired

In accordance with paragraph 7 of Art. 78 of the Tax Code of the Russian Federation, an application for offset or refund of the amount of overpaid tax can be submitted within three years from the date of payment of the specified amount.

In practice, it is not uncommon for an organization’s personal account card to show an overpayment of income tax. The amount of the existing overpayment is confirmed by the act of joint reconciliation of calculations for taxes, fees, penalties and fines. At the same time, the deadline for applying for a refund of the overpayment has expired, and therefore the organization plans to write it off.

Is it possible to classify a write-off overpayment of income tax that has expired as an expense that reduces the tax base for income tax?

This is what the Ministry of Finance reports (see Letter dated 08/08/2011 N 03-03-06/1/457). Clause 1 of Art. 252 of the Tax Code of the Russian Federation provides that expenses that reduce the tax base for the purposes of calculating income tax are recognized as justified (economically justified) and documented expenses, provided that they are incurred to carry out activities aimed at generating income.

Considering that within three years the taxpayer did not apply to the tax authority for a refund of the tax overpayment, the amount of the specified overpayment is not a receivable and is not recognized as a bad debt under clause 2 of Art. 266 of the Tax Code of the Russian Federation and does not reduce the tax base for corporate income tax.

In addition, according to paragraph 4 of Art. 270 of the Tax Code of the Russian Federation, expenses in the form of income tax are not taken into account when determining the tax base for income tax.

O.Yu. Pozdysheva

Journal expert

"Income tax:

accounting of income and expenses"

An overpayment of taxes, even a very small one, is like the proverb: “It’s a small misfortune, but it doesn’t let you sleep.” Full immersion in the topic will make it easy to restore the balance in tax payments before the statute of limitations makes it excruciatingly painful.

In general, the action plan is simple: discovered ⇒ chose: refund or offset ⇒ submitted an application to the tax office ⇒ received a refund or offset of the overpayment.

BLANKS AND FORMS on the topic

So, overpayment of tax: how to return? – read below in full detail and with illustrations. (the article mainly talks about overpayment of “tax”, but everything stated is also true for fines and penalties for taxes – approx. editorial staff)

The content of the article

|

What to do if there is an overpayment of taxes?

Overpayment of tax can occur in two cases:

- you are mistaken - this is unnecessary paid tax;

- the tax authority made a mistake - this is unnecessary exacted tax.

In the second case - the amount of excess tax collected is refundable with interest(from the day following the collection to the day of return or offset at the Bank of Russia refinancing rate in force during this period).

The distinctive criterion is the basis for the transfer to the budget.

Overpaid tax is formed if you paid an amount more than required by law. The reasons may be different, for example:

- the entrepreneur himself (without the “help” of tax authorities) incorrectly calculated the amount of tax;

- error in the payment (incorrect amount, incorrect details, repeated payment, etc.);

- change in the tax regime (for example, in the middle of the year the right to use the simplified tax system was lost, and advance payments had already been made), changes in legislation;

- At the end of the year, the final tax amount is less than the advance payments made.

The common basis for these reasons is that the overpayment was made by the entrepreneur without the participation of the tax authority. If the tax authorities made a decision, made a demand, and you paid it, even voluntarily, this is already an excessively collected tax.

Overcharged tax– more was transferred to the budget than required by law, and this was caused by the actions of the tax authority. For example:

- the inspectorate assessed additional taxes, and the entrepreneur challenged them in court, but at the time of the court’s decision the money had already been transferred to the budget;

- the tax authority assessed tax, fines, penalties, reflected this in the decision based on the results of the tax audit and (or) in the request, the amounts were transferred to the budget, after which errors were identified. It does not matter whether the entrepreneur voluntarily paid the excess amounts or they were collected forcibly, it is important that the basis was “calculations” of the Federal Tax Service;

- The tax authorities identified an overpayment of taxes and independently carried out an offset against the arrears; it later turned out that there was an overpayment, but the debts in the repayment of which the overpayment was offset were accrued erroneously (an unlawful offset from the date of its implementation can be considered an excessively collected amount).

The resulting overpayment can be:

- offset against existing tax debts (fines, penalties);

- offset against future payments;

- return to the bank account.

The procedure for “offsetting” an overpayment is simpler than a refund; as a rule, the tax authorities are more willing to offset it. But offsets are only possible between taxes of the same level (see the next topic).

If there are tax debts (penalties, fines) that can be offset, first an offset will be made to pay them off; the remaining amount can be disposed of at your own discretion.

If there are debts that can be offset, tax authorities can independently direct the resulting overpayment to pay off the debt, without your application, notifying you “after the fact.” But they do not always show such independence. Therefore, you don’t have to wait for the Federal Tax Service and take the initiative: the test will be completed faster - less penalties.

If the overpayment is unnecessary recovered amount, there are no tax debts, and you want offset amounts against future payments– a question may arise, since the Tax Code does not directly indicate the possibility of such an offset (it only stipulates the return of such amounts). The approved application forms for this “option” require minor adjustments. However, the tax authorities may agree to this (internal regulations allow them such an offset). But it’s better to consult with the inspectorate first.

To return or offset tax overpayments, you must send an application to the Federal Tax Service. Application forms are approved by Order No. ММВ-7-8/09 (see below).

Which taxes can be offset?

All taxes are divided into groups (types): federal, regional and local. This distribution is established by the Tax Code (Articles 12 – 15).

Federal taxes and fees:

- taxes under special tax regimes (STS, UTII, Unified Agricultural Tax, Patent)

- value added tax;

- excise taxes;

- personal income tax;

- corporate income tax;

- mineral extraction tax;

- water tax;

- fees for the use of objects of the animal world and for the use of objects of aquatic biological resources;

- National tax.

Regional taxes:

- corporate property tax;

- gambling tax;

- transport tax.

Local taxes and fees:

- land tax;

- property tax for individuals;

- trade fee.

Overpayment can be offset only between taxes of the same group (type), regardless of which budget the revenues go to and which BCC (budget classification code).

In addition, an entrepreneur can act as a tax agent: for example, transfer personal income tax to the budget from the salaries of his employees. It is also impossible to offset between taxes for which the individual entrepreneur acts as a tax agent and taxes for which the individual entrepreneur is the taxpayer.

Application for offset of overpaid or collected tax (form/blank, sample)

![]() Adj. No. 9 to the Order of the Federal Tax Service of Russia dated March 3, 2015 No. ММВ-7-8/90@: open for viewing or filling out (doc, 32KB).

Adj. No. 9 to the Order of the Federal Tax Service of Russia dated March 3, 2015 No. ММВ-7-8/90@: open for viewing or filling out (doc, 32KB).

Application for refund of overpaid or collected tax (form/blank, sample)

![]() Adj. No. 8 to the Order of the Federal Tax Service of Russia dated March 3, 2015 No. ММВ-7-8/90@: open for viewing or filling out (doc, 34KB).

Adj. No. 8 to the Order of the Federal Tax Service of Russia dated March 3, 2015 No. ММВ-7-8/90@: open for viewing or filling out (doc, 34KB).

Sample form with comments.

Where should I go to offset or refund taxes, penalties, and fines?

As a general rule, you need to contact the tax authority at the place of registration (i.e., place of registration).

If an entrepreneur is registered with several tax inspectorates (at the place of business, at the location of the real estate), it is better to send the application to the tax authority where the overpayment was identified - this is the opinion of the Ministry of Finance. Although the Federal Tax Service in some cases believes that the taxpayer has the right to independently choose which tax office it is more convenient for him to contact.

If an error is discovered after a change in tax office, all applications are submitted at the place of current tax registration.

Some confusion may arise if there was a tax change during the period when the issue of credit/refund was “in process.” For example, an entrepreneur filed an application and changed the Federal Tax Service before the tax authorities made a decision. In such a situation, the tax authority at the old place of registration must complete the issue - this is not spelled out in the Tax Code of the Russian Federation, but follows from judicial practice.

If the tax authority made a decision on the “old” registration, and the entrepreneur challenged it in court, the court may oblige the tax inspectorate to fulfill the obligation to return/offset, both at the old and new place of registration (from the court’s point of view, the tax authorities are centralized system).

You can also return/set off the overpayment in court.

At the same time, for overpaid amounts, it is necessary to first contact the tax authority; if a refusal is received or a decision is not received at all, it is necessary to file a complaint with a higher authority and only after that - to the court.

Regarding excessively collected taxes, you can go directly to the court, but you can also first send an application to the Federal Tax Service.

What is the deadline to submit an application for a credit or refund of overpaid taxes?

Overpaid tax

The period for filing a claim with the tax authority is 3 years. In general, the period begins to count from the moment of payment.

Peculiarities:

- If the overpayment occurred when transferring advance payments (that is, at the end of the year the tax amounts turned out to be less than the advance payments already transferred), then the three-year period begins from the date of filing the annual declaration. Or from the statutory date for filing the return if the return is filed late.

- If the tax was paid in parts (several payments) and there was an overpayment, the period is calculated for each payment separately.

Rules for calculating the period:

- the term expires on the corresponding date and month of the last year of the term (i.e. the same date of the same month three years later);

- If the expiration date falls on a weekend or holiday, the expiration date is postponed to the next working day.

For example: an erroneous payment was made on October 28, 2014, since October 28, 2017 is a Saturday, then you must apply for a refund (offset) of the overpayment until October 30, 2017 inclusive.

The deadline for going to court when challenging the decision of the tax authorities is 3 months from the day the tax authority refused the offset (refund) or did not make a decision on the offset (refund) within the period established by the Tax Code (this is 10 working days).

You can also go to court with material requirement on offset or refund of overpaid taxes, i.e. file an application with the court not to appeal the decision of the tax authority, but to return (offset) the overpaid amount of tax. In this case, the general limitation period is 3 years. There is a fine line here, a legal one: if this is your case, contact a lawyer.

Overcharged tax

The deadline for contacting the tax authority is 1 month from the day you learned about the collection, or when the judicial act on the unlawful collection of taxes came into force.

The period for going to court is 3 years from the day you learned or should have known about the collection of excess payments.

P.S. Have you done everything and are waiting for a refund or credit? Be patient...

When will the inspectorate return (offset) the overpayment of taxes?

The tax office must make a decision on offset or refund of amounts within 10 working days after receiving your application. Tax authorities must notify of their decision within 5 working days after its adoption.

If the decision is positive, the following is carried out:

- credit – within 10 working days;

- return – within one month.

The period is generally counted from the date the Federal Tax Service receives the taxpayer’s application.

But. If an overpayment is detected by an entrepreneur, the tax authority has the right to not immediately believe it and initiate additional procedures:

- reconcile tax payments - no more than 15 working days (if there are no discrepancies - 10 working days);

- conduct a desk audit (if the presence of an overpayment follows from a declaration, for example, an annual or clarifying one) - no more than 3 months.

And after these procedures are completed, the countdown begins for the Federal Tax Service to make a decision and offset and return the overpayment, i.e. plus 10 business days for credit or plus a month for refund.

- Article 78 of the Tax Code of the Russian Federation (Part 1) “Credit or refund of amounts of overpaid taxes, fees, penalties, fines”

- Article 79 of the Tax Code of the Russian Federation (Part 1) “Refund of amounts of excessively collected taxes, fees, penalties and fines”

- Order of the Federal Tax Service of Russia dated 03.03.2015 N ММВ-7-8/90@ "On approval of document forms used by tax authorities when carrying out offset and refund of amounts of overpaid (collected) taxes, fees, penalties, fines"

- Letter of the Ministry of Finance of Russia dated July 12, 2010 N 03-02-07/1-315 (the offset and return of excess payments to the budget is carried out by the inspection at the place of your registration that identified the overpayment)

- Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 N 57, paragraph 33 (for overpaid payments, an appeal to the court is possible only after the inspection has refused to satisfy the claim or left it unanswered)

- Part 4 Art. 198 of the Arbitration Procedure Code of the Russian Federation (the period for going to court when challenging a decision or action (inaction) of the tax authorities is three months)